- India

- /

- Basic Materials

- /

- NSEI:RAMCOIND

Unearthing None's Undiscovered Gems In November 2024

Reviewed by Simply Wall St

As global markets react to a "red sweep" in the U.S. elections, optimism about growth and tax reforms has propelled major indices to new heights, with the small-cap Russell 2000 Index leading gains but still shy of its record high. In this buoyant yet uncertain environment, identifying stocks that possess strong fundamentals and resilience can be key to uncovering potential undiscovered gems amidst shifting economic policies and market dynamics.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Lion Rock Group | 16.91% | 14.33% | 10.15% | ★★★★★★ |

| PSC | 17.90% | 2.07% | 13.38% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Mandiri Herindo Adiperkasa | NA | 20.72% | 11.08% | ★★★★★★ |

| Impellam Group | 31.12% | -5.43% | -6.86% | ★★★★★★ |

| Bank Ganesha | NA | 25.03% | 70.72% | ★★★★★★ |

| Citra Tubindo | NA | 9.17% | 14.32% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

| Wilson | 64.79% | 30.09% | 68.29% | ★★★★☆☆ |

Let's review some notable picks from our screened stocks.

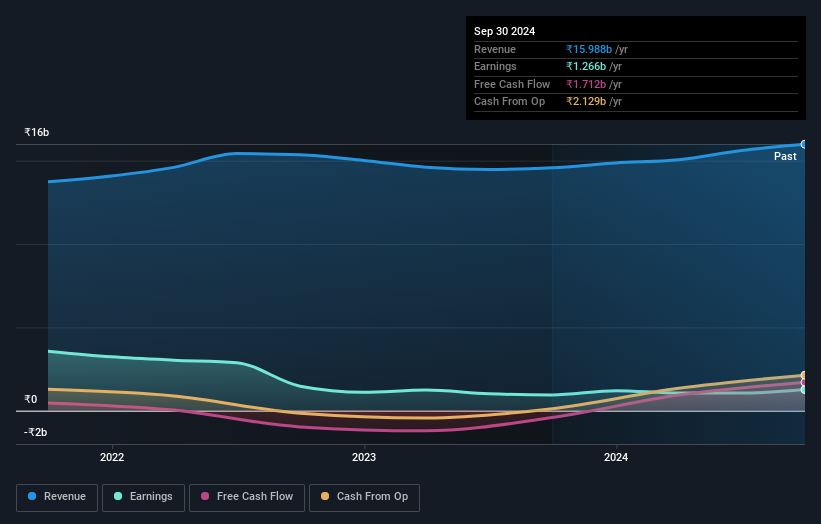

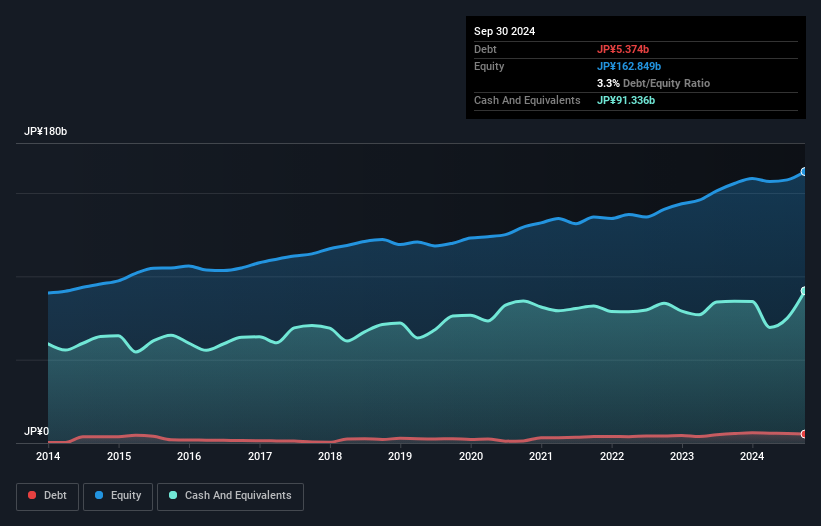

Ramco Industries (NSEI:RAMCOIND)

Simply Wall St Value Rating: ★★★★★★

Overview: Ramco Industries Limited operates in the building products, textiles, and power generation sectors in India with a market capitalization of ₹25.61 billion.

Operations: Ramco Industries generates revenue primarily from its building products, textiles, and power generation sectors. The company has a market capitalization of ₹25.61 billion.

Ramco Industries, a promising player in the market, has shown impressive financial resilience. With its interest payments well covered by EBIT at 17.2 times, it demonstrates strong operational efficiency. The company's net debt to equity ratio stands at a satisfactory 1%, reflecting prudent financial management over the past five years as it reduced its debt to equity from 4.2% to 3.2%. Recent earnings growth of 33.7% outpaced the industry average of 15.1%, and with shares trading at 84% below estimated fair value, Ramco's potential for value appreciation is noteworthy amidst ongoing strategic developments and leadership changes.

- Click to explore a detailed breakdown of our findings in Ramco Industries' health report.

Explore historical data to track Ramco Industries' performance over time in our Past section.

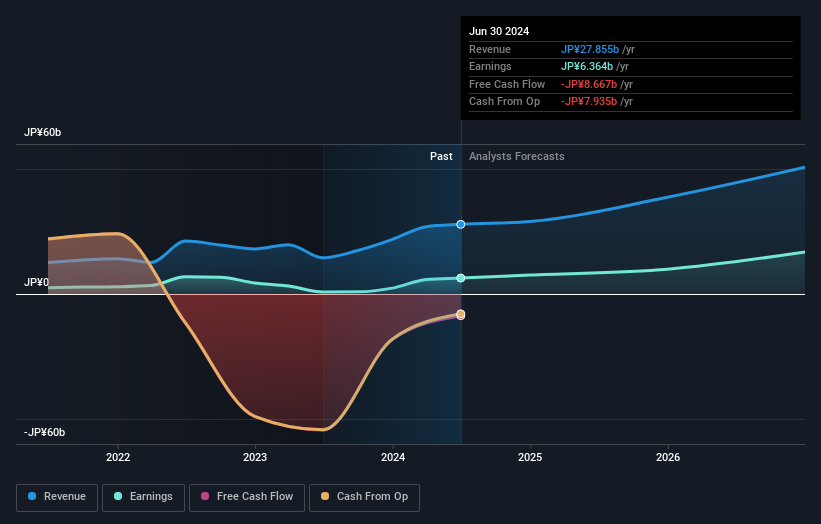

Japan Investment Adviser (TSE:7172)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Japan Investment Adviser Co., Ltd. offers a range of financial solutions in Japan and has a market capitalization of approximately ¥71.07 billion.

Operations: The company generates revenue primarily from its Finance Solution segment, which contributed ¥28.10 billion.

Japan Investment Adviser, a smaller player in the financial sector, has shown remarkable earnings growth of 289.8% over the past year, outpacing the industry average of 22.7%. However, its net debt to equity ratio remains high at 159.2%, suggesting significant leverage. Despite trading at 35% below estimated fair value and having high-quality earnings with EBIT covering interest payments by 7.8 times, recent corporate guidance lowered expectations due to non-operating exchange losses from yen appreciation. The core Operating Lease Business performed well but couldn't offset these losses entirely, impacting ordinary and net income expectations for the year ending December 2024.

- Dive into the specifics of Japan Investment Adviser here with our thorough health report.

Learn about Japan Investment Adviser's historical performance.

Kato Sangyo (TSE:9869)

Simply Wall St Value Rating: ★★★★★☆

Overview: Kato Sangyo Co., Ltd. operates in the general food wholesaling business both in Japan and internationally, with a market capitalization of ¥132.41 billion.

Operations: Kato Sangyo generates revenue primarily through its food wholesaling operations in Japan and abroad. The company reported a market capitalization of ¥132.41 billion.

Kato Sangyo, a nimble player in the market, has shown impressive growth with earnings rising by 20.5% over the past year, outpacing its industry peers. The company trades at a 14% discount to its estimated fair value, suggesting potential for value-seeking investors. Despite an increase in its debt-to-equity ratio from 2.1 to 3.3 over five years, Kato Sangyo's financial health remains strong with more cash than total debt and robust interest coverage. A notable ¥4.6 billion one-off gain has influenced recent results but doesn't overshadow the company's consistent profitability and solid cash runway prospects moving forward.

- Get an in-depth perspective on Kato Sangyo's performance by reading our health report here.

Review our historical performance report to gain insights into Kato Sangyo's's past performance.

Next Steps

- Explore the 4670 names from our Undiscovered Gems With Strong Fundamentals screener here.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NSEI:RAMCOIND

Ramco Industries

Engages in the building products, textiles, and power generation businesses in India.

Flawless balance sheet, good value and pays a dividend.