Advertisement

- Japan

- /

- Trade Distributors

- /

- TSE:8093

Take Care Before Diving Into The Deep End On Kyokuto Boeki Kaisha, Ltd. (TSE:8093)

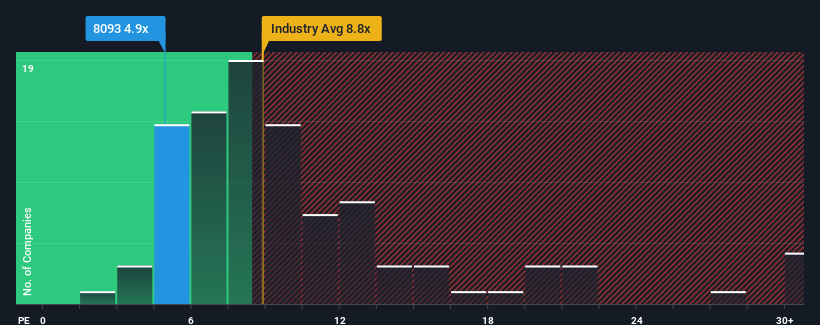

With a price-to-earnings (or "P/E") ratio of 4.9x Kyokuto Boeki Kaisha, Ltd. (TSE:8093) may be sending very bullish signals at the moment, given that almost half of all companies in Japan have P/E ratios greater than 13x and even P/E's higher than 20x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly reduced P/E.

With earnings growth that's exceedingly strong of late, Kyokuto Boeki Kaisha has been doing very well. One possibility is that the P/E is low because investors think this strong earnings growth might actually underperform the broader market in the near future. If that doesn't eventuate, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

Check out our latest analysis for Kyokuto Boeki Kaisha

Does Growth Match The Low P/E?

There's an inherent assumption that a company should far underperform the market for P/E ratios like Kyokuto Boeki Kaisha's to be considered reasonable.

Retrospectively, the last year delivered an exceptional 236% gain to the company's bottom line. The latest three year period has also seen an excellent 384% overall rise in EPS, aided by its short-term performance. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

Weighing that recent medium-term earnings trajectory against the broader market's one-year forecast for expansion of 10% shows it's noticeably more attractive on an annualised basis.

In light of this, it's peculiar that Kyokuto Boeki Kaisha's P/E sits below the majority of other companies. It looks like most investors are not convinced the company can maintain its recent growth rates.

The Bottom Line On Kyokuto Boeki Kaisha's P/E

Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

We've established that Kyokuto Boeki Kaisha currently trades on a much lower than expected P/E since its recent three-year growth is higher than the wider market forecast. There could be some major unobserved threats to earnings preventing the P/E ratio from matching this positive performance. At least price risks look to be very low if recent medium-term earnings trends continue, but investors seem to think future earnings could see a lot of volatility.

Plus, you should also learn about these 2 warning signs we've spotted with Kyokuto Boeki Kaisha .

Of course, you might also be able to find a better stock than Kyokuto Boeki Kaisha. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Valuation is complex, but we're here to simplify it.

Discover if Kyokuto Boeki Kaisha might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:8093

Kyokuto Boeki Kaisha

Primarily operates as an engineering trading company in Japan and internationally.

Proven track record with adequate balance sheet and pays a dividend.

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|12.2% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.1% undervalued

TR

Community Contributor