Advertisement

Reply (BIT:REY) Valuation Check After New Biological Computing And AI Robotics Projects

Reply (BIT:REY) has drawn fresh attention after two recent announcements: a research collaboration on biological computing with the University of Milan and a robotics orchestration project for Otto Group developed alongside NVIDIA.

See our latest analysis for Reply.

Despite the recent headlines around biological computing and AI robotics, Reply’s share price has come under pressure, with a 7 day share price return of 9.53% and a year to date share price return of 9.29% alongside a 1 year total shareholder return of 35.92%, pointing to weak recent momentum after a tougher stretch for longer term holders.

If these AI and automation themes interest you, it can be worth widening your research to other tech names and seeing what stands out across high growth tech and AI stocks.

With Reply shares under pressure despite its work in biological computing and AI robotics, the key question for you is whether this weakness is a reset that leaves upside open, or if the market is already pricing in future growth.

Price-to-Earnings of 14.2x: Is it justified?

Reply currently trades on a P/E of 14.2x, which screens as good value versus both peers and the wider European IT industry, even after the recent share price weakness.

The P/E ratio compares the company’s share price to its earnings per share and is a common way investors judge how much they are paying for each unit of profit, especially for profitable, established software and IT services businesses like Reply.

According to the data, Reply’s P/E of 14.2x is below the peer average of 31.9x and below the European IT industry average of 20x. It also sits under an estimated “fair” P/E of 23.7x that our model suggests the market could move towards if sentiment and fundamentals align.

This combination of a lower multiple than sector peers and an estimated fair ratio that is higher than today’s level suggests the market is pricing Reply’s earnings more cautiously than both its direct peers and what the fair ratio work implies.

Explore the SWS fair ratio for Reply

Result: Price-to-Earnings of 14.2x (UNDERVALUED)

However, you should weigh risks such as recent negative 1 year and multi year total returns, and the possibility that AI projects may take longer to translate into earnings.

Find out about the key risks to this Reply narrative.

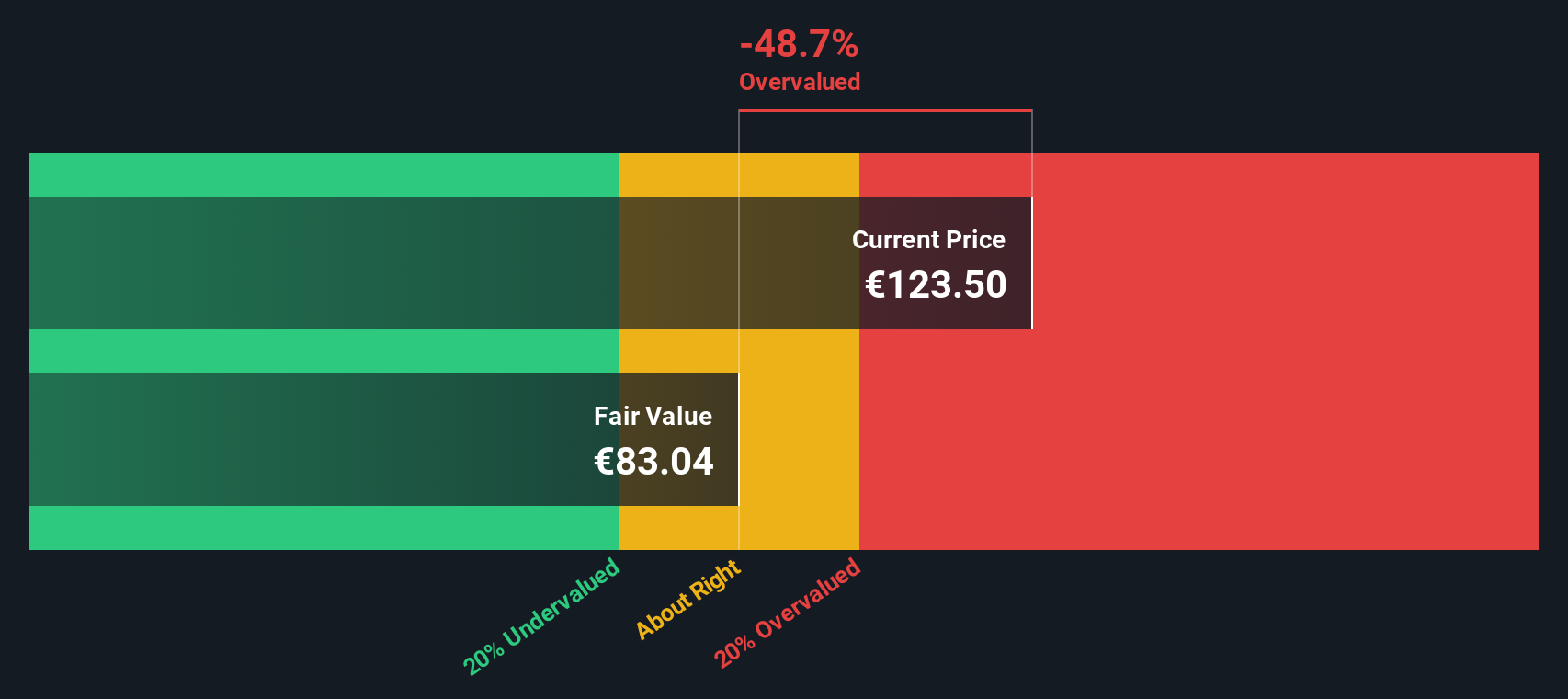

Another view through the SWS DCF model

While the P/E of 14.2x screens as attractive, our DCF model paints a different picture, with Reply at €100.6 compared to an estimated future cash flow value of €87.7, which points to an overvalued result on this measure.

This gap suggests the market may be assigning Reply a richer price than its projected cash flows support, especially if earnings grow closer to the 5.74% annual forecast. Which lens do you find more compelling when you weigh up the risk and potential reward?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Reply for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 867 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Reply Narrative

If you see the numbers differently, or simply want to stress test these assumptions, you can build your own view in just a few minutes using Do it your way.

A good starting point is our analysis highlighting 5 key rewards investors are optimistic about regarding Reply.

Looking for more investment ideas?

If Reply is on your radar, do not stop there. Broaden your watchlist so you are ready when other opportunities line up with your approach.

- Spot potential value by screening for companies trading below estimated cash flow, starting with these 867 undervalued stocks based on cash flows that match your preferred fundamentals.

- Target income focused ideas by scanning these 11 dividend stocks with yields > 3% that may suit a portfolio built around regular cash returns.

- Lean into high growth themes with these 29 AI penny stocks that could align with your view on future AI spending and adoption.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About BIT:REY

Reply

Provides consulting, system integration, and digital services based on communication channels and digital media in Italy and internationally.

Flawless balance sheet, undervalued and pays a dividend.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0775.1% undervalued

135 followersusers have followed this narrative

1 commentusers have commented on this narrative

22 likesusers have liked this narrative

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9822.7% undervalued

43 followersusers have followed this narrative

0 commentsusers have commented on this narrative

33 likesusers have liked this narrative

KO

Kouj on CSL ·

CSL: The Dip Is the Opportunity

Fair Value:AU$1559.0% undervalued

19 followersusers have followed this narrative

0 commentsusers have commented on this narrative

13 likesusers have liked this narrative

GA

GavrielH on DHT Holdings ·

DHT Holdings, inc: Strait of Hormuz Risk Amidst US-Israel vs Iran Tensions Spikes VLCC Rates.

Fair Value:US$3653.2% undervalued

15 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

EL

elizabao on Welltower ·

Leveraging the Senior Housing Supply Gap

Fair Value:US$228.148.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VE

Vestra on Fortinet ·

Fortinet, Inc. (FTNT): Navigating the Firewall Refresh Cycle and the SASE AI Pivot

Fair Value:US$87.044.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VE

Vestra on ASML Holding ·

ASML Holding N.V. (ASML): The Lithography Monopoly and the High-NA EUV AI Era

Fair Value:€1.29k8.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

KA

kabz2342 on Nu Holdings ·

Nu holdings will continue to disrupt the South American banking market

Fair Value:US$64.378.4% undervalued

53 followersusers have followed this narrative

3 commentsusers have commented on this narrative

29 likesusers have liked this narrative

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9822.7% undervalued

43 followersusers have followed this narrative

0 commentsusers have commented on this narrative

33 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$59633.6% undervalued

1310 followersusers have followed this narrative

2 commentsusers have commented on this narrative

10 likesusers have liked this narrative

Trending Discussion

DA

daqui_luis on Corticeira Amorim S.G.P.S ·

Great analysis on a great and solid company with a dominant position in the Cork Market.

1

|0