Advertisement

Take Care Before Jumping Onto NTN Corporation (TSE:6472) Even Though It's 29% Cheaper

The NTN Corporation (TSE:6472) share price has fared very poorly over the last month, falling by a substantial 29%. Instead of being rewarded, shareholders who have already held through the last twelve months are now sitting on a 21% share price drop.

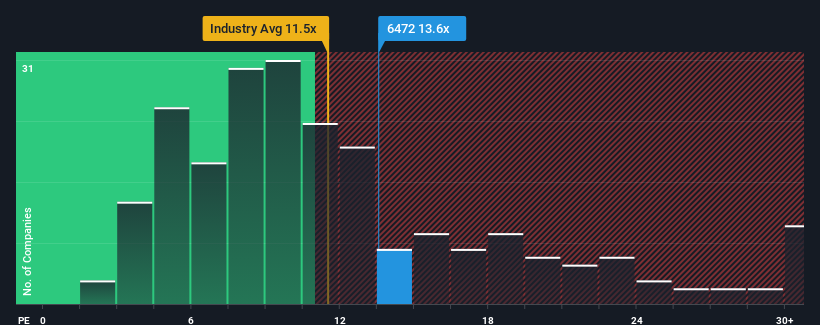

In spite of the heavy fall in price, it's still not a stretch to say that NTN's price-to-earnings (or "P/E") ratio of 13.6x right now seems quite "middle-of-the-road" compared to the market in Japan, where the median P/E ratio is around 13x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/E.

NTN hasn't been tracking well recently as its declining earnings compare poorly to other companies, which have seen some growth on average. It might be that many expect the dour earnings performance to strengthen positively, which has kept the P/E from falling. You'd really hope so, otherwise you're paying a relatively elevated price for a company with this sort of growth profile.

Check out our latest analysis for NTN

Is There Some Growth For NTN?

The only time you'd be comfortable seeing a P/E like NTN's is when the company's growth is tracking the market closely.

Retrospectively, the last year delivered a frustrating 37% decrease to the company's bottom line. However, a few very strong years before that means that it was still able to grow EPS by an impressive 445% in total over the last three years. Accordingly, while they would have preferred to keep the run going, shareholders would probably welcome the medium-term rates of earnings growth.

Shifting to the future, estimates from the six analysts covering the company suggest earnings should grow by 33% per annum over the next three years. That's shaping up to be materially higher than the 9.6% per year growth forecast for the broader market.

With this information, we find it interesting that NTN is trading at a fairly similar P/E to the market. It may be that most investors aren't convinced the company can achieve future growth expectations.

The Final Word

With its share price falling into a hole, the P/E for NTN looks quite average now. It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

We've established that NTN currently trades on a lower than expected P/E since its forecast growth is higher than the wider market. When we see a strong earnings outlook with faster-than-market growth, we assume potential risks are what might be placing pressure on the P/E ratio. At least the risk of a price drop looks to be subdued, but investors seem to think future earnings could see some volatility.

You should always think about risks. Case in point, we've spotted 4 warning signs for NTN you should be aware of, and 1 of them is a bit concerning.

If you're unsure about the strength of NTN's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if NTN might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:6472

NTN

Engages in the manufacture and sale of bearings, drive shafts, and precision equipment and other products in Japan and internationally.

Undervalued with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|42.8% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|66.0% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|40.8% undervalued

UN

Community Contributor