Advertisement

To find a multi-bagger stock, what are the underlying trends we should look for in a business? Firstly, we'd want to identify a growing return on capital employed (ROCE) and then alongside that, an ever-increasing base of capital employed. Basically this means that a company has profitable initiatives that it can continue to reinvest in, which is a trait of a compounding machine. That's why when we briefly looked at Watanabe Sato's (TYO:1807) ROCE trend, we were pretty happy with what we saw.

What is Return On Capital Employed (ROCE)?

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. The formula for this calculation on Watanabe Sato is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

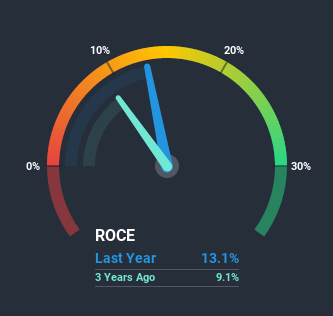

0.13 = JP¥2.7b ÷ (JP¥32b - JP¥12b) (Based on the trailing twelve months to December 2020).

Thus, Watanabe Sato has an ROCE of 13%. On its own, that's a standard return, however it's much better than the 10% generated by the Construction industry.

Check out our latest analysis for Watanabe Sato

While the past is not representative of the future, it can be helpful to know how a company has performed historically, which is why we have this chart above. If you're interested in investigating Watanabe Sato's past further, check out this free graph of past earnings, revenue and cash flow.

What Does the ROCE Trend For Watanabe Sato Tell Us?

While the returns on capital are good, they haven't moved much. The company has consistently earned 13% for the last five years, and the capital employed within the business has risen 29% in that time. 13% is a pretty standard return, and it provides some comfort knowing that Watanabe Sato has consistently earned this amount. Stable returns in this ballpark can be unexciting, but if they can be maintained over the long run, they often provide nice rewards to shareholders.

One more thing to note, even though ROCE has remained relatively flat over the last five years, the reduction in current liabilities to 36% of total assets, is good to see from a business owner's perspective. Effectively suppliers now fund less of the business, which can lower some elements of risk.

Our Take On Watanabe Sato's ROCE

To sum it up, Watanabe Sato has simply been reinvesting capital steadily, at those decent rates of return. On top of that, the stock has rewarded shareholders with a remarkable 139% return to those who've held over the last five years. So even though the stock might be more "expensive" than it was before, we think the strong fundamentals warrant this stock for further research.

Since virtually every company faces some risks, it's worth knowing what they are, and we've spotted 3 warning signs for Watanabe Sato (of which 1 makes us a bit uncomfortable!) that you should know about.

For those who like to invest in solid companies, check out this free list of companies with solid balance sheets and high returns on equity.

When trading Watanabe Sato or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Watanabe Sato might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TSE:1807

Watanabe Sato

Engages in the contracting and investigation, research, planning, designing, supervision, technical guidance, and consultation of civil engineering construction activities.

Established dividend payer with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|19.7% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|87.9% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|20.5% undervalued

CH

Community Contributor