Advertisement

- Japan

- /

- Electrical

- /

- TSE:6652

It Might Not Be A Great Idea To Buy IDEC Corporation (TSE:6652) For Its Next Dividend

IDEC Corporation (TSE:6652) is about to trade ex-dividend in the next three days. Typically, the ex-dividend date is two business days before the record date, which is the date on which a company determines the shareholders eligible to receive a dividend. The ex-dividend date is important as the process of settlement involves at least two full business days. So if you miss that date, you would not show up on the company's books on the record date. In other words, investors can purchase IDEC's shares before the 28th of March in order to be eligible for the dividend, which will be paid on the 27th of May.

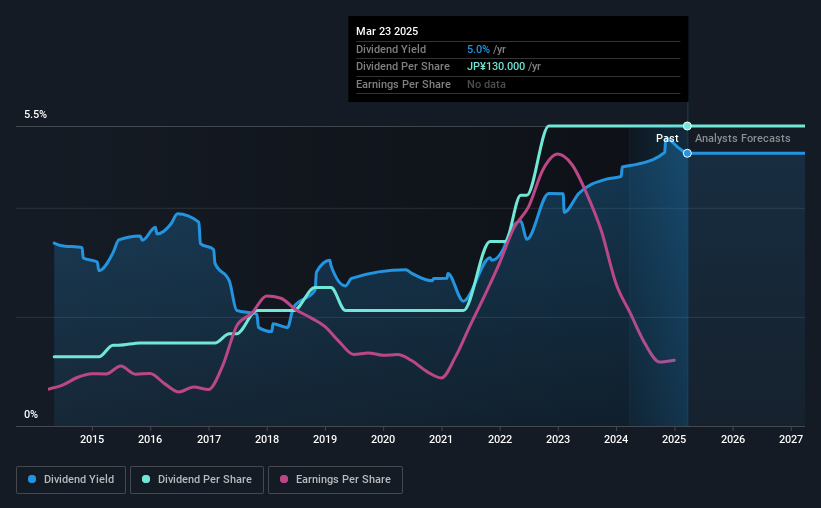

The company's next dividend payment will be JP¥65.00 per share, and in the last 12 months, the company paid a total of JP¥130 per share. Calculating the last year's worth of payments shows that IDEC has a trailing yield of 5.0% on the current share price of JP¥2600.00. We love seeing companies pay a dividend, but it's also important to be sure that laying the golden eggs isn't going to kill our golden goose! So we need to check whether the dividend payments are covered, and if earnings are growing.

Dividends are usually paid out of company profits, so if a company pays out more than it earned then its dividend is usually at greater risk of being cut. IDEC distributed an unsustainably high 148% of its profit as dividends to shareholders last year. Without extenuating circumstances, we'd consider the dividend at risk of a cut. Yet cash flow is typically more important than profit for assessing dividend sustainability, so we should always check if the company generated enough cash to afford its dividend. Dividends consumed 56% of the company's free cash flow last year, which is within a normal range for most dividend-paying organisations.

It's disappointing to see that the dividend was not covered by profits, but cash is more important from a dividend sustainability perspective, and IDEC fortunately did generate enough cash to fund its dividend. Still, if the company repeatedly paid a dividend greater than its profits, we'd be concerned. Extraordinarily few companies are capable of persistently paying a dividend that is greater than their profits.

See our latest analysis for IDEC

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Companies with falling earnings are riskier for dividend shareholders. Investors love dividends, so if earnings fall and the dividend is reduced, expect a stock to be sold off heavily at the same time. That's why it's not ideal to see IDEC's earnings per share have been shrinking at 4.9% a year over the previous five years.

Many investors will assess a company's dividend performance by evaluating how much the dividend payments have changed over time. IDEC has delivered 16% dividend growth per year on average over the past 10 years. The only way to pay higher dividends when earnings are shrinking is either to pay out a larger percentage of profits, spend cash from the balance sheet, or borrow the money. IDEC is already paying out 148% of its profits, and with shrinking earnings we think it's unlikely that this dividend will grow quickly in the future.

The Bottom Line

Has IDEC got what it takes to maintain its dividend payments? It's never fun to see a company's earnings per share in retreat. What's more, IDEC is paying out a majority of its earnings and over half its free cash flow. It's hard to say if the business has the financial resources and time to turn things around without cutting the dividend. Bottom line: IDEC has some unfortunate characteristics that we think could lead to sub-optimal outcomes for dividend investors.

With that in mind though, if the poor dividend characteristics of IDEC don't faze you, it's worth being mindful of the risks involved with this business. To help with this, we've discovered 2 warning signs for IDEC that you should be aware of before investing in their shares.

A common investing mistake is buying the first interesting stock you see. Here you can find a full list of high-yield dividend stocks.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:6652

IDEC

Engages in the development of human machine interfaces, industrial switches, control devices, and daily life scenes in Japan and internationally.

Flawless balance sheet with reasonable growth potential.

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.6% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor