- Japan

- /

- Professional Services

- /

- TSE:3900

What CrowdWorks Inc.'s (TSE:3900) 29% Share Price Gain Is Not Telling You

CrowdWorks Inc. (TSE:3900) shareholders have had their patience rewarded with a 29% share price jump in the last month. The bad news is that even after the stocks recovery in the last 30 days, shareholders are still underwater by about 2.6% over the last year.

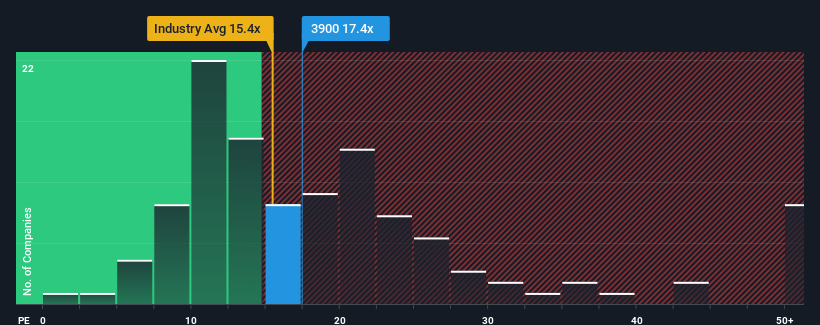

Since its price has surged higher, given around half the companies in Japan have price-to-earnings ratios (or "P/E's") below 13x, you may consider CrowdWorks as a stock to potentially avoid with its 17.4x P/E ratio. However, the P/E might be high for a reason and it requires further investigation to determine if it's justified.

CrowdWorks certainly has been doing a good job lately as it's been growing earnings more than most other companies. It seems that many are expecting the strong earnings performance to persist, which has raised the P/E. If not, then existing shareholders might be a little nervous about the viability of the share price.

See our latest analysis for CrowdWorks

Does Growth Match The High P/E?

CrowdWorks' P/E ratio would be typical for a company that's expected to deliver solid growth, and importantly, perform better than the market.

Retrospectively, the last year delivered an exceptional 49% gain to the company's bottom line. Pleasingly, EPS has also lifted 132% in aggregate from three years ago, thanks to the last 12 months of growth. Therefore, it's fair to say the earnings growth recently has been superb for the company.

Looking ahead now, EPS is anticipated to climb by 7.2% per year during the coming three years according to the dual analysts following the company. That's shaping up to be materially lower than the 9.3% per year growth forecast for the broader market.

In light of this, it's alarming that CrowdWorks' P/E sits above the majority of other companies. Apparently many investors in the company are way more bullish than analysts indicate and aren't willing to let go of their stock at any price. There's a good chance these shareholders are setting themselves up for future disappointment if the P/E falls to levels more in line with the growth outlook.

The Bottom Line On CrowdWorks' P/E

CrowdWorks shares have received a push in the right direction, but its P/E is elevated too. While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

We've established that CrowdWorks currently trades on a much higher than expected P/E since its forecast growth is lower than the wider market. When we see a weak earnings outlook with slower than market growth, we suspect the share price is at risk of declining, sending the high P/E lower. Unless these conditions improve markedly, it's very challenging to accept these prices as being reasonable.

Many other vital risk factors can be found on the company's balance sheet. You can assess many of the main risks through our free balance sheet analysis for CrowdWorks with six simple checks.

If you're unsure about the strength of CrowdWorks' business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:3900

Excellent balance sheet with reasonable growth potential.

Market Insights

Community Narratives