Advertisement

- Japan

- /

- Commercial Services

- /

- TSE:1418

We Think Interlife Holdings (TYO:1418) Can Manage Its Debt With Ease

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies Interlife Holdings Co., Ltd. (TYO:1418) makes use of debt. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first step when considering a company's debt levels is to consider its cash and debt together.

Check out our latest analysis for Interlife Holdings

What Is Interlife Holdings's Debt?

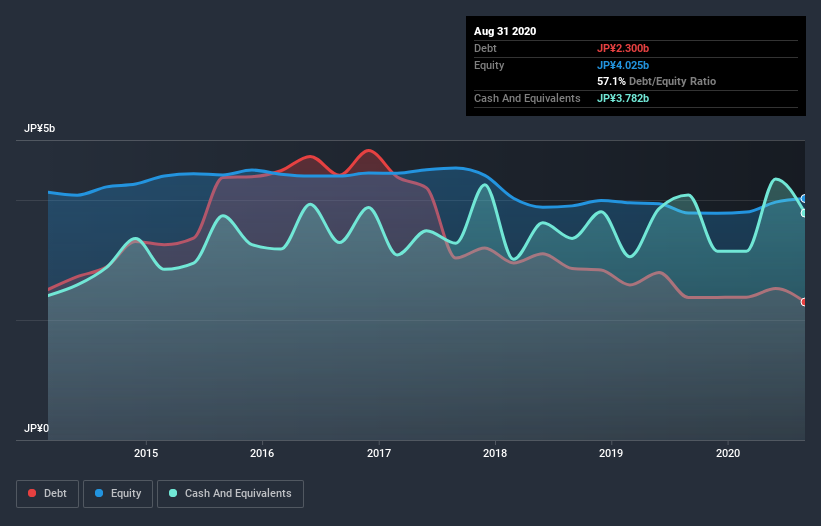

As you can see below, Interlife Holdings had JP¥2.30b of debt, at August 2020, which is about the same as the year before. You can click the chart for greater detail. But it also has JP¥3.78b in cash to offset that, meaning it has JP¥1.48b net cash.

A Look At Interlife Holdings's Liabilities

The latest balance sheet data shows that Interlife Holdings had liabilities of JP¥4.25b due within a year, and liabilities of JP¥1.17b falling due after that. Offsetting this, it had JP¥3.78b in cash and JP¥1.96b in receivables that were due within 12 months. So it actually has JP¥331.0m more liquid assets than total liabilities.

This short term liquidity is a sign that Interlife Holdings could probably pay off its debt with ease, as its balance sheet is far from stretched. Simply put, the fact that Interlife Holdings has more cash than debt is arguably a good indication that it can manage its debt safely.

Even more impressive was the fact that Interlife Holdings grew its EBIT by 249% over twelve months. If maintained that growth will make the debt even more manageable in the years ahead. The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since Interlife Holdings will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. While Interlife Holdings has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. During the last two years, Interlife Holdings produced sturdy free cash flow equating to 77% of its EBIT, about what we'd expect. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Summing up

While it is always sensible to investigate a company's debt, in this case Interlife Holdings has JP¥1.48b in net cash and a decent-looking balance sheet. And it impressed us with its EBIT growth of 249% over the last year. So we don't think Interlife Holdings's use of debt is risky. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. To that end, you should learn about the 5 warning signs we've spotted with Interlife Holdings (including 3 which is don't sit too well with us) .

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

If you decide to trade Interlife Holdings, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About TSE:1418

Interlife Holdings

Provides designs, constructs, manages, and maintains commercial facilities and public facilities in Japan.

Flawless balance sheet 6 star dividend payer.

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|27.1% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|5.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor