Advertisement

- South Korea

- /

- Semiconductors

- /

- KOSE:A195870

3 Asian Stocks That Might Be Trading Below Estimated Value In November 2025

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate a landscape marked by mixed performances and strategic economic decisions, Asian equities are garnering attention amid easing U.S.-China trade tensions and Japan's record stock market highs. In this environment, identifying undervalued stocks becomes crucial for investors looking to capitalize on potential growth opportunities that may arise from favorable regional developments.

Top 10 Undervalued Stocks Based On Cash Flows In Asia

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| T'Way Air (KOSE:A091810) | ₩1711.00 | ₩3398.49 | 49.7% |

| Takara Bio (TSE:4974) | ¥914.00 | ¥1815.23 | 49.6% |

| New Zealand King Salmon Investments (NZSE:NZK) | NZ$0.196 | NZ$0.39 | 49.2% |

| Meitu (SEHK:1357) | HK$8.68 | HK$17.27 | 49.8% |

| LianChuang Electronic TechnologyLtd (SZSE:002036) | CN¥10.06 | CN¥20.02 | 49.7% |

| EverProX Technologies (SZSE:300548) | CN¥93.50 | CN¥185.29 | 49.5% |

| Daiichi Sankyo Company (TSE:4568) | ¥3369.00 | ¥6631.69 | 49.2% |

| COVER (TSE:5253) | ¥1838.00 | ¥3673.18 | 50% |

| Chongqing Baiya Sanitary Products (SZSE:003006) | CN¥22.18 | CN¥43.54 | 49.1% |

| Alibaba Health Information Technology (SEHK:241) | HK$5.68 | HK$11.29 | 49.7% |

Here's a peek at a few of the choices from the screener.

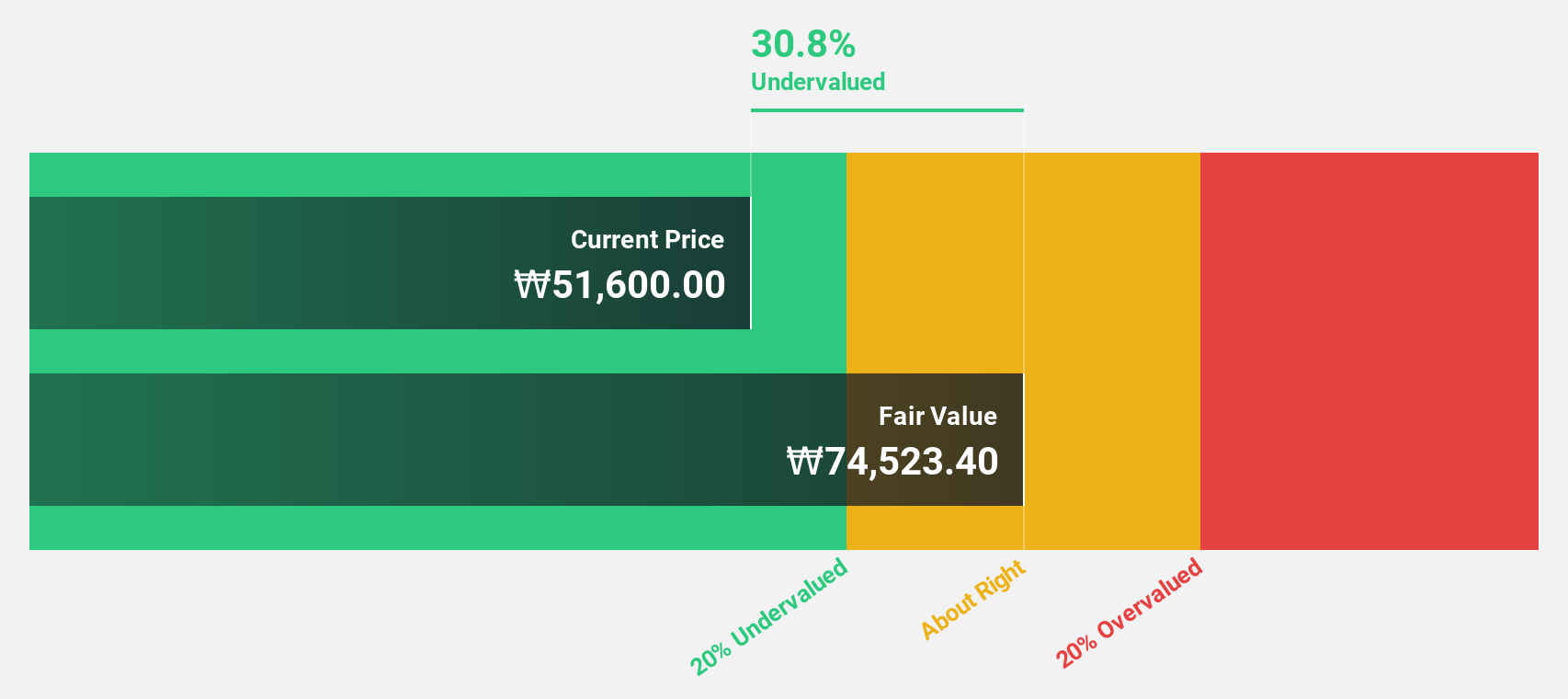

HAESUNG DS (KOSE:A195870)

Overview: HAESUNG DS Co., Ltd. manufactures and sells semiconductor components both in South Korea and internationally, with a market cap of ₩931.60 billion.

Operations: The company's revenue primarily comes from its semiconductor segment, generating ₩589.48 billion.

Estimated Discount To Fair Value: 24%

HAESUNG DS is trading at ₩54,800, significantly below its estimated fair value of ₩72,073.21. Despite a volatile share price and lower profit margins compared to last year, the stock's earnings are projected to grow substantially at 54.6% annually over the next three years—outpacing both revenue growth and market averages in Korea. However, its dividend yield of 1.46% lacks coverage by free cash flows, highlighting potential sustainability issues despite strong growth prospects.

- Our growth report here indicates HAESUNG DS may be poised for an improving outlook.

- Delve into the full analysis health report here for a deeper understanding of HAESUNG DS.

Round One (TSE:4680)

Overview: Round One Corporation operates indoor leisure complex facilities and has a market cap of ¥289.12 billion.

Operations: Revenue Segments (in millions of ¥): Amusement: ¥47,500, Bowling: ¥38,200, Karaoke: ¥19,600.

Estimated Discount To Fair Value: 33%

Round One Corporation is trading at ¥1,102.5, notably below its estimated fair value of ¥1,645.11, presenting a good relative value compared to peers and industry standards. Despite recent volatility in share price and slower revenue growth forecasts of 8.4% annually, the company's earnings are expected to grow at 12.7% per year—exceeding Japan's market average of 7.8%. Recent sales data show mixed results across regions but overall positive growth trends year-to-date in both Japan and the USA markets.

- Upon reviewing our latest growth report, Round One's projected financial performance appears quite optimistic.

- Unlock comprehensive insights into our analysis of Round One stock in this financial health report.

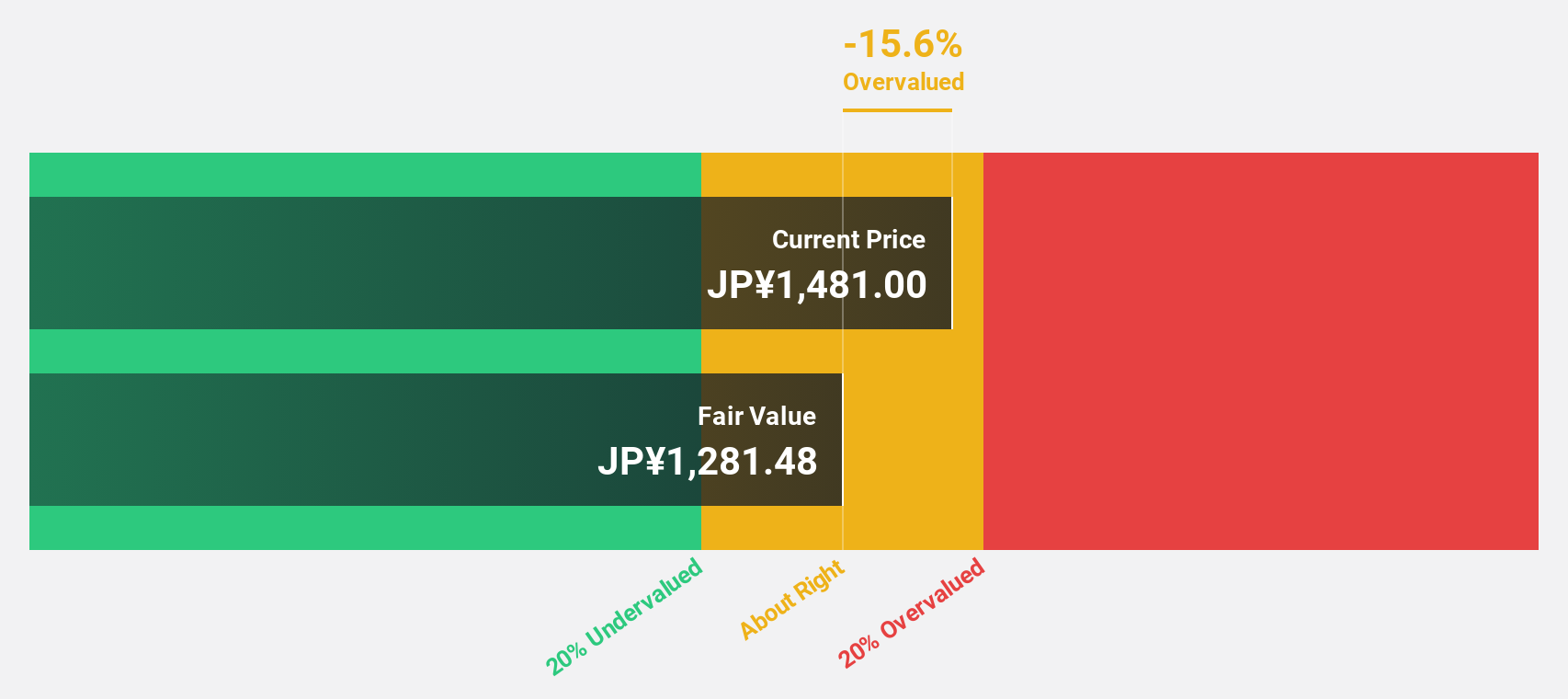

MEC (TSE:4971)

Overview: MEC Company Ltd. focuses on the research, development, production, and sale of chemicals, equipment, and materials for printed circuit boards across Japan, Taiwan, Hong Kong, China, Thailand, and Europe with a market cap of ¥81.81 billion.

Operations: The company's revenue segments are ¥12.06 billion from Japan, ¥3.65 billion from China, ¥3.47 billion from Taiwan, ¥2.49 billion from Hong Kong, ¥1.28 billion from Europe, and ¥910.30 million from Thailand.

Estimated Discount To Fair Value: 28.4%

MEC Company Ltd. is trading at ¥4,480, significantly below its estimated fair value of ¥6,261.27, suggesting it may be undervalued based on cash flows. Despite a volatile share price recently and lower profit margins than last year, earnings are forecast to grow 22.59% annually—outpacing the Japanese market average of 7.8%. Recent strategic alliances in semiconductor packaging could enhance future cash flow potential as demand for organic interposers rises globally.

- The growth report we've compiled suggests that MEC's future prospects could be on the up.

- Click here to discover the nuances of MEC with our detailed financial health report.

Where To Now?

- Access the full spectrum of 272 Undervalued Asian Stocks Based On Cash Flows by clicking on this link.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if HAESUNG DS might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About KOSE:A195870

HAESUNG DS

Manufactures and sells semiconductor components in South Korea and internationally.

Flawless balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|7.5% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|25.4% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.6% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.0% undervalued

DA

Community Contributor