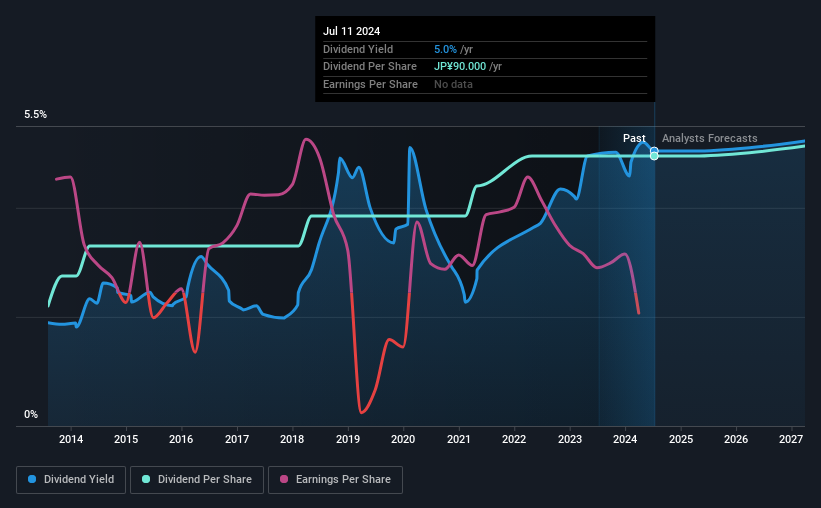

The board of LIXIL Corporation (TSE:5938) has announced that it will pay a dividend of ¥45.00 per share on the 2nd of December. This means the annual payment is 5.0% of the current stock price, which is above the average for the industry.

Check out our latest analysis for LIXIL

LIXIL Might Find It Hard To Continue The Dividend

Impressive dividend yields are good, but this doesn't matter much if the payments can't be sustained. Despite not generating a profit, LIXIL is still paying a dividend. The company is also yet to generate cash flow, so the dividend sustainability is definitely questionable.

Analysts expect the EPS to grow by 44.2% over the next 12 months. While it is good to see income moving in the right direction, it still looks like the company won't achieve profitability. Unfortunately, for the dividend to continue at current levels the company definitely needs to get there sooner rather than later.

LIXIL Has A Solid Track Record

The company has a sustained record of paying dividends with very little fluctuation. The annual payment during the last 10 years was ¥40.00 in 2014, and the most recent fiscal year payment was ¥90.00. This implies that the company grew its distributions at a yearly rate of about 8.4% over that duration. Companies like this can be very valuable over the long term, if the decent rate of growth can be maintained.

The Company Could Face Some Challenges Growing The Dividend

Investors who have held shares in the company for the past few years will be happy with the dividend income they have received. It's encouraging to see that LIXIL has been growing its earnings per share at 34% a year over the past five years. While the company hasn't yet recorded a profit, the growth rates are healthy. If profitability can be achieved soon and growth continues apace, this stock could certainly turn into a solid dividend payer.

LIXIL's Dividend Doesn't Look Sustainable

In summary, while it's good to see that the dividend hasn't been cut, we are a bit cautious about LIXIL's payments, as there could be some issues with sustaining them into the future. In the past the payments have been stable, but we think the company is paying out too much for this to continue for the long term. We would probably look elsewhere for an income investment.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. However, there are other things to consider for investors when analysing stock performance. Taking the debate a bit further, we've identified 2 warning signs for LIXIL that investors need to be conscious of moving forward. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:5938

LIXIL

Through its subsidiaries, operates water technology and housing technology business in Japan and internationally.

Established dividend payer and fair value.

Similar Companies

Market Insights

Community Narratives