Advertisement

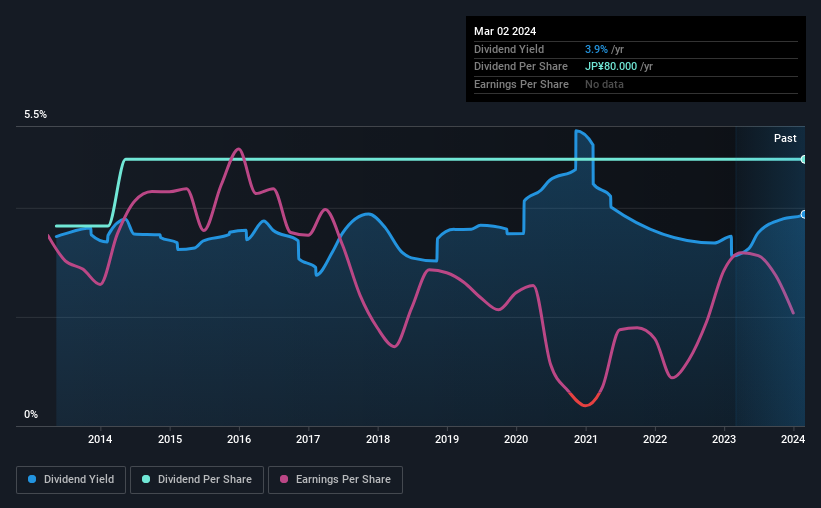

The board of Heiwa Corporation (TSE:6412) has announced that it will pay a dividend on the 1st of July, with investors receiving ¥40.00 per share. This makes the dividend yield 3.9%, which will augment investor returns quite nicely.

View our latest analysis for Heiwa

Heiwa's Dividend Is Well Covered By Earnings

While it is great to have a strong dividend yield, we should also consider whether the payment is sustainable. Prior to this announcement, Heiwa's dividend was only 67% of earnings, however it was paying out 2,391% of free cash flows. This signals that the company is more focused on returning cash flow to shareholders, but it could mean that the dividend is exposed to cuts in the future.

Unless the company can turn things around, EPS could fall by 7.8% over the next year. If the dividend continues along the path it has been on recently, we estimate the payout ratio could be 74%, which is definitely feasible to continue.

Heiwa Has A Solid Track Record

The company has a sustained record of paying dividends with very little fluctuation. The dividend has gone from an annual total of ¥60.00 in 2014 to the most recent total annual payment of ¥80.00. This means that it has been growing its distributions at 2.9% per annum over that time. While the consistency in the dividend payments is impressive, we think the relatively slow rate of growth is less attractive.

Dividend Growth May Be Hard To Come By

Investors could be attracted to the stock based on the quality of its payment history. Unfortunately things aren't as good as they seem. In the last five years, Heiwa's earnings per share has shrunk at approximately 7.8% per annum. Declining earnings will inevitably lead to the company paying a lower dividend in line with lower profits.

Our Thoughts On Heiwa's Dividend

Overall, it's nice to see a consistent dividend payment, but we think that longer term, the current level of payment might be unsustainable. While Heiwa is earning enough to cover the payments, the cash flows are lacking. Overall, we don't think this company has the makings of a good income stock.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. For example, we've picked out 1 warning sign for Heiwa that investors should know about before committing capital to this stock. Is Heiwa not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if Heiwa might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:6412

Heiwa

Develops, manufactures, and sells pachinko and pachislot machines in Japan.

High growth potential and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|27.0% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|5.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor