- Japan

- /

- Food and Staples Retail

- /

- TSE:3382

We Think Seven & i Holdings (TSE:3382) Can Stay On Top Of Its Debt

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that Seven & i Holdings Co., Ltd. (TSE:3382) does use debt in its business. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we think about a company's use of debt, we first look at cash and debt together.

View our latest analysis for Seven & i Holdings

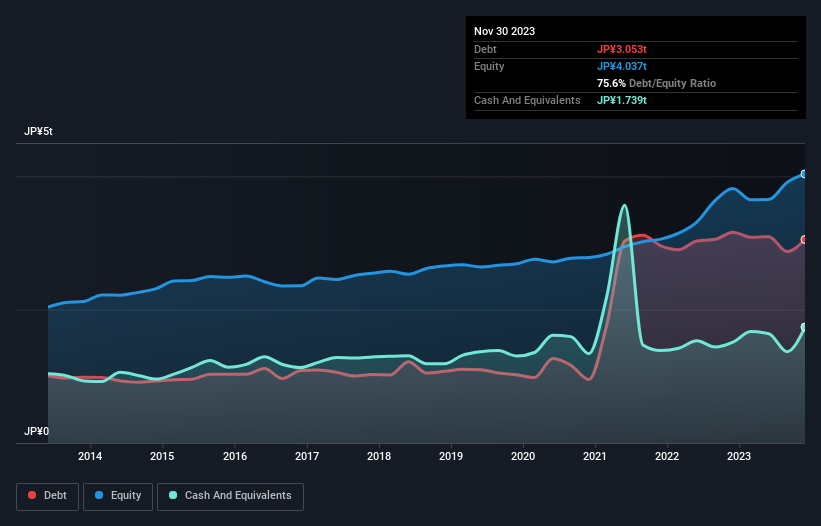

What Is Seven & i Holdings's Debt?

As you can see below, Seven & i Holdings had JP¥3.05t of debt, at November 2023, which is about the same as the year before. You can click the chart for greater detail. However, because it has a cash reserve of JP¥1.74t, its net debt is less, at about JP¥1.31t.

How Strong Is Seven & i Holdings' Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Seven & i Holdings had liabilities of JP¥3.30t due within 12 months and liabilities of JP¥3.76t due beyond that. Offsetting this, it had JP¥1.74t in cash and JP¥598.1b in receivables that were due within 12 months. So it has liabilities totalling JP¥4.72t more than its cash and near-term receivables, combined.

This deficit is considerable relative to its very significant market capitalization of JP¥5.60t, so it does suggest shareholders should keep an eye on Seven & i Holdings' use of debt. Should its lenders demand that it shore up the balance sheet, shareholders would likely face severe dilution.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Seven & i Holdings has a low net debt to EBITDA ratio of only 1.3. And its EBIT covers its interest expense a whopping 17.4 times over. So you could argue it is no more threatened by its debt than an elephant is by a mouse. The good news is that Seven & i Holdings has increased its EBIT by 8.8% over twelve months, which should ease any concerns about debt repayment. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Seven & i Holdings can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the most recent three years, Seven & i Holdings recorded free cash flow worth 75% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This cold hard cash means it can reduce its debt when it wants to.

Our View

Seven & i Holdings's interest cover was a real positive on this analysis, as was its conversion of EBIT to free cash flow. Having said that, its level of total liabilities somewhat sensitizes us to potential future risks to the balance sheet. Considering this range of data points, we think Seven & i Holdings is in a good position to manage its debt levels. Having said that, the load is sufficiently heavy that we would recommend any shareholders keep a close eye on it. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. We've identified 1 warning sign with Seven & i Holdings , and understanding them should be part of your investment process.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:3382

Seven & i Holdings

Operates convenience stores, superstores, department stores, supermarkets, and specialty stores.

Moderate growth potential with mediocre balance sheet.