Advertisement

Chugin Financial GroupInc (TSE:5832) Will Pay A Dividend Of ¥29.50

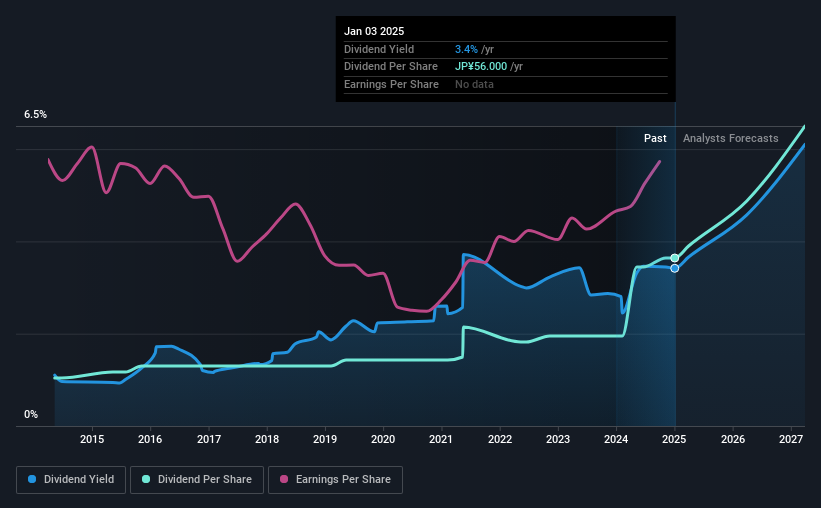

Chugin Financial Group,Inc.'s (TSE:5832) investors are due to receive a payment of ¥29.50 per share on 27th of June. The dividend yield will be in the average range for the industry at 3.4%.

See our latest analysis for Chugin Financial GroupInc

Chugin Financial GroupInc's Dividend Forecasted To Be Well Covered By Earnings

We like a dividend to be consistent over the long term, so checking whether it is sustainable is important.

Chugin Financial GroupInc has established itself as a dividend paying company with over 10 years history of distributing earnings to shareholders. Taking data from its last earnings report, calculating for the company's payout ratio shows 33%, which means that Chugin Financial GroupInc would be able to pay its last dividend without pressure on the balance sheet.

Looking forward, earnings per share is forecast to rise by 16.6% over the next year. Assuming the dividend continues along recent trends, we think the future payout ratio could be 36% by next year, which is in a pretty sustainable range.

Chugin Financial GroupInc Has A Solid Track Record

The company has a sustained record of paying dividends with very little fluctuation. Since 2015, the dividend has gone from ¥16.00 total annually to ¥56.00. This means that it has been growing its distributions at 13% per annum over that time. So, dividends have been growing pretty quickly, and even more impressively, they haven't experienced any notable falls during this period.

The Dividend Looks Likely To Grow

Investors who have held shares in the company for the past few years will be happy with the dividend income they have received. We are encouraged to see that Chugin Financial GroupInc has grown earnings per share at 12% per year over the past five years. With a decent amount of growth and a low payout ratio, we think this bodes well for Chugin Financial GroupInc's prospects of growing its dividend payments in the future.

We Really Like Chugin Financial GroupInc's Dividend

Overall, we think that Chugin Financial GroupInc could be a great option for a dividend investment, although we would have preferred if the dividend wasn't cut this year. Reducing the amount it is paying as a dividend can protect the company's balance sheet, keeping the dividend sustainable for longer. All of these factors considered, we think this has solid potential as a dividend stock.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. Are management backing themselves to deliver performance? Check their shareholdings in Chugin Financial GroupInc in our latest insider ownership analysis. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:5832

Chugin Financial GroupInc

Through its subsidiary The Chugoku Bank, Limited, provides various financial services to corporate and individual customers in Japan.

Solid track record with reasonable growth potential and pays a dividend.

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|35.7% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|20.5% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|25.2% overvalued

DA

Community Contributor