Advertisement

- Italy

- /

- Retail Distributors

- /

- BIT:RMT

Some Investors May Be Worried About Riba Mundo Tecnología's (BIT:RMT) Returns On Capital

If we want to find a stock that could multiply over the long term, what are the underlying trends we should look for? In a perfect world, we'd like to see a company investing more capital into its business and ideally the returns earned from that capital are also increasing. Basically this means that a company has profitable initiatives that it can continue to reinvest in, which is a trait of a compounding machine. In light of that, when we looked at Riba Mundo Tecnología (BIT:RMT) and its ROCE trend, we weren't exactly thrilled.

Return On Capital Employed (ROCE): What Is It?

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. The formula for this calculation on Riba Mundo Tecnología is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.16 = €7.0m ÷ (€97m - €55m) (Based on the trailing twelve months to June 2024).

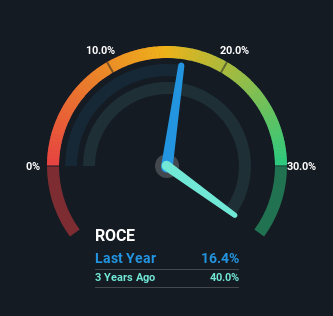

So, Riba Mundo Tecnología has an ROCE of 16%. In absolute terms, that's a satisfactory return, but compared to the Retail Distributors industry average of 11% it's much better.

Check out our latest analysis for Riba Mundo Tecnología

Historical performance is a great place to start when researching a stock so above you can see the gauge for Riba Mundo Tecnología's ROCE against it's prior returns. If you're interested in investigating Riba Mundo Tecnología's past further, check out this free graph covering Riba Mundo Tecnología's past earnings, revenue and cash flow.

What Does the ROCE Trend For Riba Mundo Tecnología Tell Us?

The trend of ROCE doesn't look fantastic because it's fallen from 40% three years ago, while the business's capital employed increased by 669%. That being said, Riba Mundo Tecnología raised some capital prior to their latest results being released, so that could partly explain the increase in capital employed. It's unlikely that all of the funds raised have been put to work yet, so as a consequence Riba Mundo Tecnología might not have received a full period of earnings contribution from it.

On a related note, Riba Mundo Tecnología has decreased its current liabilities to 56% of total assets. So we could link some of this to the decrease in ROCE. Effectively this means their suppliers or short-term creditors are funding less of the business, which reduces some elements of risk. Some would claim this reduces the business' efficiency at generating ROCE since it is now funding more of the operations with its own money. Keep in mind 56% is still pretty high, so those risks are still somewhat prevalent.

What We Can Learn From Riba Mundo Tecnología's ROCE

While returns have fallen for Riba Mundo Tecnología in recent times, we're encouraged to see that sales are growing and that the business is reinvesting in its operations. Despite these promising trends, the stock has collapsed 85% over the last year, so there could be other factors hurting the company's prospects. Therefore, we'd suggest researching the stock further to uncover more about the business.

Riba Mundo Tecnología does have some risks, we noticed 7 warning signs (and 5 which don't sit too well with us) we think you should know about.

While Riba Mundo Tecnología may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BIT:RMT

Riba Mundo Tecnología

Engages in the purchase and resale of consumer electronic products in the United States, the United Kingdom, rest of Europe, and the United Arab Emirates.

Slight risk and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|35.1% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|89.8% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|15.2% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|96.0% undervalued

AG

Community Contributor