Advertisement

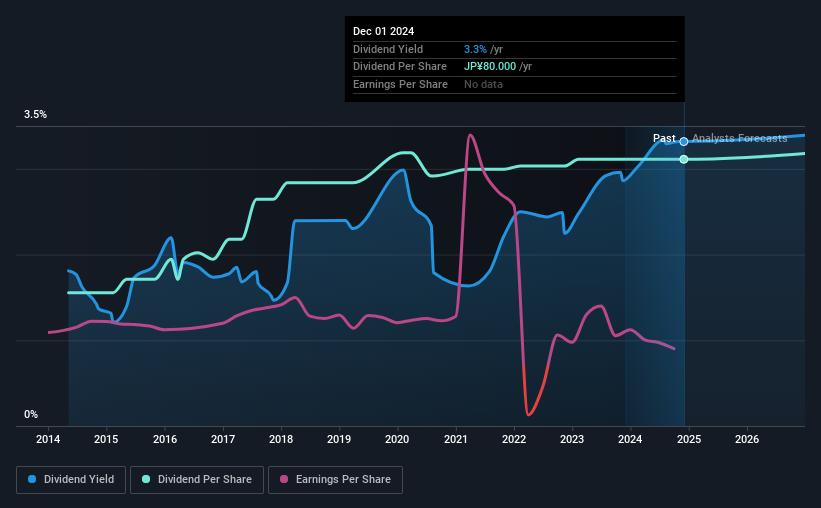

Nabtesco Corporation (TSE:6268) has announced that it will pay a dividend of ¥40.00 per share on the 27th of March. Based on this payment, the dividend yield on the company's stock will be 3.3%, which is an attractive boost to shareholder returns.

View our latest analysis for Nabtesco

Estimates Indicate Nabtesco's Could Struggle to Maintain Dividend Payments In The Future

Impressive dividend yields are good, but this doesn't matter much if the payments can't be sustained. Based on the last payment, earnings were actually smaller than the dividend, and the company was actually spending more cash than it was making. Paying out such a large dividend compared to earnings while also not generating free cash flows is a major warning sign for the sustainability of the dividend as these levels are certainly a bit high.

The next 12 months is set to see EPS grow by 23.6%. However, if the dividend continues along recent trends, it could start putting pressure on the balance sheet with the payout ratio reaching 119% over the next year.

Dividend Volatility

Although the company has a long dividend history, it has been cut at least once in the last 10 years. The annual payment during the last 10 years was ¥40.00 in 2014, and the most recent fiscal year payment was ¥80.00. This means that it has been growing its distributions at 7.2% per annum over that time. A reasonable rate of dividend growth is good to see, but we're wary that the dividend history is not as solid as we'd like, having been cut at least once.

The Dividend Has Limited Growth Potential

Given that the dividend has been cut in the past, we need to check if earnings are growing and if that might lead to stronger dividends in the future. Over the past five years, it looks as though Nabtesco's EPS has declined at around 19% a year. Such rapid declines definitely have the potential to constrain dividend payments if the trend continues into the future. However, the next year is actually looking up, with earnings set to rise. We would just wait until it becomes a pattern before getting too excited.

We're Not Big Fans Of Nabtesco's Dividend

Overall, while some might be pleased that the dividend wasn't cut, we think this may help Nabtesco make more consistent payments in the future. The company's earnings aren't high enough to be making such big distributions, and it isn't backed up by strong growth or consistency either. Considering all of these factors, we wouldn't rely on this dividend if we wanted to live on the income.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. However, there are other things to consider for investors when analysing stock performance. To that end, Nabtesco has 3 warning signs (and 1 which is a bit unpleasant) we think you should know about. Is Nabtesco not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if Nabtesco might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:6268

Nabtesco

Manufactures and sells industrial robot parts, construction machinery, railway vehicle brakes and automatic doors, aircraft parts, automobile brakes and drive controls, marine controls, and platform safety products in Japan and internationally.

Flawless balance sheet with proven track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor