Advertisement

- Japan

- /

- Construction

- /

- TSE:1807

These 4 Measures Indicate That Watanabe Sato (TYO:1807) Is Using Debt Safely

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We can see that Watanabe Sato Co., Ltd. (TYO:1807) does use debt in its business. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

See our latest analysis for Watanabe Sato

How Much Debt Does Watanabe Sato Carry?

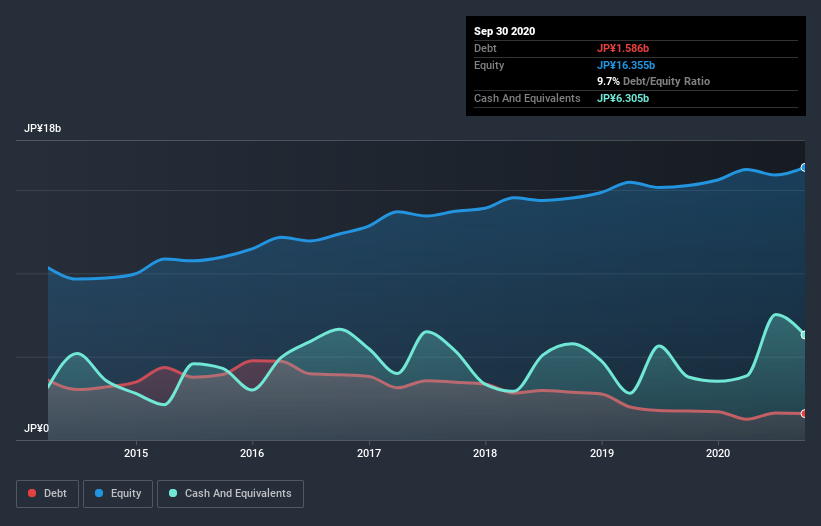

As you can see below, Watanabe Sato had JP¥1.59b of debt at September 2020, down from JP¥1.74b a year prior. But on the other hand it also has JP¥6.31b in cash, leading to a JP¥4.72b net cash position.

How Healthy Is Watanabe Sato's Balance Sheet?

We can see from the most recent balance sheet that Watanabe Sato had liabilities of JP¥10.6b falling due within a year, and liabilities of JP¥3.62b due beyond that. Offsetting this, it had JP¥6.31b in cash and JP¥9.06b in receivables that were due within 12 months. So it actually has JP¥1.17b more liquid assets than total liabilities.

This surplus suggests that Watanabe Sato is using debt in a way that is appears to be both safe and conservative. Due to its strong net asset position, it is not likely to face issues with its lenders. Simply put, the fact that Watanabe Sato has more cash than debt is arguably a good indication that it can manage its debt safely.

In addition to that, we're happy to report that Watanabe Sato has boosted its EBIT by 46%, thus reducing the spectre of future debt repayments. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since Watanabe Sato will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. Watanabe Sato may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. During the last three years, Watanabe Sato produced sturdy free cash flow equating to 78% of its EBIT, about what we'd expect. This cold hard cash means it can reduce its debt when it wants to.

Summing up

While we empathize with investors who find debt concerning, you should keep in mind that Watanabe Sato has net cash of JP¥4.72b, as well as more liquid assets than liabilities. And we liked the look of last year's 46% year-on-year EBIT growth. So is Watanabe Sato's debt a risk? It doesn't seem so to us. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. Be aware that Watanabe Sato is showing 2 warning signs in our investment analysis , and 1 of those is concerning...

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

If you decide to trade Watanabe Sato, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Watanabe Sato might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TSE:1807

Watanabe Sato

Engages in the contracting and investigation, research, planning, designing, supervision, technical guidance, and consultation of civil engineering construction activities.

Established dividend payer with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|19.7% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|87.9% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|20.5% undervalued

CH

Community Contributor