Advertisement

- Japan

- /

- Semiconductors

- /

- TSE:3436

Casio ComputerLtd (TSE:6952) Expands G-SHOCK Line with ITZY Collaboration and Strong Earnings Growth

Simply Wall St

Reviewed by Simply Wall St

Casio ComputerLtd (TSE:6952) is making headlines with its innovative collaborations, such as the recent partnership with ITZY for the G-SHOCK brand, which underscores its strategic focus on capturing new markets. Despite impressive earnings growth and a strong dividend yield, Casio faces challenges with potential overvaluation and modest revenue growth projections. Readers should expect a detailed analysis of Casio's financial health, strategic initiatives, and the competitive pressures it faces, along with insights into future growth prospects and market risks.

Click here and access our complete analysis report to understand the dynamics of Casio ComputerLtd.

Unique Capabilities Enhancing Casio's Market Position

Casio has demonstrated strong financial health, with earnings growing by 18.9% over the past year, significantly outperforming the Consumer Durables industry. This growth is complemented by a forecasted earnings increase of 12.8% per year, surpassing the JP market average of 8.8%. The company's consistent dividend payments, yielding 3.94%, place it among the top 25% of dividend payers in Japan. Moreover, Casio's strategic alliances, such as the collaboration with ITZY for the G-SHOCK brand, highlight its innovative approach to capturing new markets. The leadership team, with an average tenure of 3.8 years, has effectively leveraged these strengths to maintain a healthy profit margin of 20%, as noted by CEO Yuichi Masuda in the latest earnings call.

Vulnerabilities Impacting Casio

However, the company's Price-To-Earnings Ratio of 17.8x suggests potential overvaluation compared to industry and peer averages of 11.8x and 14.2x, respectively. This financial challenge is further compounded by a low forecasted Return on Equity of 8.8%, which falls short of industry benchmarks. Additionally, revenue growth is projected at a modest 2% per year, trailing behind the JP market average of 4.2%. The past five years have seen a 9.9% annual decline in earnings, indicating underlying vulnerabilities that need addressing. The increased operational costs, as highlighted by CFO Seiji Tamura, also impact overall profitability.

Future Prospects for Casio in the Market

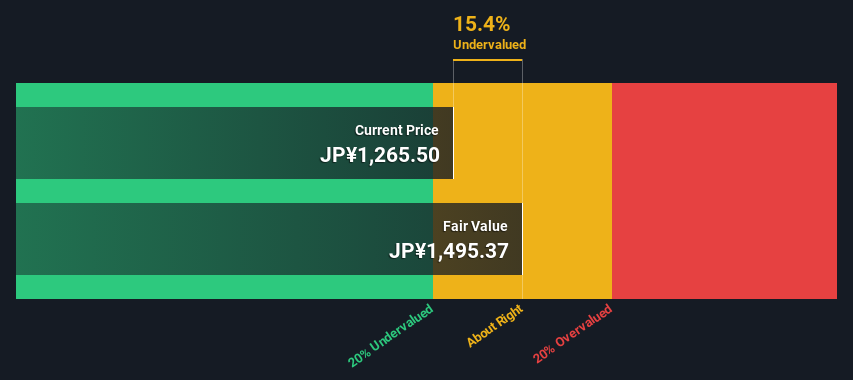

Casio's potential for revenue growth is promising if it can exceed the current forecast of 2% annually. Trading at 24.9% below the estimated fair value presents an opportunity for price appreciation, attracting investors seeking stable income through continued dividend growth. Strategic initiatives, such as expanding digital marketing and increasing presence in Asian markets, are expected to drive further growth. The trend towards sustainability offers a unique opportunity for innovation, as emphasized by Masuda, positioning Casio to capitalize on emerging market trends.

Competitive Pressures and Market Risks Facing Casio

Nonetheless, Casio faces significant threats from increased competition and economic uncertainties in key markets. These factors could impact market share and growth projections, as noted by Tamura. The risk of economic downturns affecting consumer durables remains a concern, potentially hindering future growth. Additionally, changes in regulatory frameworks could affect operational strategies and cost structures, posing further challenges. One-off gains impacting financial results may distort the sustainability of earnings, limiting investor interest in the long term.

Conclusion

Casio's strong earnings growth and high dividend yield demonstrate its capacity to outperform its peers in the Consumer Durables industry, positioning it as an attractive option for income-focused investors. However, its Price-To-Earnings Ratio of 17.8x, higher than industry and peer averages, suggests that the market may have high expectations for the company, which could be risky if growth does not meet forecasts. The company's strategic initiatives, such as digital marketing expansion and focus on sustainability, offer potential for future revenue growth, especially in Asian markets. Nonetheless, Casio must address its low forecasted Return on Equity and modest revenue growth projections to sustain investor confidence, particularly in the face of competitive pressures and economic uncertainties.

Next Steps

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Simply Wall St and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

About TSE:3436

Sumco

Manufactures and sells silicon wafers for the semiconductor industry in Japan, the United States, China, Taiwan, Korea, and internationally.

Reasonable growth potential with mediocre balance sheet.

Market Insights

Advertisement

Community Narratives

Pole position to benefit from GENIUS Act

Fair Value US$233.04|58.8% undervalued

CH

Community Contributor

IREN will transform from bitcoin miner to leader in AI infrastructure

Fair Value US$21.48|17.5% undervalued

KA

Community Contributor

Behind the Assay: XRF Scientific’s Role in Modern Mining Economics

Fair Value AU$2.10|2.4% undervalued

RO

Community Contributor