Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that Sato Shoji Corporation (TSE:8065) does use debt in its business. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we examine debt levels, we first consider both cash and debt levels, together.

View our latest analysis for Sato Shoji

What Is Sato Shoji's Net Debt?

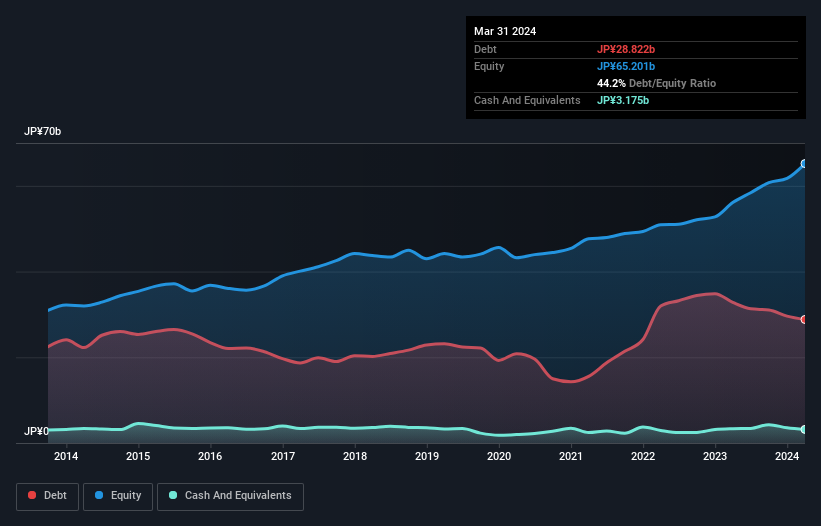

You can click the graphic below for the historical numbers, but it shows that Sato Shoji had JP¥28.8b of debt in March 2024, down from JP¥32.8b, one year before. However, because it has a cash reserve of JP¥3.18b, its net debt is less, at about JP¥25.6b.

A Look At Sato Shoji's Liabilities

The latest balance sheet data shows that Sato Shoji had liabilities of JP¥92.1b due within a year, and liabilities of JP¥15.5b falling due after that. On the other hand, it had cash of JP¥3.18b and JP¥91.2b worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by JP¥13.3b.

While this might seem like a lot, it is not so bad since Sato Shoji has a market capitalization of JP¥31.0b, and so it could probably strengthen its balance sheet by raising capital if it needed to. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Sato Shoji has a debt to EBITDA ratio of 3.4, which signals significant debt, but is still pretty reasonable for most types of business. But its EBIT was about 1k times its interest expense, implying the company isn't really paying a high cost to maintain that level of debt. Even were the low cost to prove unsustainable, that is a good sign. We saw Sato Shoji grow its EBIT by 5.6% in the last twelve months. That's far from incredible but it is a good thing, when it comes to paying off debt. There's no doubt that we learn most about debt from the balance sheet. But it is Sato Shoji's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the last three years, Sato Shoji saw substantial negative free cash flow, in total. While investors are no doubt expecting a reversal of that situation in due course, it clearly does mean its use of debt is more risky.

Our View

Sato Shoji's conversion of EBIT to free cash flow and net debt to EBITDA definitely weigh on it, in our esteem. But its interest cover tells a very different story, and suggests some resilience. Taking the abovementioned factors together we do think Sato Shoji's debt poses some risks to the business. While that debt can boost returns, we think the company has enough leverage now. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. These risks can be hard to spot. Every company has them, and we've spotted 1 warning sign for Sato Shoji you should know about.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:8065

Sato Shoji

Sells iron and steel products, non-ferrous metals, machines, electronic materials, industrial tools, lifestyle goods, precious metals and jewelry, construction materials, and environment-related goods in Japan.

Established dividend payer with mediocre balance sheet.

Market Insights

Community Narratives