Subaru (TSE:7270) is turning heads after another sharp move in its share price, leaving investors wondering what is driving this momentum. While there is no clear single event or headline making waves, the company’s recent trajectory has certainly sparked a wave of curiosity. For anyone on the fence about buying, selling, or sitting tight, moments like these can feel like a wake-up call to dig deeper into Subaru’s underlying story.

Taking a step back, Subaru’s stock has delivered an impressive ride over the past year, with shares rising 31% on a total return basis. The momentum is especially clear over the past 3 months, as the stock climbed over 22%, strongly outpacing much of the broader auto sector. This performance stands out even more when set against Subaru’s modest revenue growth and a drop in net income over the last year. This underscores a disconnect that is hard to ignore.

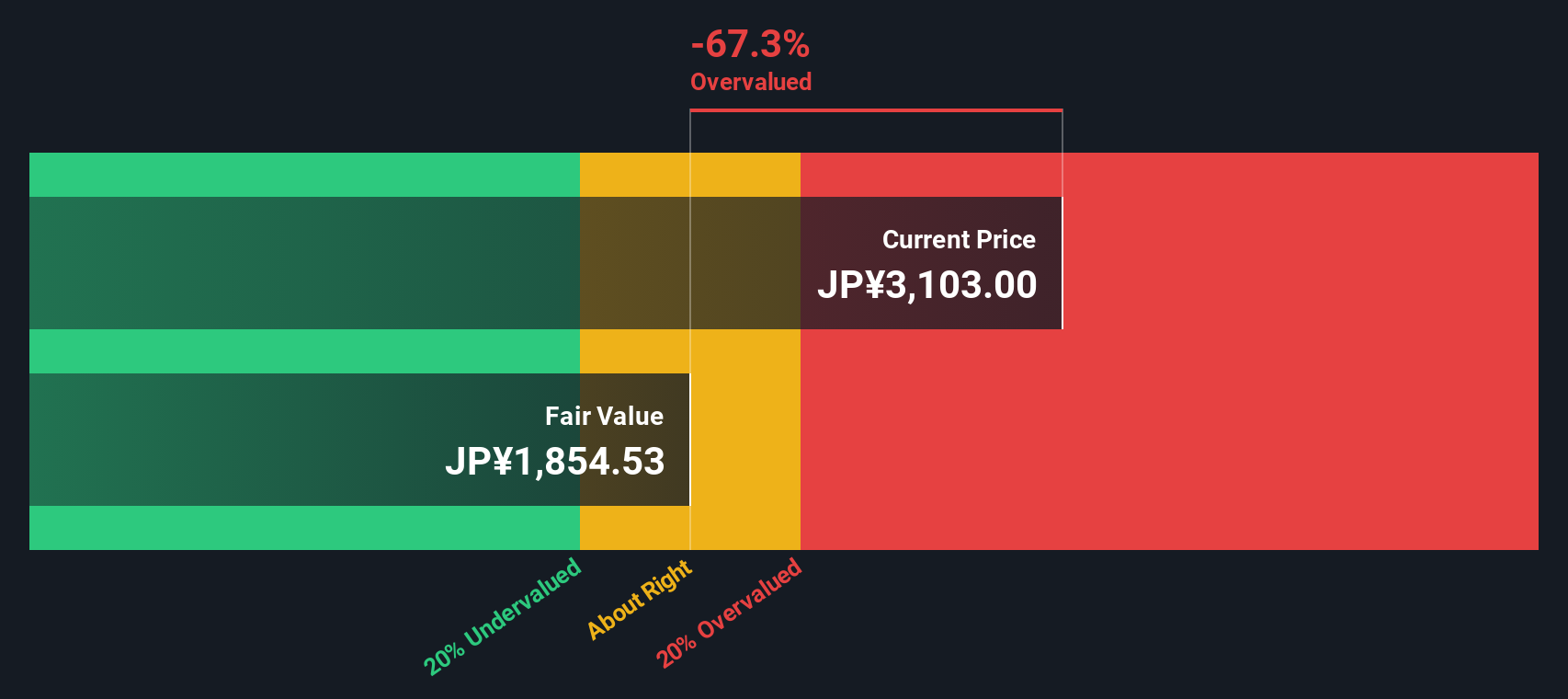

With the recent rally and a valuation gap in plain sight, some investors may be asking whether Subaru is a bargain or if the market is pricing in bold growth ahead.

Advertisement

Price-to-Earnings of 7.4x: Is it justified?

Subaru appears significantly undervalued based on its price-to-earnings (P/E) ratio, which stands at 7.4 times earnings. This is well below both the Japanese market average of 14.7x and the Asian auto industry average of 21x.

The price-to-earnings multiple is a fundamental valuation tool that helps investors understand how much they are paying for each yen of company earnings. For an established automaker like Subaru, a lower P/E ratio could suggest that investors are skeptical of future growth or are discounting potential risks. In comparison, a higher ratio would typically indicate optimism for sustained profits or expansion.

Given Subaru's P/E discount to both local and sector peers, the market may be underestimating its ability to deliver long-term shareholder value. The justification for this multiple will depend on whether recent performance and future prospects align with this low valuation. This may warrant a closer look at the company's earnings momentum and underlying fundamentals.

However, risks remain, including weak net income growth and a sizable decline from analysts' price targets. These factors could challenge the bullish outlook.

While the market approach based on earnings suggests Subaru looks attractively priced, our DCF model tells a different story. The model indicates the shares may be trading above their intrinsic value. Could expectations be running ahead of fundamentals?

Confidently open up your investing horizons and capture new opportunities at the forefront of innovation and value. Don’t let standout stocks pass you by.

Unlock value and spot hidden gems by tapping into the latest lineup of stocks trading below their intrinsic worth with undervalued stocks based on cash flows.

Ride the next artificial intelligence wave by zeroing in on fast-rising companies at the heart of AI breakthroughs using AI penny stocks.

Power up your portfolio with dependable income by targeting companies with strong yield potential through dividend stocks with yields > 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency • Be alerted to new Warning Signs or Risks via email or mobile • Track the Fair Value of your stocks

Kshitija (or Keisha) Bhandaru is an Equity Analyst at Simply Wall St and has over 6 years of experience in the finance industry and describes herself as a lifelong learner driven by her intellectual curiosity. She previously worked with Market Realist for 5 years as an Equity Analyst.