Advertisement

Okuma (TSE:6103): Exploring Valuation After Recent Share Price Fluctuations

Simply Wall St

Reviewed by Kshitija Bhandaru

Okuma (TSE:6103) stock has caught some attention lately as investors track its recent price movements and changes over the month. The company’s share price reflects a mix of short-term fluctuations and longer-term trends that are worth watching for value-oriented investors.

See our latest analysis for Okuma.

After a solid stretch of long-term growth, Okuma’s share price has seen some recent ups and downs. While the 1-day share price return of 3.37% hints at a spark of renewed optimism, the 1-year total shareholder return of 14.8% underscores the company’s broad upward momentum, even as short-term trading remains patchy.

If recent swings have you rethinking your next move, this could be a perfect moment to discover fast growing stocks with high insider ownership

With solid fundamentals and an impressive multi-year return, the real question is whether Okuma shares are still undervalued or if markets have already priced in all that future growth. This could present limited upside for new investors.

Price-to-Earnings of 24.9x: Is it justified?

Okuma shares currently trade at a price-to-earnings (P/E) ratio of 24.9x, which puts the stock well above both the industry norm and its peers. At a last close price of ¥3,525, this premium suggests investors have priced in strong future prospects compared to similar companies.

The P/E ratio measures how much investors are willing to pay for a unit of earnings and is a well-watched signal in the machinery sector. A high ratio often means the market expects significant profit growth ahead or sees the company as higher quality than most.

However, Okuma’s P/E of 24.9x is much higher than the JP Machinery industry average of 13x and the peer average of 15.7x. Even compared to an estimated fair price-to-earnings ratio of 20.6x, Okuma’s shares appear richly valued. This may mean the market expects the company’s forecasted earnings rebound to materialize, or it could signal overexuberance in pricing future growth.

Explore the SWS fair ratio for Okuma

Result: Price-to-Earnings of 24.9x (OVERVALUED)

However, slowing revenue growth or unexpected earnings setbacks could quickly shift sentiment and challenge the current optimism around Okuma’s share price.

Find out about the key risks to this Okuma narrative.

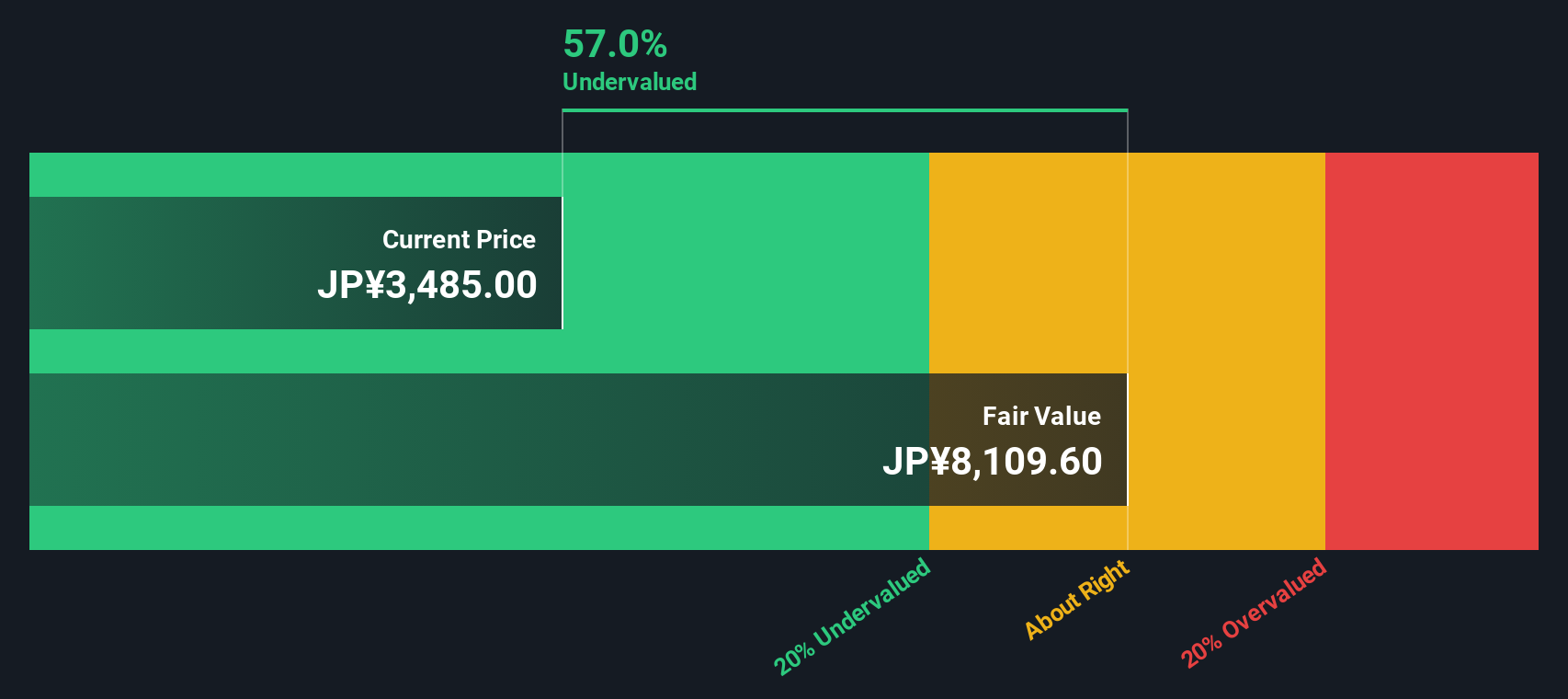

Another View: What About the SWS DCF Model?

While the current price-to-earnings ratio paints Okuma as overvalued compared to both the industry and its peers, our DCF model offers a very different perspective. According to our calculations, Okuma is actually trading at a meaningful discount to its intrinsic value. Could the market be overlooking this potential upside?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Okuma for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Okuma Narrative

If you think a different story is hidden in the numbers or you prefer your own approach, you can easily develop your own narrative in just a few minutes. Do it your way

A great starting point for your Okuma research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Smart Investment Opportunities?

The best investors are always scanning for new ways to put their money to work. Don’t let great options pass by. Try out these distinctive stock screens and see where your next big idea leads.

- Supercharge your portfolio with high yields and steady income by checking out these 18 dividend stocks with yields > 3% now yielding over 3%.

- Capitalize on early-stage innovation and emerging players by tapping into these 3562 penny stocks with strong financials and see which companies could be tomorrow’s standouts.

- Ride the momentum of artificial intelligence breakthroughs. Browse these 25 AI penny stocks to pinpoint the most promising AI opportunities shaping the market today.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:6103

Okuma

Manufactures and sells machine tools in Japan, the United States, Europe, and Asia/Pacific.

Excellent balance sheet with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

Kodiak AI - a potential 100 bagger opportunity?

Fair Value US$14.00|44.7% undervalued

DA

Community Contributor

A Fair Price for a Great Business Facing Real Threats

Fair Value US$383.06|13.0% undervalued

IM

Community Contributor

AXON And Shopify Integration Will Unlock Global Mobile Advertising

Fair Value US$646.30|7.3% undervalued

AN

Based on Analyst Price Targets