Advertisement

- Japan

- /

- Commercial Services

- /

- TSE:7976

Hanil Cement And 2 Other Undiscovered Gems With Solid Potential

Simply Wall St

Reviewed by Simply Wall St

In the midst of global market fluctuations, with U.S. stocks ending lower due to tariff uncertainties and a cooling labor market, investors are keenly observing small-cap indices like the S&P 600 for potential opportunities. As markets navigate these challenges, discovering stocks with solid fundamentals and growth potential becomes crucial; Hanil Cement and two other lesser-known companies stand out as promising candidates in this environment.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Darya-Varia Laboratoria | NA | 1.44% | -11.65% | ★★★★★★ |

| Quemchi | 0.66% | 82.67% | 21.69% | ★★★★★★ |

| Wilson Bank Holding | NA | 7.87% | 8.22% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Aesler Grup Internasional | NA | -17.61% | -40.21% | ★★★★★★ |

| National General Insurance (P.J.S.C.) | NA | 11.69% | 30.36% | ★★★★★☆ |

| Watt's | 70.56% | 7.69% | -0.53% | ★★★★★☆ |

| Hollyland (China) Electronics Technology | 3.46% | 13.95% | 11.27% | ★★★★★☆ |

| Al-Deera Holding Company K.P.S.C | 6.11% | 51.44% | 59.77% | ★★★★☆☆ |

| Central Cooperative Bank AD | 4.88% | 37.94% | 537.05% | ★★★★☆☆ |

Underneath we present a selection of stocks filtered out by our screen.

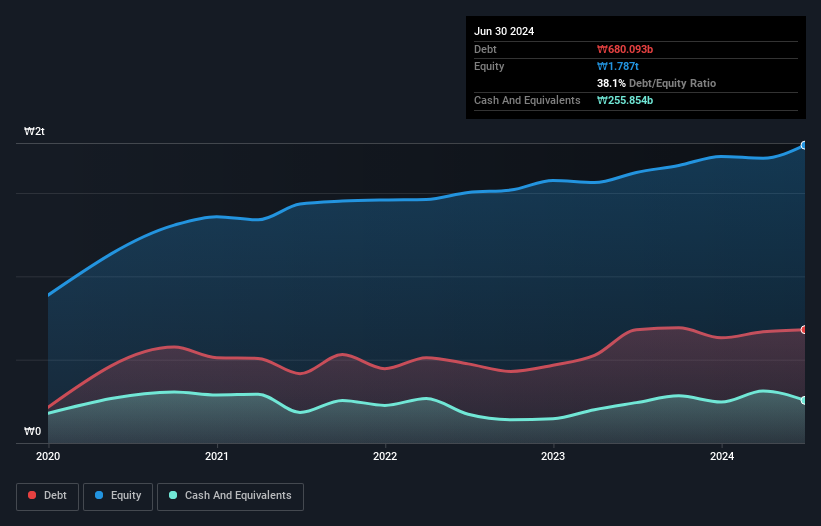

Hanil Cement (KOSE:A300720)

Simply Wall St Value Rating: ★★★★★☆

Overview: Hanil Cement Co., Ltd. is engaged in the production and sale of cement, ready-mixed concrete, and admixtures, with a market capitalization of ₩1.09 trillion.

Operations: The primary revenue streams for Hanil Cement come from its Cement Sector, generating ₩917.97 billion, and the Remital Sector, contributing ₩468.26 billion. The Ready-Mixed Concrete Sector also adds significantly with ₩277.42 billion in revenue.

With an impressive earnings growth of 46.8% over the past year, Hanil Cement has outpaced the Basic Materials industry's 9%, showcasing its potential in this niche sector. The company seems to be trading at a significant discount, valued at 90.3% below estimated fair value, which may attract keen investors looking for hidden opportunities. Its financial health appears robust with a net debt to equity ratio of 20.3%, deemed satisfactory, and interest payments well-covered by EBIT at 14 times coverage. These elements suggest a stable footing and possible room for further growth in the coming years.

- Click to explore a detailed breakdown of our findings in Hanil Cement's health report.

Understand Hanil Cement's track record by examining our Past report.

Kawada Technologies (TSE:3443)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Kawada Technologies, Inc. operates in Japan's steel, civil engineering, architecture, and IT service sectors with a market cap of ¥48.43 billion.

Operations: Kawada Technologies derives its revenue primarily from the steel structure and civil engineering segments, with ¥65.22 billion and ¥38.23 billion respectively. The architecture segment contributes ¥12.78 billion, while the solution shon adds another ¥7.63 billion to its revenue streams.

Kawada Technologies, a promising player in its sector, showcases impressive financial metrics that might catch the eye of savvy investors. With a net debt to equity ratio at 24.3%, it comfortably sits within satisfactory levels, indicating prudent financial management. The company's earnings surged by 59% over the past year, outperforming the broader construction industry growth of nearly 20%. Trading at a price-to-earnings ratio of 5.6x—considerably lower than Japan's market average of 13.4x—it offers good relative value compared to peers. However, future earnings are projected to dip by an average of 8% annually over the next three years, which may be worth monitoring closely for potential impacts on its valuation and growth trajectory.

- Click here and access our complete health analysis report to understand the dynamics of Kawada Technologies.

Examine Kawada Technologies' past performance report to understand how it has performed in the past.

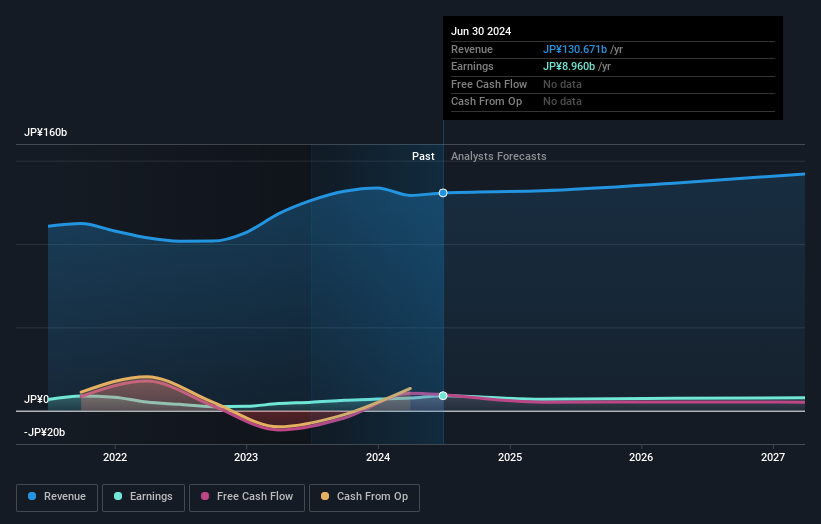

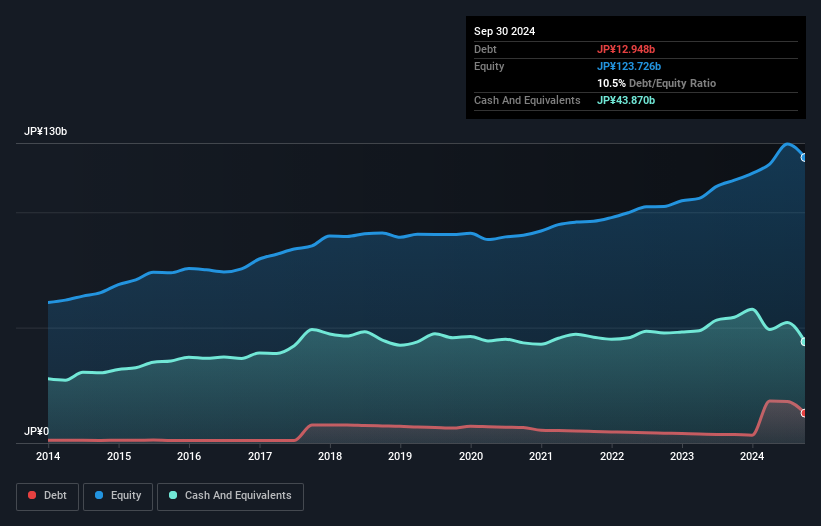

Mitsubishi Pencil (TSE:7976)

Simply Wall St Value Rating: ★★★★★☆

Overview: Mitsubishi Pencil Co., Ltd. is a Japanese company that manufactures and supplies writing instruments, with a market capitalization of ¥123.64 billion.

Operations: The company generates revenue primarily from the sale of writing instruments in Japan. It has a market capitalization of ¥123.64 billion, reflecting its established presence in the industry.

Renowned for its innovative stationery products, Mitsubishi Pencil is a small cap player showing promising financial metrics. The company recently reported a significant earnings growth of 44%, outpacing the industry average of 8%. With cash holdings surpassing total debt, its fiscal health appears robust. A notable ¥5.3 billion one-off gain has influenced recent results, yet the firm continues to trade at an attractive 52% below estimated fair value. Mitsubishi Pencil's strategic share repurchase program aims to enhance capital efficiency, with plans to buy back up to 1 million shares by July 2025.

- Unlock comprehensive insights into our analysis of Mitsubishi Pencil stock in this health report.

Assess Mitsubishi Pencil's past performance with our detailed historical performance reports.

Seize The Opportunity

- Unlock our comprehensive list of 4699 Undiscovered Gems With Strong Fundamentals by clicking here.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:7976

Mitsubishi Pencil

Manufactures and supplies writing instruments in Japan.

Excellent balance sheet, good value and pays a dividend.

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|27.1% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|4.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor