Sinko Industries' (TSE:6458) Shareholders Will Receive A Bigger Dividend Than Last Year

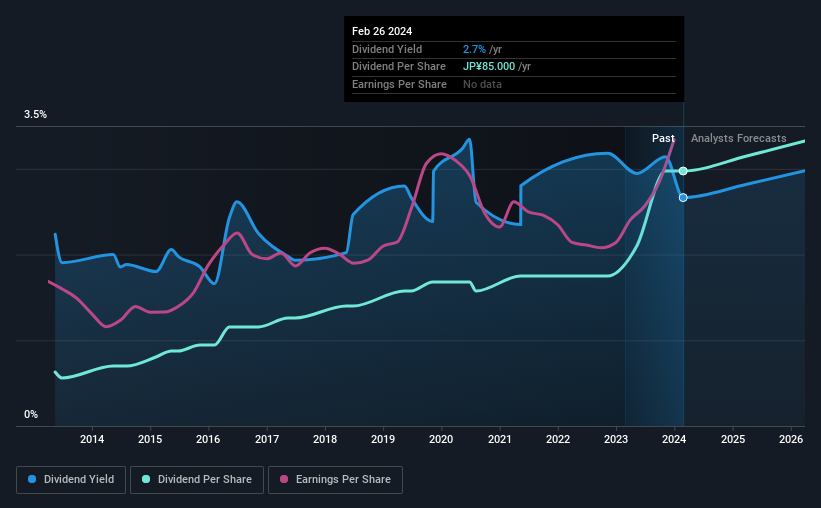

Sinko Industries Ltd.'s (TSE:6458) dividend will be increasing from last year's payment of the same period to ¥50.00 on 26th of June. This takes the dividend yield to 2.7%, which shareholders will be pleased with.

While the dividend yield is important for income investors, it is also important to consider any large share price moves, as this will generally outweigh any gains from distributions. Investors will be pleased to see that Sinko Industries' stock price has increased by 32% in the last 3 months, which is good for shareholders and can also explain a decrease in the dividend yield.

Check out our latest analysis for Sinko Industries

Sinko Industries' Earnings Easily Cover The Distributions

We like to see robust dividend yields, but that doesn't matter if the payment isn't sustainable. However, Sinko Industries' earnings easily cover the dividend. This means that most of what the business earns is being used to help it grow.

Over the next year, EPS is forecast to expand by 8.6%. If the dividend continues on this path, the payout ratio could be 35% by next year, which we think can be pretty sustainable going forward.

Sinko Industries Has A Solid Track Record

The company has been paying a dividend for a long time, and it has been quite stable which gives us confidence in the future dividend potential. Since 2014, the annual payment back then was ¥18.00, compared to the most recent full-year payment of ¥85.00. This implies that the company grew its distributions at a yearly rate of about 17% over that duration. We can see that payments have shown some very nice upward momentum without faltering, which provides some reassurance that future payments will also be reliable.

The Dividend Has Growth Potential

The company's investors will be pleased to have been receiving dividend income for some time. It's encouraging to see that Sinko Industries has been growing its earnings per share at 9.9% a year over the past five years. A low payout ratio and decent growth suggests that the company is reinvesting well, and it also has plenty of room to increase the dividend over time.

Sinko Industries Looks Like A Great Dividend Stock

In summary, it is always positive to see the dividend being increased, and we are particularly pleased with its overall sustainability. Earnings are easily covering distributions, and the company is generating plenty of cash. Taking this all into consideration, this looks like it could be a good dividend opportunity.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. However, there are other things to consider for investors when analysing stock performance. You can also discover whether shareholders are aligned with insider interests by checking our visualisation of insider shareholdings and trades in Sinko Industries stock. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

If you're looking to trade Sinko Industries, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:6458

Sinko Industries

Manufactures, sells, and installs air conditioning equipment in Japan and internationally.

Flawless balance sheet with solid track record and pays a dividend.