Advertisement

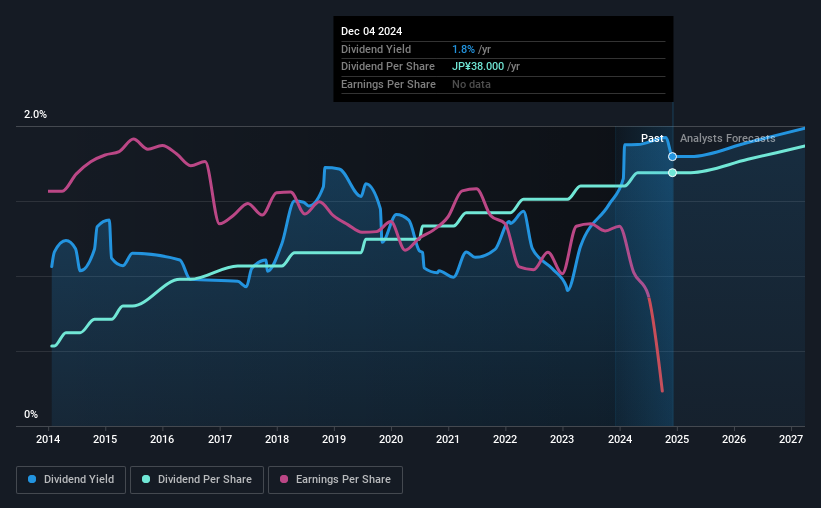

Fujitsu General Limited's (TSE:6755) investors are due to receive a payment of ¥19.00 per share on 19th of June. Based on this payment, the dividend yield for the company will be 1.8%, which is fairly typical for the industry.

View our latest analysis for Fujitsu General

Fujitsu General Might Find It Hard To Continue The Dividend

Unless the payments are sustainable, the dividend yield doesn't mean too much. Even though Fujitsu General isn't generating a profit, it is generating healthy free cash flows that easily cover the dividend. In general, cash flows are more important than the more traditional measures of profit so we feel pretty comfortable with the dividend at this level.

Analysts are expecting EPS to grow by 56.2% over the next 12 months. It's encouraging to see things moving in the right direction, but this probably won't be enough for the company to turn a profit. However, the positive cash flow ratio gives us some comfort about the sustainability of the dividend.

Fujitsu General Has A Solid Track Record

The company has been paying a dividend for a long time, and it has been quite stable which gives us confidence in the future dividend potential. The dividend has gone from an annual total of ¥12.00 in 2014 to the most recent total annual payment of ¥38.00. This works out to be a compound annual growth rate (CAGR) of approximately 12% a year over that time. Rapidly growing dividends for a long time is a very valuable feature for an income stock.

The Dividend Has Limited Growth Potential

Investors could be attracted to the stock based on the quality of its payment history. Let's not jump to conclusions as things might not be as good as they appear on the surface. Fujitsu General's EPS has fallen by approximately 24% per year during the past five years. A sharp decline in earnings per share is not great from from a dividend perspective. Even conservative payout ratios can come under pressure if earnings fall far enough. However, the next year is actually looking up, with earnings set to rise. We would just wait until it becomes a pattern before getting too excited.

In Summary

Overall, this is probably not a great income stock, even though the dividend is being raised at the moment. The company has been bring in plenty of cash to cover the dividend, but we don't necessarily think that makes it a great dividend stock. This company is not in the top tier of income providing stocks.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. However, there are other things to consider for investors when analysing stock performance. Given that earnings are not growing, the dividend does not look nearly so attractive. See if the 6 analysts are forecasting a turnaround in our free collection of analyst estimates here. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:6755

Fujitsu General

Develops, manufactures, sells, and service of air conditioner and telecommunications products and components.

Excellent balance sheet with moderate growth potential.

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|35.7% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|20.5% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|25.2% overvalued

DA

Community Contributor