Enel (BIT:ENEL) shares have been quietly climbing in recent weeks, with a 5% gain over the past month. Investors seem interested in the utility’s steady returns and consistent revenue growth as broader markets fluctuate.

Enel’s steady climb this month is part of a longer-term trend, as the stock has delivered a solid 1-year total shareholder return of 26%. This shows momentum is building as investors grow more comfortable with its earnings and growth outlook.

But with Enel shares near their recent highs and trading just below analysts’ price targets, investors may wonder if there is still room for upside or if the market has already factored in the company’s future growth.

Advertisement

Most Popular Narrative: 3.3% Undervalued

Enel’s most followed narrative suggests its fair value sits just above the current price, hinting at some remaining upside. The fair value is set at €8.49, compared to the latest close of €8.21, with analysts factoring in both growth prospects and sector risks.

*Enel's significant investment in digitalization (e.g., smart grids, automation, BESS capacity now at 11.5GW) and grid modernization is yielding improved operational efficiency. This is evidenced by €1 billion in cash cost savings already realized toward its 2027 target, supporting margin expansion and sustained net income improvement.*

Curious what earnings projections and profit margin targets push this valuation higher? The next move might surprise you. See how analysts are building a case for growth and discover the financial levers that could redefine Enel’s future payout and price potential.

However, persistent currency volatility or regulatory changes in key European markets could present challenges to Enel's growth optimism and put pressure on its profit outlook.

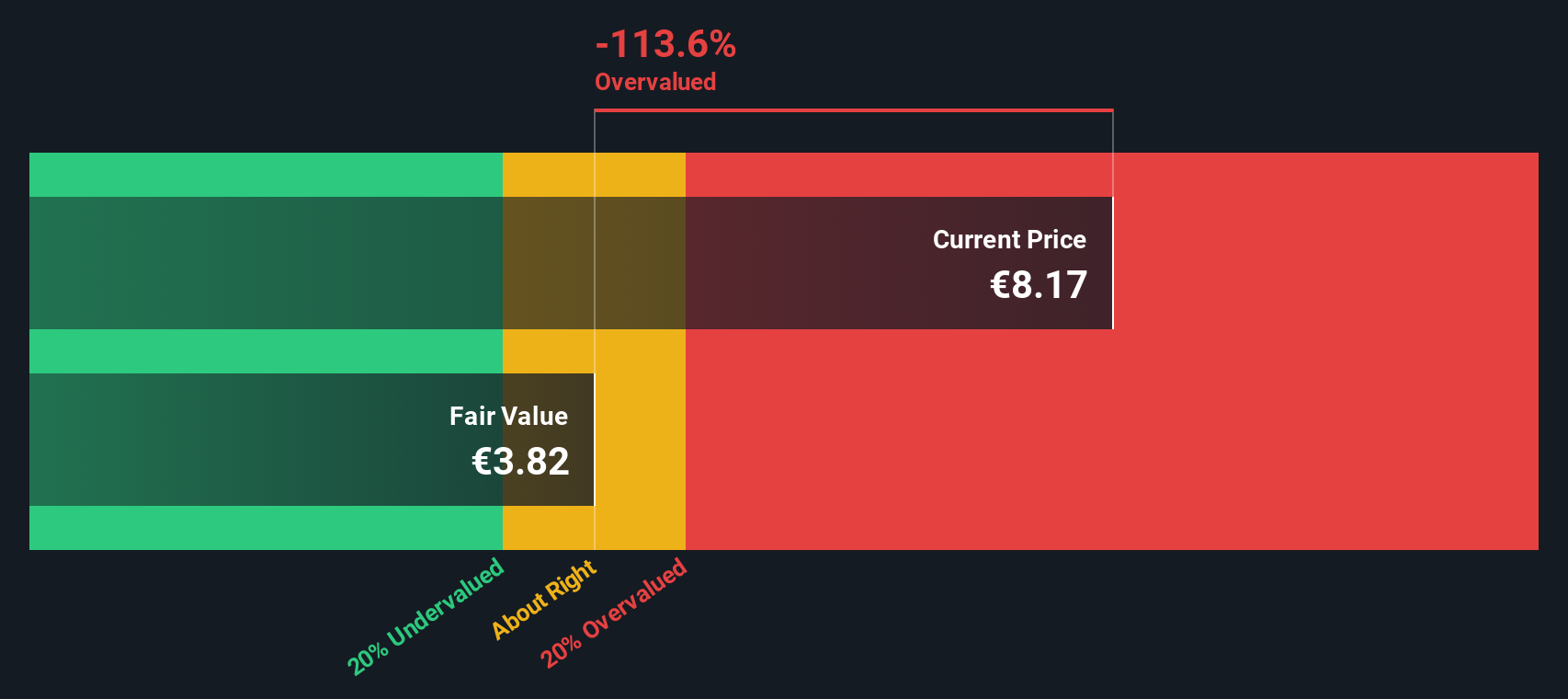

Taking a different approach, our DCF model offers a more cautious outlook than the multiples-based valuation. The SWS DCF model estimates Enel’s fair value to be much lower than its current price, suggesting the shares may be overvalued if you weigh cash flow projections more heavily. This raises the question: do cash flows tell a different story than analyst optimism?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Enel for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Enel Narrative

If you want to take a hands-on approach or see things differently, you can craft your own narrative using the available data in just a few minutes. Do it your way.

Sharpen your portfolio with unique opportunities you might have overlooked. The right investment at the right time could give you the edge over the crowd.

Unlock tech innovation by tracking these 26 quantum computing stocks and their breakthroughs in quantum hardware, secure communication, and future-defining algorithms.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Enel might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.