Advertisement

- Japan

- /

- Consumer Services

- /

- TSE:6071

There's A Lot To Like About IBJ's (TSE:6071) Upcoming JP¥8.00 Dividend

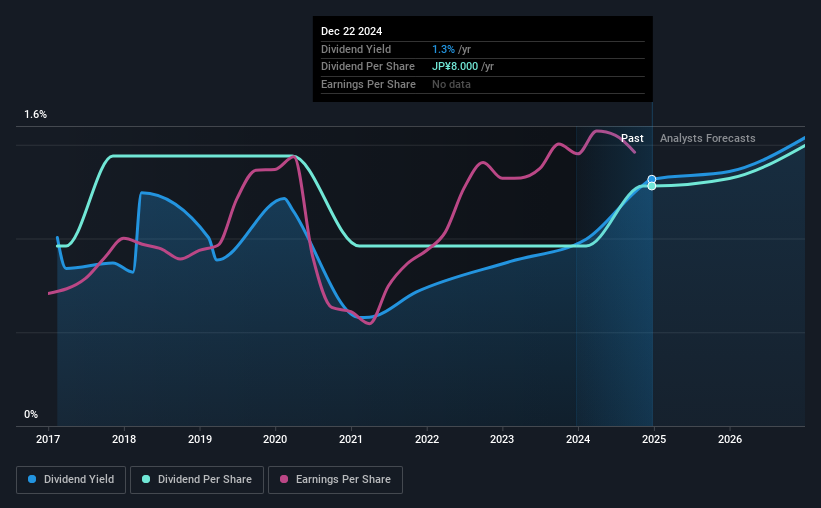

It looks like IBJ, Inc. (TSE:6071) is about to go ex-dividend in the next 3 days. The ex-dividend date occurs one day before the record date which is the day on which shareholders need to be on the company's books in order to receive a dividend. The ex-dividend date is important because any transaction on a stock needs to have been settled before the record date in order to be eligible for a dividend. This means that investors who purchase IBJ's shares on or after the 27th of December will not receive the dividend, which will be paid on the 26th of March.

The company's next dividend payment will be JP¥8.00 per share, on the back of last year when the company paid a total of JP¥8.00 to shareholders. Based on the last year's worth of payments, IBJ stock has a trailing yield of around 1.3% on the current share price of JP¥608.00. Dividends are a major contributor to investment returns for long term holders, but only if the dividend continues to be paid. So we need to investigate whether IBJ can afford its dividend, and if the dividend could grow.

See our latest analysis for IBJ

Dividends are typically paid out of company income, so if a company pays out more than it earned, its dividend is usually at a higher risk of being cut. IBJ has a low and conservative payout ratio of just 15% of its income after tax. That said, even highly profitable companies sometimes might not generate enough cash to pay the dividend, which is why we should always check if the dividend is covered by cash flow. Luckily it paid out just 15% of its free cash flow last year.

It's encouraging to see that the dividend is covered by both profit and cash flow. This generally suggests the dividend is sustainable, as long as earnings don't drop precipitously.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Businesses with strong growth prospects usually make the best dividend payers, because it's easier to grow dividends when earnings per share are improving. If earnings fall far enough, the company could be forced to cut its dividend. This is why it's a relief to see IBJ earnings per share are up 9.5% per annum over the last five years. Earnings per share have been increasing steadily and management is reinvesting almost all of the profits back into the business. If profits are reinvested effectively, this could be a bullish combination for future earnings and dividends.

Another key way to measure a company's dividend prospects is by measuring its historical rate of dividend growth. Since the start of our data, eight years ago, IBJ has lifted its dividend by approximately 3.7% a year on average. It's encouraging to see the company lifting dividends while earnings are growing, suggesting at least some corporate interest in rewarding shareholders.

The Bottom Line

Has IBJ got what it takes to maintain its dividend payments? Earnings per share growth has been growing somewhat, and IBJ is paying out less than half its earnings and cash flow as dividends. This is interesting for a few reasons, as it suggests management may be reinvesting heavily in the business, but it also provides room to increase the dividend in time. We would prefer to see earnings growing faster, but the best dividend stocks over the long term typically combine significant earnings per share growth with a low payout ratio, and IBJ is halfway there. There's a lot to like about IBJ, and we would prioritise taking a closer look at it.

Wondering what the future holds for IBJ? See what the two analysts we track are forecasting, with this visualisation of its historical and future estimated earnings and cash flow

Generally, we wouldn't recommend just buying the first dividend stock you see. Here's a curated list of interesting stocks that are strong dividend payers.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:6071

Excellent balance sheet and fair value.

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.4% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|17.8% undervalued

TI

Community Contributor