- Italy

- /

- Telecom Services and Carriers

- /

- BIT:TIT

Telecom Italia S.p.A. (BIT:TIT) Looks Inexpensive After Falling 25% But Perhaps Not Attractive Enough

Telecom Italia S.p.A. (BIT:TIT) shareholders that were waiting for something to happen have been dealt a blow with a 25% share price drop in the last month. Instead of being rewarded, shareholders who have already held through the last twelve months are now sitting on a 26% share price drop.

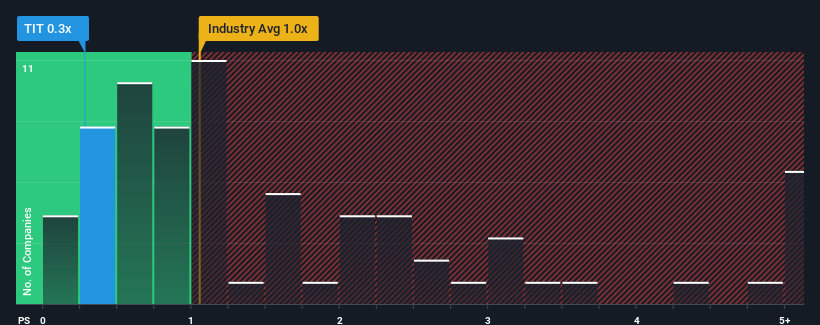

After such a large drop in price, Telecom Italia may be sending buy signals at present with its price-to-sales (or "P/S") ratio of 0.3x, considering almost half of all companies in the Telecom industry in Italy have P/S ratios greater than 1.1x and even P/S higher than 4x aren't out of the ordinary. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the reduced P/S.

View our latest analysis for Telecom Italia

How Telecom Italia Has Been Performing

Telecom Italia could be doing better as it's been growing revenue less than most other companies lately. The P/S ratio is probably low because investors think this lacklustre revenue performance isn't going to get any better. If this is the case, then existing shareholders will probably struggle to get excited about the future direction of the share price.

Keen to find out how analysts think Telecom Italia's future stacks up against the industry? In that case, our free report is a great place to start.Is There Any Revenue Growth Forecasted For Telecom Italia?

There's an inherent assumption that a company should underperform the industry for P/S ratios like Telecom Italia's to be considered reasonable.

Retrospectively, the last year delivered a decent 3.2% gain to the company's revenues. However, due to its less than impressive performance prior to this period, revenue growth is practically non-existent over the last three years overall. Accordingly, shareholders probably wouldn't have been overly satisfied with the unstable medium-term growth rates.

Shifting to the future, estimates from the ten analysts covering the company suggest revenue should grow by 0.2% per annum over the next three years. With the industry predicted to deliver 5.3% growth each year, the company is positioned for a weaker revenue result.

With this information, we can see why Telecom Italia is trading at a P/S lower than the industry. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

The Key Takeaway

Telecom Italia's recently weak share price has pulled its P/S back below other Telecom companies. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

We've established that Telecom Italia maintains its low P/S on the weakness of its forecast growth being lower than the wider industry, as expected. At this stage investors feel the potential for an improvement in revenue isn't great enough to justify a higher P/S ratio. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

You should always think about risks. Case in point, we've spotted 2 warning signs for Telecom Italia you should be aware of, and 1 of them shouldn't be ignored.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Valuation is complex, but we're here to simplify it.

Discover if Telecom Italia might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BIT:TIT

Telecom Italia

Engages in the provision of fixed and mobile telecommunications services in Italy and internationally.

Undervalued with moderate growth potential.

Similar Companies

Market Insights

Community Narratives