Advertisement

- China

- /

- Hospitality

- /

- SZSE:300144

Top Growth Companies With Insider Confidence October 2024

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate a complex landscape, with notable shifts in interest rates and sector performances, investors are keenly observing the resilience of growth stocks. In this environment, companies with high insider ownership often stand out as they reflect a strong alignment between management and shareholder interests, potentially indicating confidence in the company's future prospects.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Lavvi Empreendimentos Imobiliários (BOVESPA:LAVV3) | 11.9% | 21.1% |

| Clinuvel Pharmaceuticals (ASX:CUV) | 10.4% | 27.4% |

| KebNi (OM:KEBNI B) | 36.3% | 87.2% |

| Findi (ASX:FND) | 35.8% | 64.8% |

| HANA Micron (KOSDAQ:A067310) | 18.3% | 105.8% |

| Pharma Mar (BME:PHM) | 11.8% | 55.1% |

| Adveritas (ASX:AV1) | 21.2% | 144.2% |

| Plenti Group (ASX:PLT) | 12.8% | 107.6% |

| EHang Holdings (NasdaqGM:EH) | 32.8% | 81.4% |

| Credo Technology Group Holding (NasdaqGS:CRDO) | 13.9% | 95% |

Here we highlight a subset of our preferred stocks from the screener.

Jiangsu Lopal Tech (SHSE:603906)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Jiangsu Lopal Tech Co., Ltd. focuses on the R&D, production, and sale of lithium iron phosphate cathode materials and environmental protection fine chemicals for vehicles globally, with a market cap of CN¥6.86 billion.

Operations: Revenue Segments (in millions of CN¥): The company generates revenue through its lithium iron phosphate cathode materials and environmental protection fine chemicals for vehicles, serving both domestic and international markets.

Insider Ownership: 35.8%

Earnings Growth Forecast: 105.4% p.a.

Jiangsu Lopal Tech is trading significantly below its estimated fair value, suggesting potential undervaluation. Despite a high debt level, the company is expected to achieve profitability within three years and boasts a forecasted annual revenue growth of 23%, outpacing the broader Chinese market. However, recent shareholder dilution and low projected return on equity may concern investors. The HKD 700 million follow-on equity offering could impact insider ownership dynamics moving forward.

- Unlock comprehensive insights into our analysis of Jiangsu Lopal Tech stock in this growth report.

- Upon reviewing our latest valuation report, Jiangsu Lopal Tech's share price might be too pessimistic.

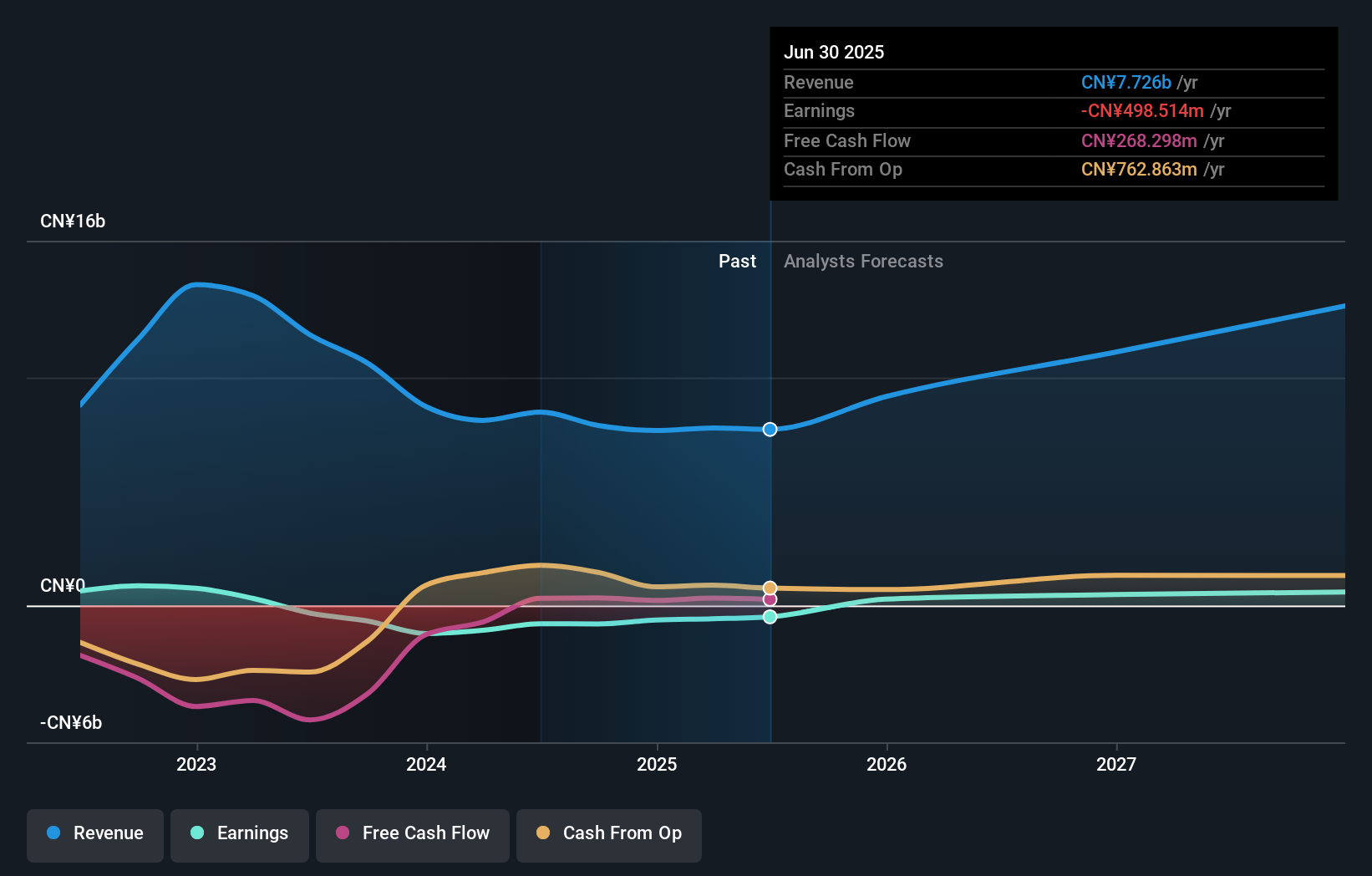

Songcheng Performance DevelopmentLtd (SZSE:300144)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Songcheng Performance Development Co., Ltd operates in the performing arts industry in China with a market cap of CN¥26.49 billion.

Operations: Songcheng Performance Development Co., Ltd generates its revenue from the performing arts sector in China.

Insider Ownership: 14.5%

Earnings Growth Forecast: 54.5% p.a.

Songcheng Performance Development Ltd is trading 27.9% below its estimated fair value, indicating potential undervaluation. The company reported strong financial performance with CNY 2.01 billion in sales for the first nine months of 2024, up from CNY 1.62 billion a year ago, and net income increased to CNY 1.01 billion from CNY 787.11 million last year. Despite volatile share prices and lower profit margins compared to the previous year, earnings are expected to grow significantly at an annual rate of 54.5%.

- Get an in-depth perspective on Songcheng Performance DevelopmentLtd's performance by reading our analyst estimates report here.

- The analysis detailed in our Songcheng Performance DevelopmentLtd valuation report hints at an inflated share price compared to its estimated value.

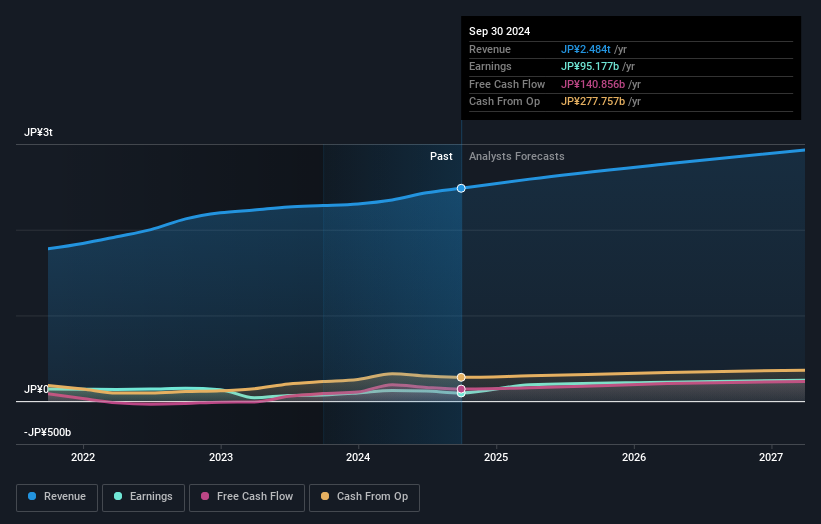

Nidec (TSE:6594)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Nidec Corporation, along with its subsidiaries, is engaged in the development, manufacturing, and sale of motors, electronics and optical components, and other related products both in Japan and internationally; it has a market cap of approximately ¥3.43 trillion.

Operations: Nidec Corporation generates revenue through its development, manufacturing, and sales of motors, electronics, and optical components globally.

Insider Ownership: 12.3%

Earnings Growth Forecast: 22.4% p.a.

Nidec is trading at 21% below its estimated fair value, suggesting potential undervaluation. Earnings are projected to grow significantly at 22.43% annually over the next three years, outpacing the Japanese market's average growth rate of 8.7%. However, revenue growth is expected to be moderate at 6.3%, though still above the market's 4.2%. Despite no recent insider transactions or share buybacks, Nidec's financial outlook remains promising for growth-focused investors.

- Click here to discover the nuances of Nidec with our detailed analytical future growth report.

- Upon reviewing our latest valuation report, Nidec's share price might be too optimistic.

Key Takeaways

- Unlock our comprehensive list of 1495 Fast Growing Companies With High Insider Ownership by clicking here.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:300144

Songcheng Performance DevelopmentLtd

Operates in the performing arts industry primarily in China.

Flawless balance sheet with solid track record and pays a dividend.

Market Insights

Advertisement

Community Narratives

100% Patient Improvement in trial puts this $16M Biotech on the radar

Fair Value US$5.30|69.8% undervalued

JO

Community Contributor

Exxon Mobil's 17.5% Upside Promises Industry-Leading Returns in Energy Transition

Fair Value US$132.00|15.0% undervalued

HE

Community Contributor

NHC Analysis: Quality at a Good Price. A Golden Opportunity?

Fair Value US$179.80|36.1% undervalued

DA

Community Contributor

Product Refresh And Global Expansion Will Empower Future Market Leadership

Fair Value US$202.60|21.1% undervalued

AN

Based on Analyst Price Targets