3 Stocks Estimated To Be Up To 45.3% Below Intrinsic Value Offering Potential Opportunities

Reviewed by Simply Wall St

As global markets navigate a complex landscape of inflation concerns and political uncertainties, recent data has shown mixed performances across major indices, with U.S. equities experiencing declines amid resilient labor market reports and hawkish Federal Reserve signals. In this context, identifying stocks that are potentially undervalued can offer intriguing opportunities for investors seeking to capitalize on discrepancies between market prices and intrinsic values.

Top 10 Undervalued Stocks Based On Cash Flows

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Ningbo Sanxing Medical ElectricLtd (SHSE:601567) | CN¥27.91 | CN¥55.63 | 49.8% |

| Alltop Technology (TPEX:3526) | NT$265.50 | NT$529.34 | 49.8% |

| Türkiye Sise Ve Cam Fabrikalari (IBSE:SISE) | TRY39.24 | TRY78.32 | 49.9% |

| FINDEX (TSE:3649) | ¥920.00 | ¥1836.04 | 49.9% |

| Solum (KOSE:A248070) | ₩18740.00 | ₩37472.86 | 50% |

| Pluk Phak Praw Rak Mae (SET:OKJ) | THB15.50 | THB30.86 | 49.8% |

| Mobvista (SEHK:1860) | HK$8.05 | HK$16.09 | 50% |

| Zhende Medical (SHSE:603301) | CN¥20.94 | CN¥41.80 | 49.9% |

| Shinko Electric Industries (TSE:6967) | ¥5870.00 | ¥11691.00 | 49.8% |

| Mobileye Global (NasdaqGS:MBLY) | US$16.51 | US$32.92 | 49.9% |

Let's explore several standout options from the results in the screener.

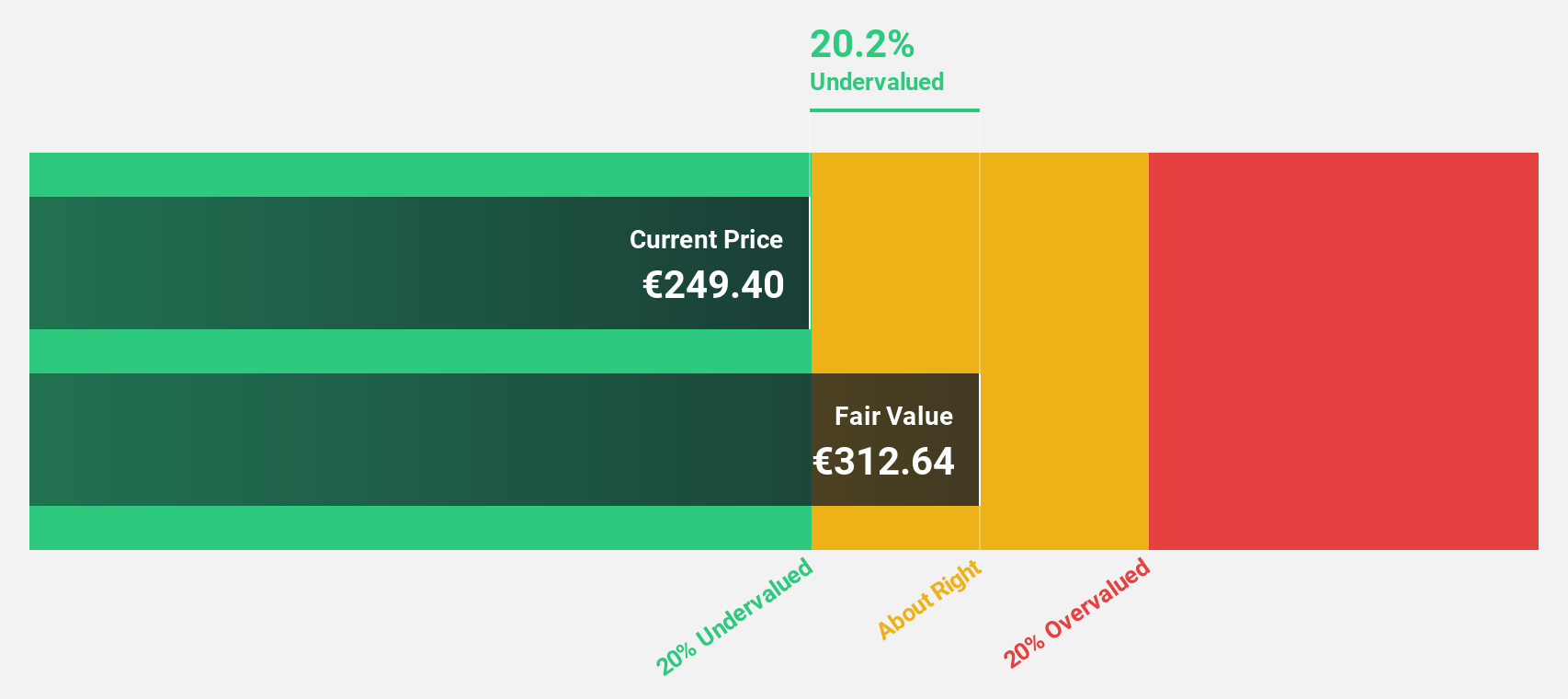

Thales (ENXTPA:HO)

Overview: Thales S.A. offers solutions across the defence and security, aerospace and space, digital identity and security, and transport sectors globally, with a market cap of €30.22 billion.

Operations: The company's revenue is derived from its Aerospace segment at €5.49 billion, Digital Identity & Security at €3.69 billion, and Defence & Security (excluding Digital I&S) at €10.56 billion.

Estimated Discount To Fair Value: 45.3%

Thales is trading significantly below its estimated fair value, with a share price of €147.15 compared to a fair value estimate of €268.91, suggesting it may be undervalued based on cash flows. Despite high debt levels and an unstable dividend history, Thales's earnings are forecast to grow at 16.7% annually, outpacing the French market's growth rate. Recent initiatives like the launch of innovative digital solutions and strategic partnerships enhance its long-term revenue prospects amidst modest expected revenue growth.

- Our earnings growth report unveils the potential for significant increases in Thales' future results.

- Click here and access our complete balance sheet health report to understand the dynamics of Thales.

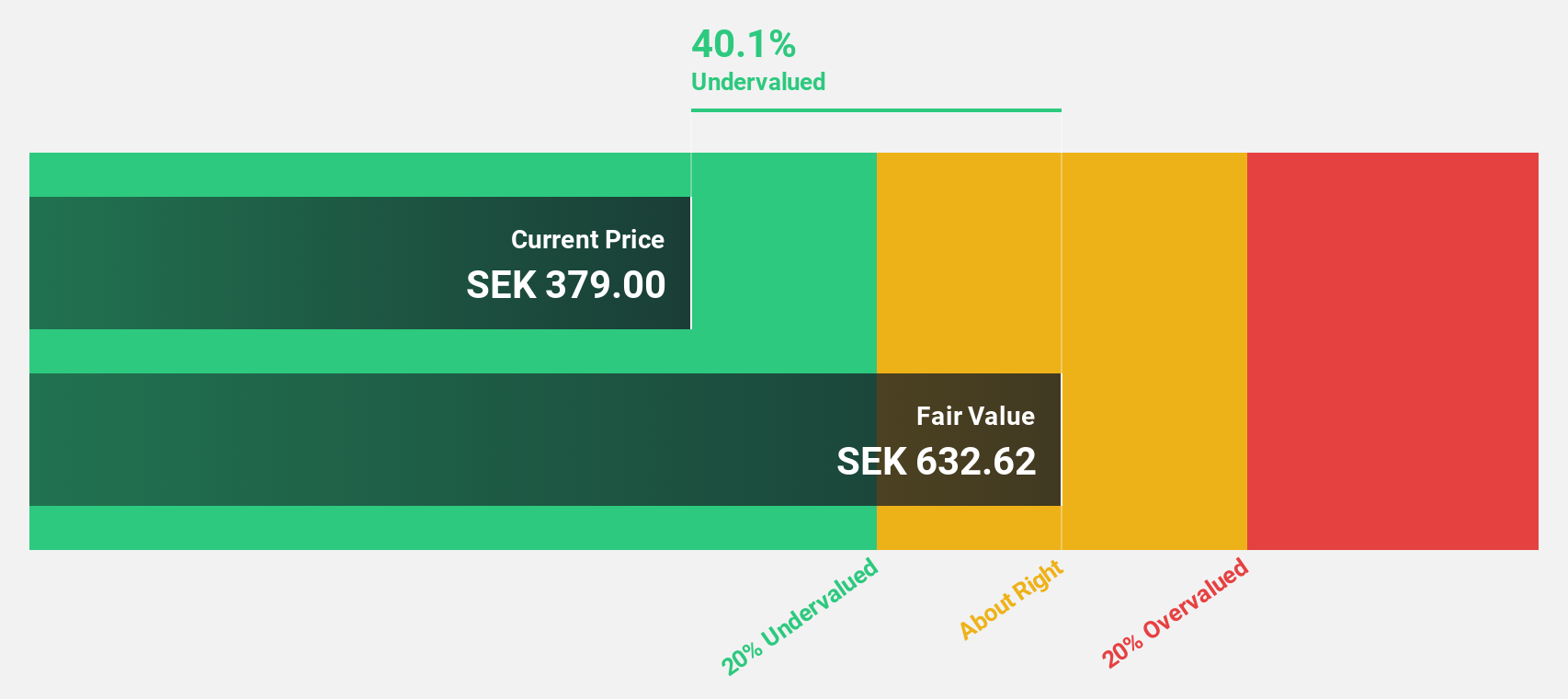

TF Bank (OM:TFBANK)

Overview: TF Bank AB (publ) is a digital bank that offers consumer banking services and e-commerce solutions via its proprietary IT platform, with a market cap of SEK8.99 billion.

Operations: TF Bank's revenue segments include SEK563.14 million from Credit Cards, SEK602.16 million from Consumer Lending, and SEK380.14 million from Ecommerce Solutions (excluding Credit Cards).

Estimated Discount To Fair Value: 36.4%

TF Bank's current share price of SEK418 is significantly below its fair value estimate of SEK657.31, highlighting potential undervaluation based on cash flows. The bank's earnings and revenue are forecast to grow substantially at 26.2% and 30% annually, respectively, outpacing the Swedish market. However, it faces challenges with a high bad loans ratio of 11.4% and a low allowance for these loans at 61%, which could impact financial stability despite strong growth prospects.

- Upon reviewing our latest growth report, TF Bank's projected financial performance appears quite optimistic.

- Get an in-depth perspective on TF Bank's balance sheet by reading our health report here.

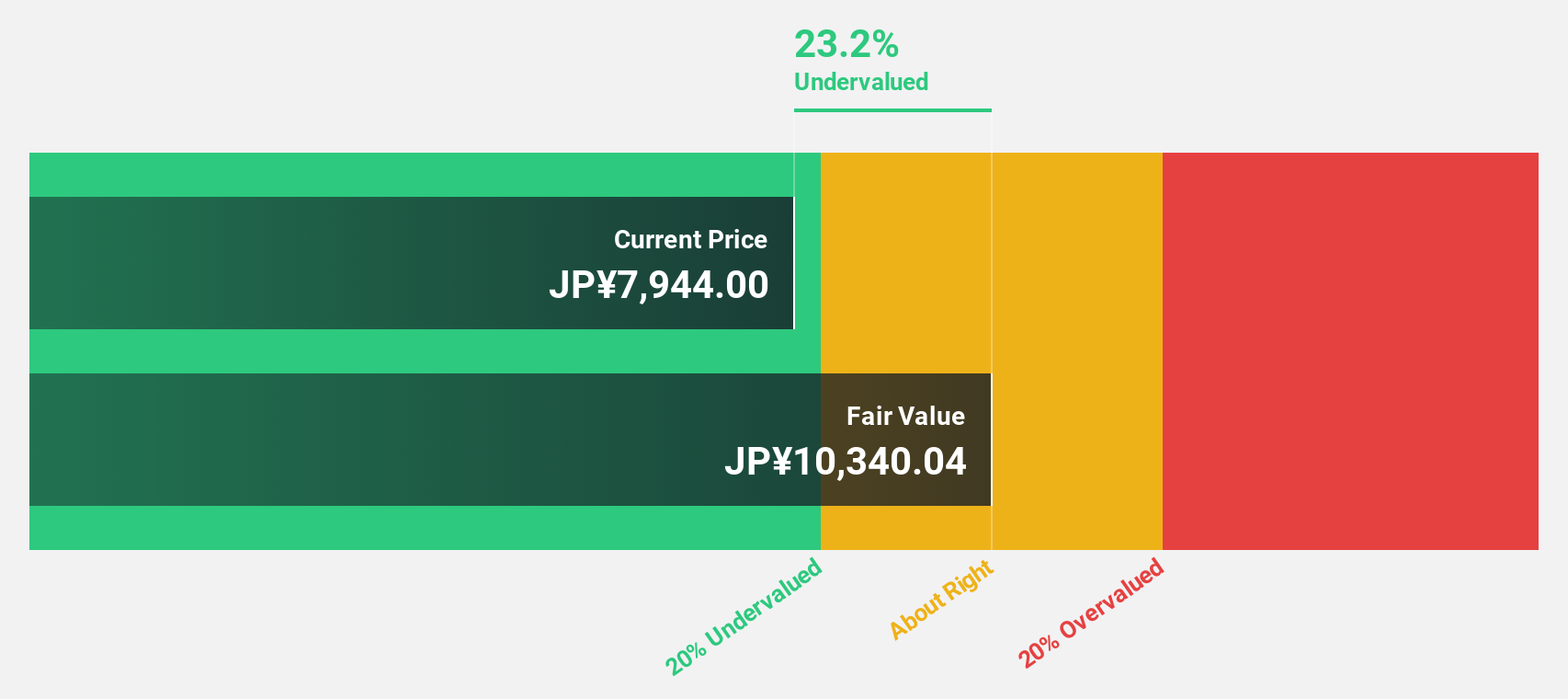

BayCurrent Consulting (TSE:6532)

Overview: BayCurrent Consulting, Inc. offers consulting services in Japan and has a market cap of ¥864.30 billion.

Operations: Revenue segments for the company include consulting services in Japan.

Estimated Discount To Fair Value: 39.1%

BayCurrent Consulting's share price of ¥5900 is considerably below its fair value estimate of ¥9691.88, suggesting undervaluation based on cash flows. The company's earnings and revenue are projected to grow at 17.95% and 17.9% annually, respectively, outpacing the Japanese market averages. Despite high volatility in recent months, BayCurrent's strong return on equity forecast of 35% in three years supports its potential as an attractive investment opportunity amidst these fluctuations.

- Our comprehensive growth report raises the possibility that BayCurrent Consulting is poised for substantial financial growth.

- Take a closer look at BayCurrent Consulting's balance sheet health here in our report.

Make It Happen

- Discover the full array of 867 Undervalued Stocks Based On Cash Flows right here.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if TF Bank might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OM:TFBANK

TF Bank

A digital bank, provides consumer banking services and e-commerce solutions through a proprietary IT platform in Sweden .

Outstanding track record with flawless balance sheet.

Similar Companies

Market Insights

Community Narratives