Advertisement

- Japan

- /

- Construction

- /

- TSE:1871

Undiscovered Gems With Strong Fundamentals In January 2025

Simply Wall St

Reviewed by Simply Wall St

As we enter 2025, global markets are navigating a complex landscape marked by mixed performances in major indices and economic indicators that suggest both opportunities and challenges. While the S&P 500 capped off an impressive two-year growth streak, recent contractions in manufacturing activity and downward GDP revisions highlight areas of concern, especially for small-cap companies that often feel these pressures acutely. In this environment, identifying stocks with strong fundamentals becomes crucial as they can offer resilience amid volatility and potential for growth despite broader market uncertainties.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Canal Shipping Agencies | NA | 8.92% | 22.01% | ★★★★★★ |

| Sugar Terminals | NA | 3.14% | 3.53% | ★★★★★★ |

| Mendelson Infrastructures & Industries | 32.64% | 6.72% | 15.39% | ★★★★★★ |

| Payton Industries | NA | 9.27% | 15.41% | ★★★★★★ |

| Suez Canal Company for Technology Settling (S.A.E) | NA | 22.31% | 13.60% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Aesler Grup Internasional | NA | -17.61% | -40.21% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| Jamuna Bank | 85.07% | 7.37% | -3.87% | ★★★★☆☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

Let's explore several standout options from the results in the screener.

Formula Systems (1985) (TASE:FORTY)

Simply Wall St Value Rating: ★★★★★★

Overview: Formula Systems (1985) Ltd. operates through its subsidiaries to offer a range of software solutions, IT professional services, software product marketing and support, computer infrastructure and integration solutions, with a market cap of ₪4.76 billion.

Operations: Formula Systems generates revenue primarily through its subsidiaries offering software solutions, IT services, and integration solutions. The company focuses on both proprietary and non-proprietary offerings, contributing to diverse income streams. It has a market cap of approximately ₪4.76 billion.

Formula Systems (1985) showcases its potential with a notable increase in earnings, reporting US$23.62 million for the third quarter of 2024, up from US$15.6 million the previous year. This growth is further reflected in its basic earnings per share from continuing operations, which rose to US$1.55 from US$1.02 year-on-year. Over nine months, sales reached approximately US$2 billion compared to about US$1.98 billion previously, indicating steady progress despite industry challenges. The company's price-to-earnings ratio of 17x remains competitive within the IT sector's average of 18x, suggesting it might be undervalued relative to peers.

PS Construction (TSE:1871)

Simply Wall St Value Rating: ★★★★★☆

Overview: PS Construction Co., Ltd. operates in the civil engineering and architecture sectors both domestically in Japan and internationally, with a market capitalization of ¥52.04 billion.

Operations: PS Construction generates revenue primarily from its Civil Engineering Business, which accounts for ¥80.43 billion, and its Construction Business, contributing ¥53.77 billion. The Manufacturing Business adds a smaller portion of ¥7.48 billion to the company's total revenue streams.

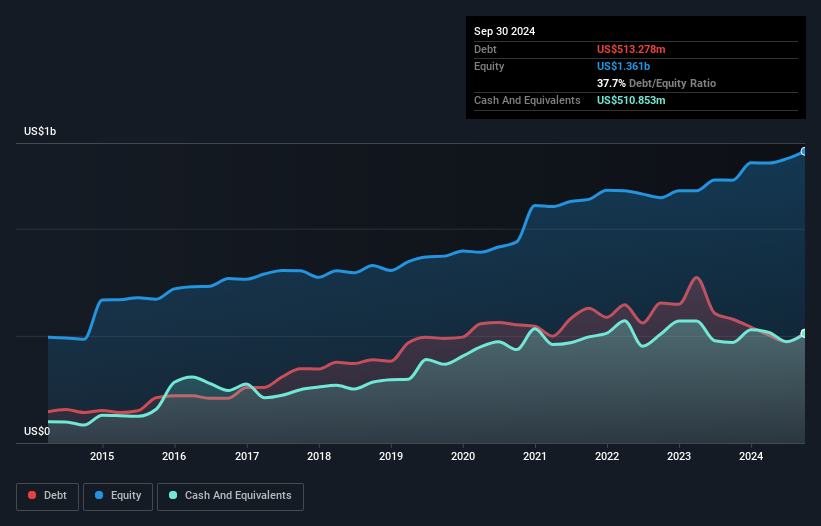

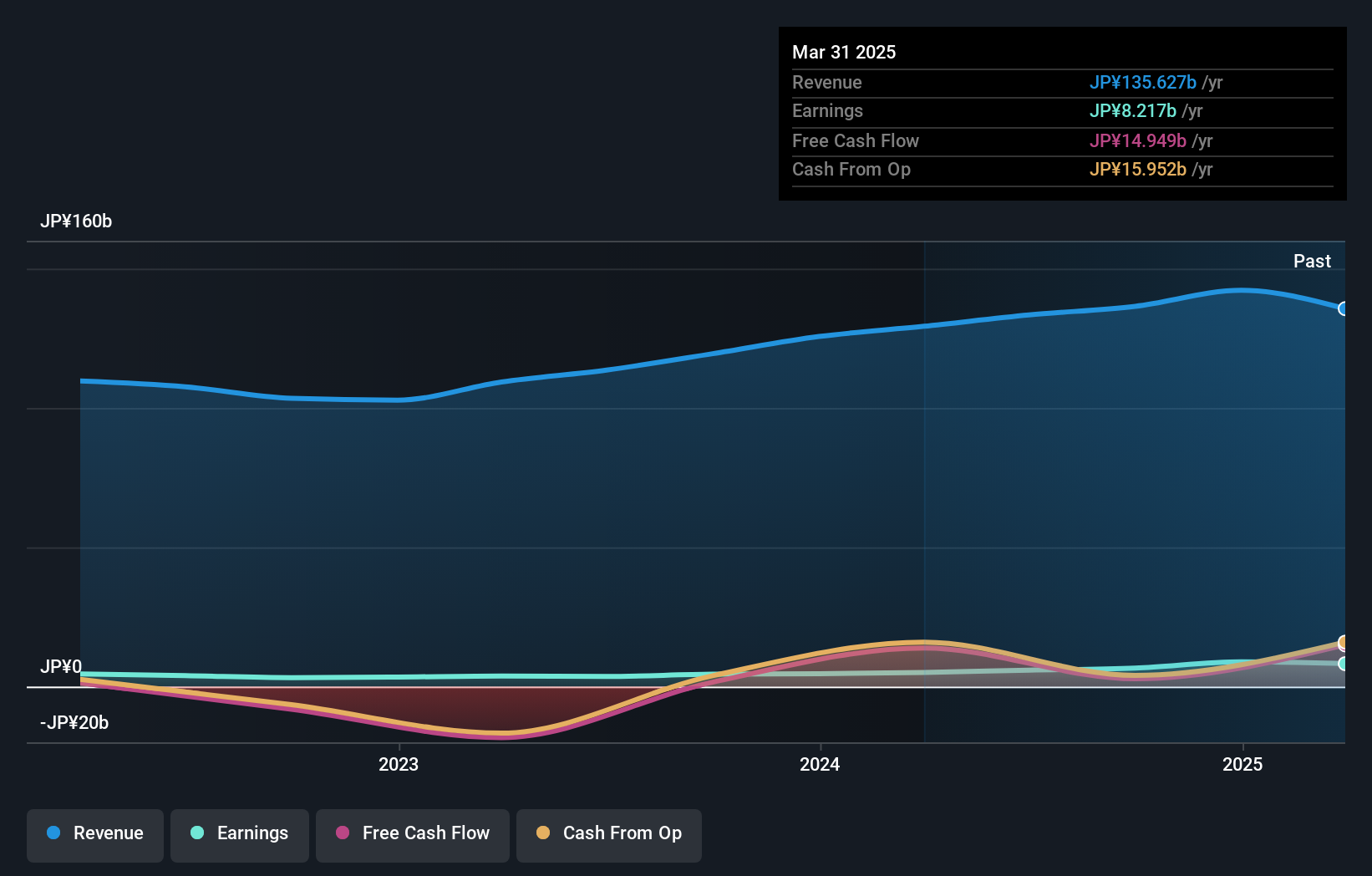

PS Construction stands out with its earnings growth of 49%, outperforming the construction industry's 21% over the past year. The company shows a robust interest coverage, with EBIT covering interest payments 83 times, indicating strong financial health. Despite a rise in debt to equity ratio from 12.5% to 29% over five years, it remains satisfactory at under 40%. The price-to-earnings ratio of 8 is appealing against Japan's market average of nearly 14. While earnings have seen an annual dip of about 4% over five years, its high-quality earnings and positive free cash flow suggest resilience and potential for future stability.

- Dive into the specifics of PS Construction here with our thorough health report.

Gain insights into PS Construction's past trends and performance with our Past report.

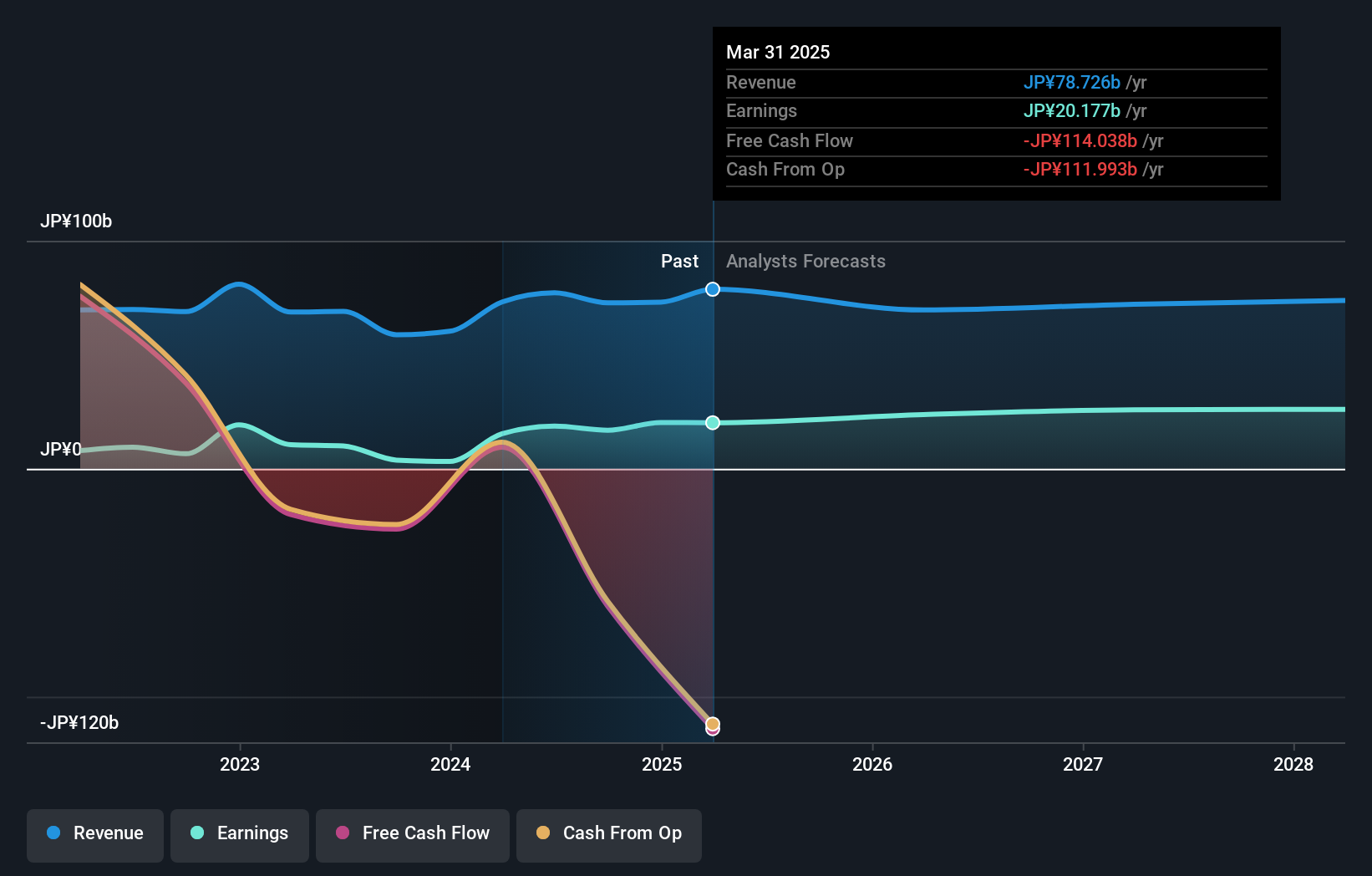

Suruga Bank (TSE:8358)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Suruga Bank Ltd. offers a range of banking and financial services to individual and corporate clients in Japan, with a market capitalization of ¥210.60 billion.

Operations: Suruga Bank generates revenue primarily from its banking segment, amounting to ¥82.04 billion. The net profit margin for the company is a key financial metric to observe, reflecting its profitability after accounting for all expenses.

Suruga Bank, a smaller player in Japan's banking sector, showcases a compelling mix of strengths and challenges. It boasts total assets of ¥3.44 trillion and total equity of ¥297.2 billion, while its deposits stand at ¥3.13 trillion against loans of ¥2.12 trillion with a net interest margin of 1.9%. Despite high non-performing loans at 8.9%, the bank’s liabilities are largely low risk due to customer deposits being the primary funding source. The price-to-earnings ratio is attractively below the market average at 12.6x, suggesting potential value for investors seeking growth opportunities in this niche space.

- Delve into the full analysis health report here for a deeper understanding of Suruga Bank.

Assess Suruga Bank's past performance with our detailed historical performance reports.

Seize The Opportunity

- Click through to start exploring the rest of the 4664 Undiscovered Gems With Strong Fundamentals now.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:1871

PS Construction

Engages in the civil engineering and architecture businesses in Japan and internationally.

6 star dividend payer with solid track record.

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|36.2% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|22.0% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|46.4% overvalued

DA

Community Contributor