Advertisement

- Japan

- /

- Professional Services

- /

- TSE:6171

C.E.Management Integrated LaboratoryLtd (TSE:6171) Is Due To Pay A Dividend Of ¥6.00

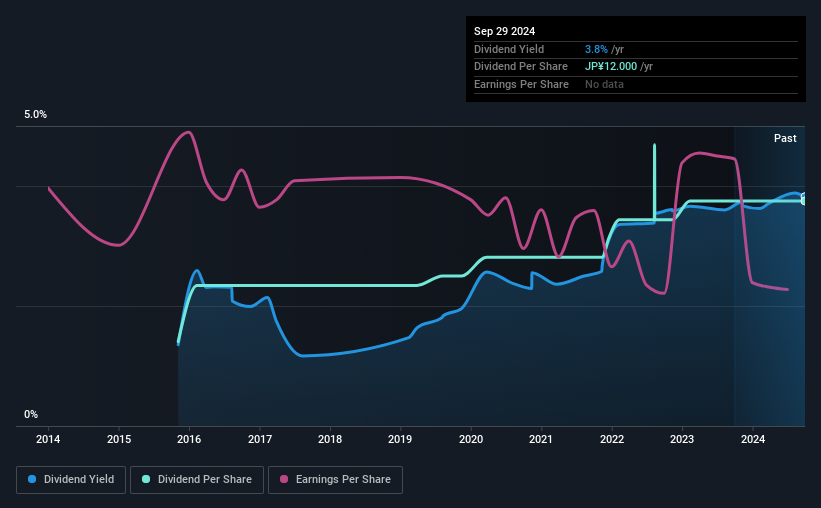

The board of C.E.Management Integrated Laboratory Co.Ltd (TSE:6171) has announced that it will pay a dividend of ¥6.00 per share on the 25th of March. This means the annual payment is 3.8% of the current stock price, which is above the average for the industry.

Check out our latest analysis for C.E.Management Integrated LaboratoryLtd

C.E.Management Integrated LaboratoryLtd's Projections Indicate Future Payments May Be Unsustainable

We like to see robust dividend yields, but that doesn't matter if the payment isn't sustainable. Before this announcement, C.E.Management Integrated LaboratoryLtd was paying out 94% of earnings, but a comparatively small 25% of free cash flows. In general, cash flows are more important than earnings, so we are comfortable that the dividend will be sustainable going forward, especially with so much cash left over for reinvestment.

If the company can't turn things around, EPS could fall by 9.6% over the next year. If the dividend continues along the path it has been on recently, the payout ratio in 12 months could be 113%, which is definitely a bit high to be sustainable going forward.

C.E.Management Integrated LaboratoryLtd Doesn't Have A Long Payment History

Even though the company has been paying a consistent dividend for a while, we would like to see a few more years before we feel comfortable relying on it. The dividend has gone from an annual total of ¥4.50 in 2015 to the most recent total annual payment of ¥12.00. This works out to be a compound annual growth rate (CAGR) of approximately 12% a year over that time. C.E.Management Integrated LaboratoryLtd has been growing its dividend quite rapidly, which is exciting. However, the short payment history makes us question whether this performance will persist across a full market cycle.

Dividend Growth May Be Hard To Come By

Investors could be attracted to the stock based on the quality of its payment history. However, things aren't all that rosy. It's not great to see that C.E.Management Integrated LaboratoryLtd's earnings per share has fallen at approximately 9.6% per year over the past five years. If earnings continue declining, the company may have to make the difficult choice of reducing the dividend or even stopping it completely - the opposite of dividend growth.

Our Thoughts On C.E.Management Integrated LaboratoryLtd's Dividend

In summary, while it's good to see that the dividend hasn't been cut, we are a bit cautious about C.E.Management Integrated LaboratoryLtd's payments, as there could be some issues with sustaining them into the future. The payments haven't been particularly stable and we don't see huge growth potential, but with the dividend well covered by cash flows it could prove to be reliable over the short term. We don't think C.E.Management Integrated LaboratoryLtd is a great stock to add to your portfolio if income is your focus.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. To that end, C.E.Management Integrated LaboratoryLtd has 5 warning signs (and 1 which is a bit concerning) we think you should know about. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:6171

C.E.Management Integrated LaboratoryLtd

Provides services in the areas of civil engineering and construction in Japan.

Excellent balance sheet established dividend payer.

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|44.5% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|46.1% undervalued

TO

Community Contributor