- Japan

- /

- Construction

- /

- TSE:1814

Daisue Construction (TSE:1814) Has Announced That It Will Be Increasing Its Dividend To ¥44.50

Daisue Construction Co., Ltd. (TSE:1814) has announced that it will be increasing its dividend from last year's comparable payment on the 2nd of December to ¥44.50. This will take the dividend yield to an attractive 5.4%, providing a nice boost to shareholder returns.

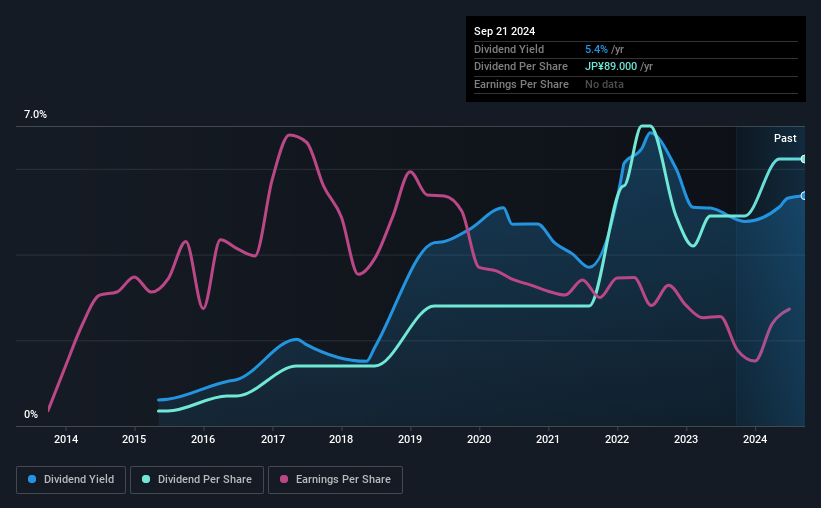

See our latest analysis for Daisue Construction

Daisue Construction's Projected Earnings Seem Likely To Cover Future Distributions

A big dividend yield for a few years doesn't mean much if it can't be sustained. Before making this announcement, Daisue Construction was earning enough to cover the dividend, but it wasn't generating any free cash flows. No cash flows could definitely make returning cash to shareholders difficult, or at least mean the balance sheet will come under pressure.

If the company can't turn things around, EPS could fall by 12.8% over the next year. If recent patterns in the dividend continue, we could see the payout ratio reaching 82% in the next 12 months which is on the higher end of the range we would say is sustainable.

Daisue Construction's Dividend Has Lacked Consistency

Looking back, Daisue Construction's dividend hasn't been particularly consistent. Due to this, we are a little bit cautious about the dividend consistency over a full economic cycle. The annual payment during the last 9 years was ¥5.00 in 2015, and the most recent fiscal year payment was ¥89.00. This implies that the company grew its distributions at a yearly rate of about 38% over that duration. Daisue Construction has grown distributions at a rapid rate despite cutting the dividend at least once in the past. Companies that cut once often cut again, so we would be cautious about buying this stock solely for the dividend income.

Dividend Growth Potential Is Shaky

With a relatively unstable dividend, it's even more important to evaluate if earnings per share is growing, which could point to a growing dividend in the future. Over the past five years, it looks as though Daisue Construction's EPS has declined at around 13% a year. A sharp decline in earnings per share is not great from from a dividend perspective. Even conservative payout ratios can come under pressure if earnings fall far enough.

Daisue Construction's Dividend Doesn't Look Sustainable

Overall, this is probably not a great income stock, even though the dividend is being raised at the moment. With cash flows lacking, it is difficult to see how the company can sustain a dividend payment. This company is not in the top tier of income providing stocks.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. However, there are other things to consider for investors when analysing stock performance. For example, we've identified 2 warning signs for Daisue Construction (1 can't be ignored!) that you should be aware of before investing. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:1814

Proven track record with adequate balance sheet and pays a dividend.