- Japan

- /

- Food and Staples Retail

- /

- TSE:3549

Kusuri No Aoki Holdings Co., Ltd. Just Missed EPS By 6.6%: Here's What Analysts Think Will Happen Next

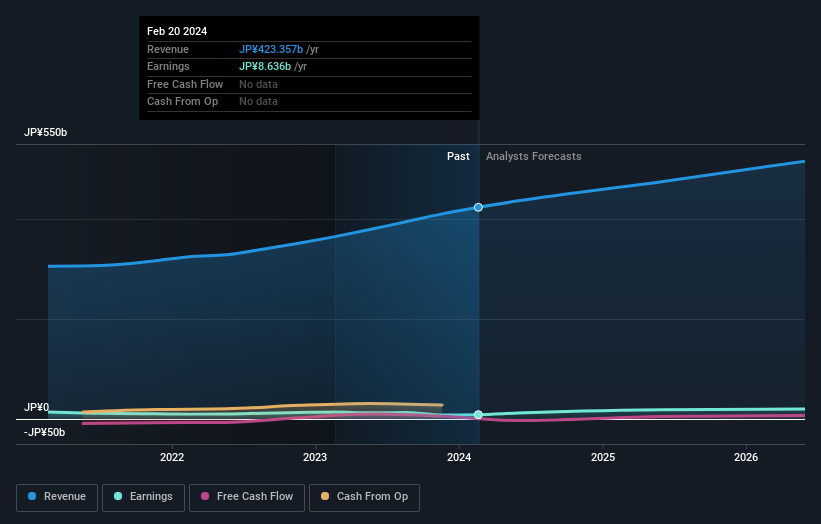

Shareholders might have noticed that Kusuri No Aoki Holdings Co., Ltd. (TSE:3549) filed its quarterly result this time last week. The early response was not positive, with shares down 5.9% to JP¥2,977 in the past week. It looks like the results were a bit of a negative overall. While revenues of JP¥111b were in line with analyst predictions, statutory earnings were less than expected, missing estimates by 6.6% to hit JP¥51.21 per share. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. So we gathered the latest post-earnings forecasts to see what estimates suggest is in store for next year.

Check out our latest analysis for Kusuri No Aoki Holdings

Following the latest results, Kusuri No Aoki Holdings' five analysts are now forecasting revenues of JP¥474.6b in 2025. This would be a solid 12% improvement in revenue compared to the last 12 months. Per-share earnings are expected to bounce 105% to JP¥187. Yet prior to the latest earnings, the analysts had been anticipated revenues of JP¥472.6b and earnings per share (EPS) of JP¥187 in 2025. The consensus analysts don't seem to have seen anything in these results that would have changed their view on the business, given there's been no major change to their estimates.

It will come as no surprise then, to learn that the consensus price target is largely unchanged at JP¥3,683. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. Currently, the most bullish analyst values Kusuri No Aoki Holdings at JP¥4,000 per share, while the most bearish prices it at JP¥3,333. The narrow spread of estimates could suggest that the business' future is relatively easy to value, or thatthe analysts have a strong view on its prospects.

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. The period to the end of 2025 brings more of the same, according to the analysts, with revenue forecast to display 9.6% growth on an annualised basis. That is in line with its 9.7% annual growth over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to see their revenues grow 2.5% per year. So although Kusuri No Aoki Holdings is expected to maintain its revenue growth rate, it's definitely expected to grow faster than the wider industry.

The Bottom Line

The most important thing to take away is that there's been no major change in sentiment, with the analysts reconfirming that the business is performing in line with their previous earnings per share estimates. Fortunately, they also reconfirmed their revenue numbers, suggesting that it's tracking in line with expectations. Additionally, our data suggests that revenue is expected to grow faster than the wider industry. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

With that in mind, we wouldn't be too quick to come to a conclusion on Kusuri No Aoki Holdings. Long-term earnings power is much more important than next year's profits. At Simply Wall St, we have a full range of analyst estimates for Kusuri No Aoki Holdings going out to 2026, and you can see them free on our platform here..

You still need to take note of risks, for example - Kusuri No Aoki Holdings has 1 warning sign we think you should be aware of.

Valuation is complex, but we're here to simplify it.

Discover if Kusuri No Aoki Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:3549

Kusuri No Aoki Holdings

Engages in the retail of pharmaceuticals, cosmetics, and daily goods in Japan.

Excellent balance sheet with moderate growth potential.