Advertisement

- Italy

- /

- Consumer Durables

- /

- BIT:RAD

Radici Pietro Industries & Brands (BIT:RAD) Has More To Do To Multiply In Value Going Forward

What are the early trends we should look for to identify a stock that could multiply in value over the long term? Typically, we'll want to notice a trend of growing return on capital employed (ROCE) and alongside that, an expanding base of capital employed. This shows us that it's a compounding machine, able to continually reinvest its earnings back into the business and generate higher returns. However, after investigating Radici Pietro Industries & Brands (BIT:RAD), we don't think it's current trends fit the mold of a multi-bagger.

Return On Capital Employed (ROCE): What Is It?

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. To calculate this metric for Radici Pietro Industries & Brands, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

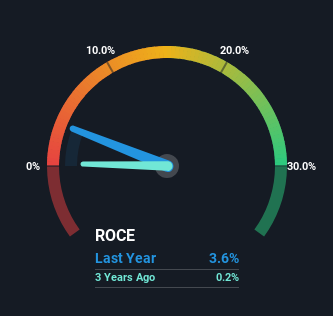

0.036 = €1.5m ÷ (€71m - €29m) (Based on the trailing twelve months to December 2023).

Thus, Radici Pietro Industries & Brands has an ROCE of 3.6%. In absolute terms, that's a low return and it also under-performs the Consumer Durables industry average of 9.4%.

See our latest analysis for Radici Pietro Industries & Brands

In the above chart we have measured Radici Pietro Industries & Brands' prior ROCE against its prior performance, but the future is arguably more important. If you'd like to see what analysts are forecasting going forward, you should check out our free analyst report for Radici Pietro Industries & Brands .

So How Is Radici Pietro Industries & Brands' ROCE Trending?

Over the past five years, Radici Pietro Industries & Brands' ROCE has remained relatively flat while the business is using 35% less capital than before. To us that doesn't look like a multi-bagger because the company appears to be selling assets and it's returns aren't increasing. Not only that, but the low returns on this capital mentioned earlier would leave most investors unimpressed.

On another note, while the change in ROCE trend might not scream for attention, it's interesting that the current liabilities have actually gone up over the last five years. This is intriguing because if current liabilities hadn't increased to 41% of total assets, this reported ROCE would probably be less than3.6% because total capital employed would be higher.The 3.6% ROCE could be even lower if current liabilities weren't 41% of total assets, because the the formula would show a larger base of total capital employed. So with current liabilities at such high levels, this effectively means the likes of suppliers or short-term creditors are funding a meaningful part of the business, which in some instances can bring some risks.

Our Take On Radici Pietro Industries & Brands' ROCE

Overall, we're not ecstatic to see Radici Pietro Industries & Brands reducing the amount of capital it employs in the business. And investors appear hesitant that the trends will pick up because the stock has fallen 61% in the last five years. In any case, the stock doesn't have these traits of a multi-bagger discussed above, so if that's what you're looking for, we think you'd have more luck elsewhere.

Since virtually every company faces some risks, it's worth knowing what they are, and we've spotted 4 warning signs for Radici Pietro Industries & Brands (of which 3 are a bit unpleasant!) that you should know about.

For those who like to invest in solid companies, check out this free list of companies with solid balance sheets and high returns on equity.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About BIT:RAD

Radici Pietro Industries & Brands

Engages in the production and distribution of woven and non-woven textile coverings worldwide.

Undervalued with excellent balance sheet.

Market Insights

Advertisement

Community Narratives

100% Patient Improvement in trial puts this $16M Biotech on the radar

Fair Value US$5.30|69.8% undervalued

JO

Community Contributor

Exxon Mobil's 17.5% Upside Promises Industry-Leading Returns in Energy Transition

Fair Value US$132.00|15.0% undervalued

HE

Community Contributor

NHC Analysis: Quality at a Good Price. A Golden Opportunity?

Fair Value US$179.80|35.9% undervalued

DA

Community Contributor

Product Refresh And Global Expansion Will Empower Future Market Leadership

Fair Value US$202.60|0% overvalued

AN

Based on Analyst Price Targets