Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies Asakuma Co.,Ltd (TYO:7678) makes use of debt. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first step when considering a company's debt levels is to consider its cash and debt together.

See our latest analysis for AsakumaLtd

What Is AsakumaLtd's Net Debt?

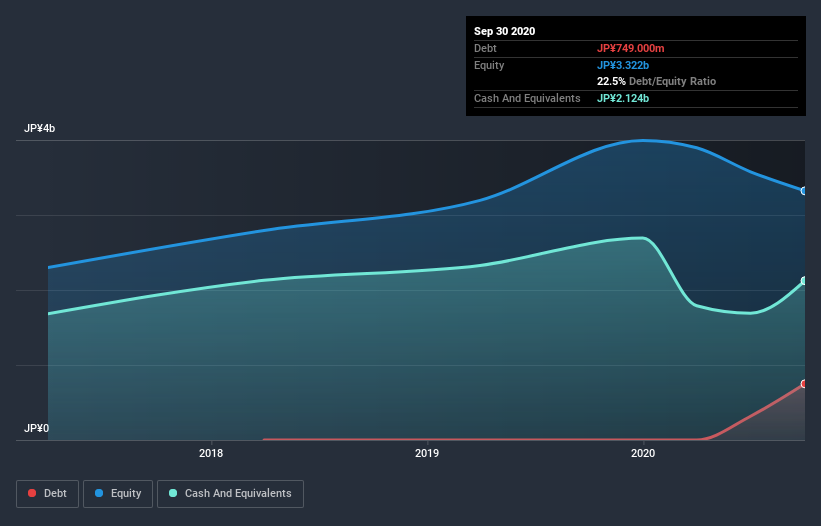

The image below, which you can click on for greater detail, shows that at September 2020 AsakumaLtd had debt of JP¥670.0m, up from none in one year. But on the other hand it also has JP¥2.12b in cash, leading to a JP¥1.45b net cash position.

How Strong Is AsakumaLtd's Balance Sheet?

We can see from the most recent balance sheet that AsakumaLtd had liabilities of JP¥1.19b falling due within a year, and liabilities of JP¥649.0m due beyond that. Offsetting this, it had JP¥2.12b in cash and JP¥226.0m in receivables that were due within 12 months. So it actually has JP¥510.0m more liquid assets than total liabilities.

This surplus suggests that AsakumaLtd has a conservative balance sheet, and could probably eliminate its debt without much difficulty. Succinctly put, AsakumaLtd boasts net cash, so it's fair to say it does not have a heavy debt load! The balance sheet is clearly the area to focus on when you are analysing debt. But it is AsakumaLtd's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

In the last year AsakumaLtd had a loss before interest and tax, and actually shrunk its revenue by 22%, to JP¥7.3b. To be frank that doesn't bode well.

So How Risky Is AsakumaLtd?

By their very nature companies that are losing money are more risky than those with a long history of profitability. And in the last year AsakumaLtd had an earnings before interest and tax (EBIT) loss, truth be told. Indeed, in that time it burnt through JP¥711m of cash and made a loss of JP¥620m. Given it only has net cash of JP¥1.45b, the company may need to raise more capital if it doesn't reach break-even soon. Overall, its balance sheet doesn't seem overly risky, at the moment, but we're always cautious until we see the positive free cash flow. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. For instance, we've identified 2 warning signs for AsakumaLtd (1 makes us a bit uncomfortable) you should be aware of.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

When trading AsakumaLtd or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TSE:7678

AsakumaLtd

Together with its subsidiary Asakuma Succession Co., Ltd., engages in the restaurant management and franchise business in Japan.

Excellent balance sheet with questionable track record.