Optimistic Investors Push Ebara Corporation (TSE:6361) Shares Up 27% But Growth Is Lacking

Despite an already strong run, Ebara Corporation (TSE:6361) shares have been powering on, with a gain of 27% in the last thirty days. The last month tops off a massive increase of 102% in the last year.

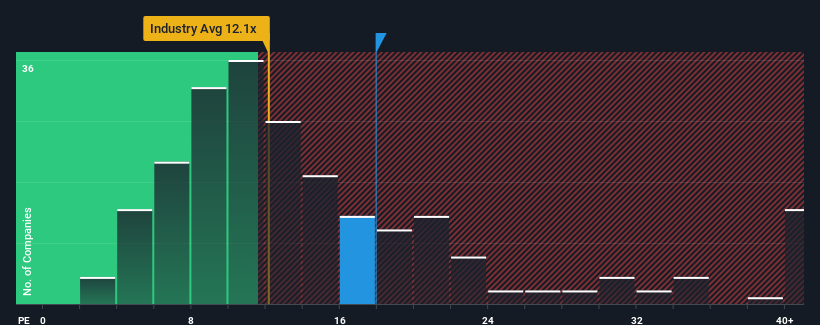

Since its price has surged higher, given around half the companies in Japan have price-to-earnings ratios (or "P/E's") below 14x, you may consider Ebara as a stock to potentially avoid with its 17.9x P/E ratio. However, the P/E might be high for a reason and it requires further investigation to determine if it's justified.

With earnings growth that's superior to most other companies of late, Ebara has been doing relatively well. The P/E is probably high because investors think this strong earnings performance will continue. If not, then existing shareholders might be a little nervous about the viability of the share price.

See our latest analysis for Ebara

How Is Ebara's Growth Trending?

There's an inherent assumption that a company should outperform the market for P/E ratios like Ebara's to be considered reasonable.

Retrospectively, the last year delivered an exceptional 19% gain to the company's bottom line. The strong recent performance means it was also able to grow EPS by 154% in total over the last three years. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

Looking ahead now, EPS is anticipated to climb by 8.7% per year during the coming three years according to the seven analysts following the company. That's shaping up to be similar to the 9.9% per annum growth forecast for the broader market.

With this information, we find it interesting that Ebara is trading at a high P/E compared to the market. It seems most investors are ignoring the fairly average growth expectations and are willing to pay up for exposure to the stock. Although, additional gains will be difficult to achieve as this level of earnings growth is likely to weigh down the share price eventually.

The Final Word

Ebara's P/E is getting right up there since its shares have risen strongly. Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

Our examination of Ebara's analyst forecasts revealed that its market-matching earnings outlook isn't impacting its high P/E as much as we would have predicted. Right now we are uncomfortable with the relatively high share price as the predicted future earnings aren't likely to support such positive sentiment for long. Unless these conditions improve, it's challenging to accept these prices as being reasonable.

Having said that, be aware Ebara is showing 2 warning signs in our investment analysis, you should know about.

Of course, you might also be able to find a better stock than Ebara. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Valuation is complex, but we're here to simplify it.

Discover if Ebara might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:6361

Flawless balance sheet with proven track record.

Similar Companies

Market Insights

Community Narratives