Advertisement

ASICS (TSE:7936): Evaluating Valuation After Recent Share Price Dip

Simply Wall St

Reviewed by Simply Wall St

ASICS (TSE:7936) recently caught the attention of investors following a noticeable dip in its share price over the past month. The company, known globally for its sportswear and running shoes, has seen its stock performance shift even though its business fundamentals have remained steady.

See our latest analysis for ASICS.

While ASICS has faced a retreat in its share price over the past month, the broader trend remains impressive, with a year-to-date share price return of 22.29% and a remarkable total shareholder return of 25.4% over the last year. Long-term holders have enjoyed extraordinary gains, posting a 415.75% three-year total shareholder return. This suggests that although recent momentum has cooled, growth potential is not out of reach for patient investors.

If ASICS’s long-term success has you thinking bigger, it could be the perfect time to broaden your perspective and discover fast growing stocks with high insider ownership

With strong fundamentals and shares trading about 23% below analyst price targets, the real question for investors is whether ASICS is currently undervalued or if the market has already accounted for its future growth prospects.

Price-to-Earnings of 31.5x: Is it justified?

At a last close price of ¥3,741, ASICS is trading at a price-to-earnings (P/E) ratio of 31.5x, making it appear significantly more expensive than its Japanese luxury sector peers.

The price-to-earnings ratio compares a company's share price to its annual earnings per share, helping investors understand how much they are paying for each yen of profit. For companies like ASICS, active in a branded consumer segment with strong recognition, a high P/E could signal expectations of robust future earnings growth or premium brand value.

However, this P/E ratio stands well above both the Japanese luxury industry average of 14.8x and the peer group average of 14.8x. It is also notably higher than the estimated fair price-to-earnings ratio of 23.1x. The market is currently attributing a premium to ASICS far beyond sector norms, which may indicate enthusiastic sentiment regarding its growth prospects. This also highlights the elevated expectations already reflected in the share price.

Explore the SWS fair ratio for ASICS

Result: Price-to-Earnings of 31.5x (OVERVALUED)

However, slowing revenue and net income growth, or weakening consumer demand, could quickly challenge the optimism currently priced into ASICS shares.

Find out about the key risks to this ASICS narrative.

Another View: SWS DCF Model Weighs In

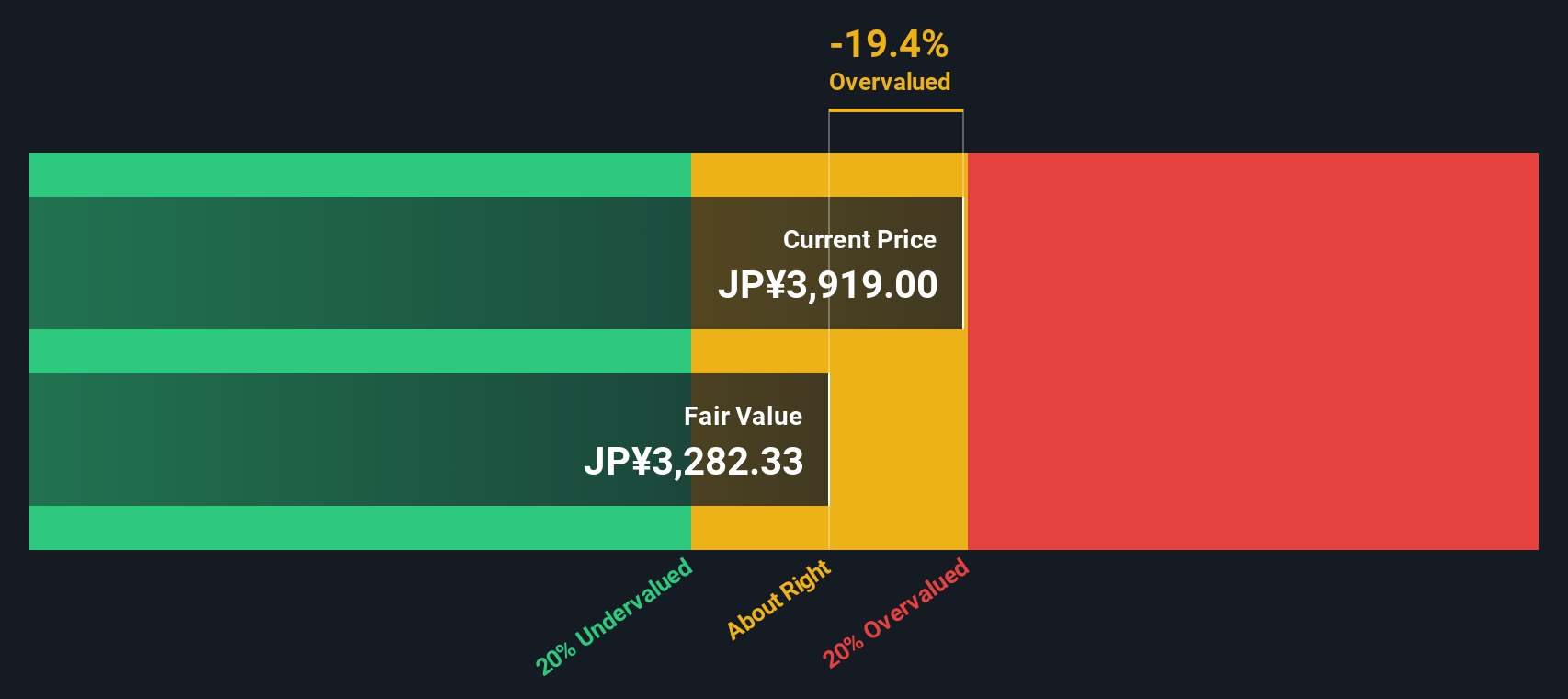

While ASICS shares appear expensive compared to industry multiples, our DCF model provides a different perspective. According to the SWS DCF model, the current price of ¥3,741 is above what we estimate as fair value at ¥3,286.39. This suggests the shares may actually be trading at a 13.9% premium. Does this challenge the idea that elevated multiples are justified by future growth, or does it simply reflect high investor confidence?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out ASICS for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 920 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own ASICS Narrative

If you want a different perspective or enjoy diving into the numbers yourself, you can shape your story from the ground up in just minutes with Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding ASICS.

Looking for more investment ideas?

Act now to spot tomorrow’s winners. Simply Wall Street's screeners connect you to fresh opportunities before they hit the mainstream, helping you stay ahead.

- Capture potential growth by targeting these 920 undervalued stocks based on cash flows that appear poised for a rebound based on strong fundamentals and attractive valuations.

- Tap into breakthrough technologies and invest with confidence by reviewing these 25 AI penny stocks that are changing the game in artificial intelligence.

- Secure steady income from these 15 dividend stocks with yields > 3% offering reliable yields above 3%, ideal for building a resilient long-term portfolio.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:7936

ASICS

Manufactures and sells sporting goods in Japan and internationally.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

138 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

931 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative