Advertisement

- Japan

- /

- Hospitality

- /

- TSE:3350

Metaplanet (TSE:3350) Valuation Check as Capital Structure Overhaul and EVO FUND Deal Move Forward

Simply Wall St

Reviewed by Simply Wall St

Metaplanet (TSE:3350) just put a major capital structure revamp on the table, with its board set to weigh new class B preferred shares, cancel older stock acquisition rights, and strike a fresh deal with EVO FUND.

See our latest analysis for Metaplanet.

Those capital moves come after a volatile stretch for Metaplanet, with the share price at ¥392 following a sharp 1 day share price return of 9.8 percent, a 30 day share price return of minus 20.16 percent, and a standout 3 year total shareholder return of 653.85 percent, signaling that longer term momentum, while choppy, has still been powerful.

If this kind of high octane story has your attention, it might be worth seeing what else is out there by exploring fast growing stocks with high insider ownership.

With revenue and earnings still growing fast, but the share price sharply off recent highs, investors face a key question: Is Metaplanet trading at a rare discount, or is the market already pricing in its next leg of growth?

Price-to-Earnings of 22.1x: Is it justified?

Metaplanet trades on a Price-to-Earnings ratio of 22.1 times at a last close of ¥392, suggesting the market is not aggressively overpaying versus peers.

The Price-to-Earnings multiple compares the current share price to per share earnings, a key lens for a business like Metaplanet where profits have only recently turned positive but are forecast to grow quickly.

Here, the 22.1 times earnings multiple sits slightly below the broader Japan hospitality industry average of 23.1 times. This hints that investors are not paying a premium despite forecasts for revenue to grow at nearly triple digit rates and earnings to expand significantly faster than the wider market. At the same time, our fair Price-to-Earnings estimate of 44.9 times is far above where the stock currently trades, which implies substantial room for re rating if those growth expectations are delivered.

Relative to its sector, Metaplanet looks modestly cheaper than the typical hospitality peer on earnings, yet materially below the level suggested by our fair ratio model. This frames where the market multiple could gravitate if consensus growth trends play out.

Explore the SWS fair ratio for Metaplanet

Result: Price-to-Earnings of 22.1x (UNDERVALUED)

However, investors should watch for execution setbacks across its Bitcoin Treasury and Web3 initiatives, or a prolonged share price slump that undermines management’s capital raising flexibility.

Find out about the key risks to this Metaplanet narrative.

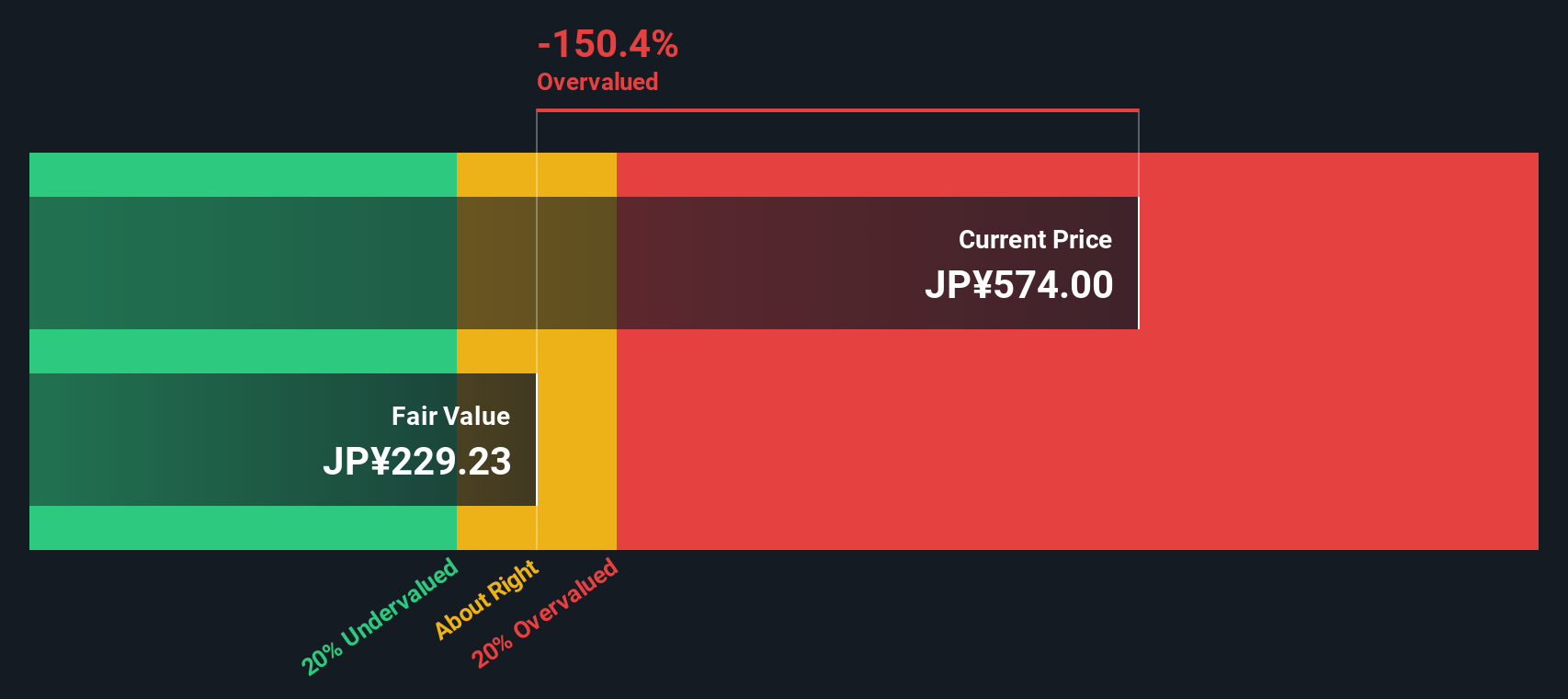

Another View: Our DCF Flags Overvaluation

While earnings multiples hint at upside, our DCF model paints a starker picture, putting fair value near ¥35.69, far below the ¥392 share price. That implies Metaplanet screens as heavily overvalued on cash flows and raises the question of which signal investors might prioritize.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Metaplanet for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 920 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Metaplanet Narrative

If you are not convinced by this perspective, or would rather dig into the numbers yourself and shape your own view in minutes, Do it your way.

A great starting point for your Metaplanet research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Ready for more investment ideas?

Before you move on, lock in your next potential opportunity with hand picked stock ideas from our powerful Simply Wall St Screener, built to surface what others miss.

- Capture early momentum by reviewing these 3571 penny stocks with strong financials, which combine small market caps with balance sheet strength and room for upside.

- Capitalize on the AI wave with these 25 AI penny stocks, where innovative businesses are turning cutting edge algorithms into real revenue growth.

- Strengthen your income strategy by focusing on these 14 dividend stocks with yields > 3%, featuring companies with yields above 3 percent that can help anchor total returns.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:3350

Metaplanet

Engages in hotel management operation and development in Japan.

Flawless balance sheet with high growth potential.

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.4% undervalued

35 followersusers have followed this narrative

6 commentsusers have commented on this narrative

10 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$126.1% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$244.5% overvalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

FU

FundamentallySarcastic on Credit Corp Group ·

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Fair Value:AU$12.6411.4% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on Alphabet ·

Positioned globally, partnered locally

Fair Value:US$390.1918.1% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JO

JohnJ on Worldline ·

When will fraudsters be investigated in depth. Fraud was ongoing in France too.

Fair Value:€0.5190.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

113 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3928.3% undervalued

952 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3406.0% undervalued

148 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative