- Japan

- /

- Food and Staples Retail

- /

- TSE:5856

Is Life Intelligent Enterprise HoldingsLtd (TSE:5856) Using Too Much Debt?

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We can see that Life Intelligent Enterprise Holdings Co.,Ltd. (TSE:5856) does use debt in its business. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for Life Intelligent Enterprise HoldingsLtd

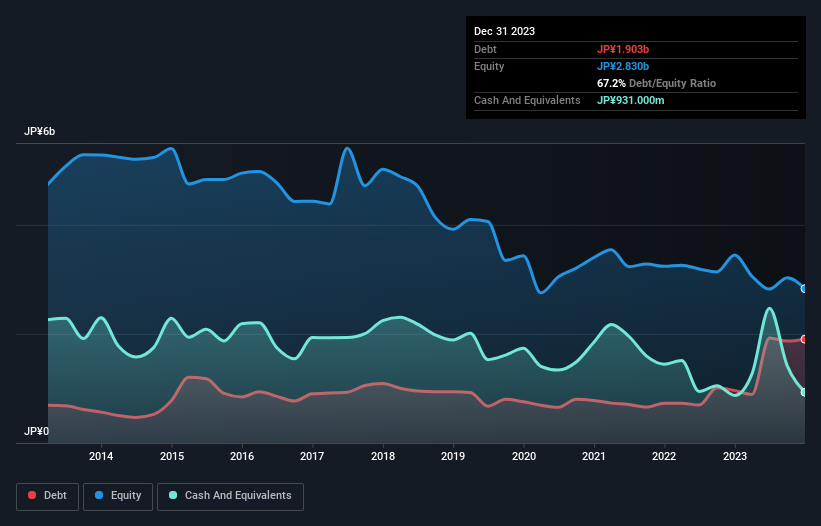

How Much Debt Does Life Intelligent Enterprise HoldingsLtd Carry?

As you can see below, at the end of December 2023, Life Intelligent Enterprise HoldingsLtd had JP¥1.90b of debt, up from JP¥962.0m a year ago. Click the image for more detail. On the flip side, it has JP¥931.0m in cash leading to net debt of about JP¥972.0m.

A Look At Life Intelligent Enterprise HoldingsLtd's Liabilities

We can see from the most recent balance sheet that Life Intelligent Enterprise HoldingsLtd had liabilities of JP¥3.13b falling due within a year, and liabilities of JP¥828.0m due beyond that. Offsetting these obligations, it had cash of JP¥931.0m as well as receivables valued at JP¥1.54b due within 12 months. So its liabilities total JP¥1.49b more than the combination of its cash and short-term receivables.

This deficit isn't so bad because Life Intelligent Enterprise HoldingsLtd is worth JP¥3.37b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt. There's no doubt that we learn most about debt from the balance sheet. But it is Life Intelligent Enterprise HoldingsLtd's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

In the last year Life Intelligent Enterprise HoldingsLtd wasn't profitable at an EBIT level, but managed to grow its revenue by 8.8%, to JP¥19b. That rate of growth is a bit slow for our taste, but it takes all types to make a world.

Caveat Emptor

Importantly, Life Intelligent Enterprise HoldingsLtd had an earnings before interest and tax (EBIT) loss over the last year. Its EBIT loss was a whopping JP¥885m. Considering that alongside the liabilities mentioned above does not give us much confidence that company should be using so much debt. So we think its balance sheet is a little strained, though not beyond repair. However, it doesn't help that it burned through JP¥782m of cash over the last year. So in short it's a really risky stock. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. For example, we've discovered 3 warning signs for Life Intelligent Enterprise HoldingsLtd (1 is a bit concerning!) that you should be aware of before investing here.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:5856

Life Intelligent Enterprise HoldingsLtd

Life Intelligent Enterprise Holdings Co.,Ltd.

Slight with mediocre balance sheet.

Market Insights

Community Narratives