Advertisement

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We note that Aeffe S.p.A. (BIT:AEF) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we examine debt levels, we first consider both cash and debt levels, together.

View our latest analysis for Aeffe

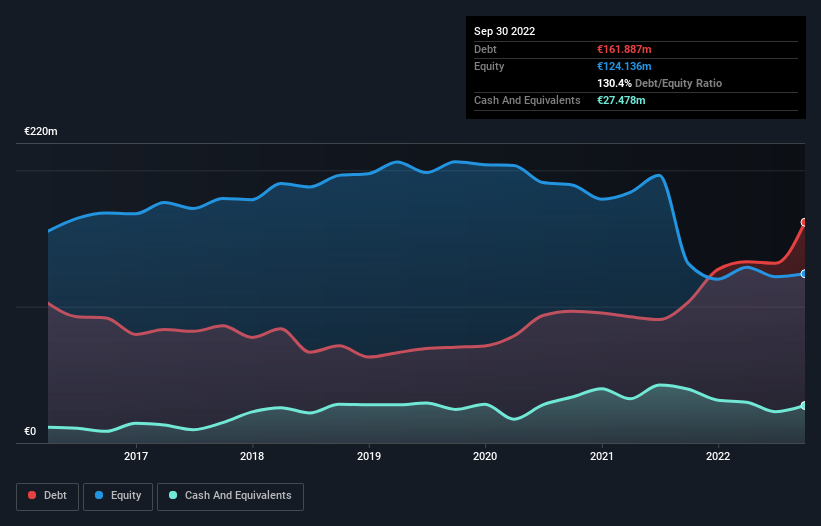

How Much Debt Does Aeffe Carry?

You can click the graphic below for the historical numbers, but it shows that as of September 2022 Aeffe had €161.9m of debt, an increase on €103.5m, over one year. However, it does have €27.5m in cash offsetting this, leading to net debt of about €134.4m.

How Healthy Is Aeffe's Balance Sheet?

We can see from the most recent balance sheet that Aeffe had liabilities of €203.3m falling due within a year, and liabilities of €170.7m due beyond that. Offsetting this, it had €27.5m in cash and €115.9m in receivables that were due within 12 months. So it has liabilities totalling €230.6m more than its cash and near-term receivables, combined.

This deficit casts a shadow over the €117.2m company, like a colossus towering over mere mortals. So we'd watch its balance sheet closely, without a doubt. After all, Aeffe would likely require a major re-capitalisation if it had to pay its creditors today.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

With a net debt to EBITDA ratio of 7.2, it's fair to say Aeffe does have a significant amount of debt. However, its interest coverage of 2.6 is reasonably strong, which is a good sign. Notably, Aeffe's EBIT was pretty flat over the last year, which isn't ideal given the debt load. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Aeffe's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So it's worth checking how much of that EBIT is backed by free cash flow. Happily for any shareholders, Aeffe actually produced more free cash flow than EBIT over the last two years. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Our View

To be frank both Aeffe's net debt to EBITDA and its track record of staying on top of its total liabilities make us rather uncomfortable with its debt levels. But at least it's pretty decent at converting EBIT to free cash flow; that's encouraging. Looking at the bigger picture, it seems clear to us that Aeffe's use of debt is creating risks for the company. If all goes well, that should boost returns, but on the flip side, the risk of permanent capital loss is elevated by the debt. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. We've identified 1 warning sign with Aeffe , and understanding them should be part of your investment process.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BIT:AEF

Aeffe

Engages in the design, production, and distribution of fashion and luxury goods worldwide.

Moderate risk and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RI

Rick_Orford on Upside Gold ·

This OVERLOOKED Gold Stock Could TRIPLE - 3.3M Ounces, Bottom-of-Peer Valuation

Fair Value:CA$470.5% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9719.1% undervalued

54 followersusers have followed this narrative

0 commentsusers have commented on this narrative

13 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1925.7% undervalued

43 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative

BJ

Bjergby on PagSeguro Digital ·

PagSeguro: A Cheap Bet on a Bank Hiding Inside a Payments Company, Priced for Failure

Fair Value:US$19.251.3% undervalued

17 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

Recently Updated Narratives

HU

Hunter_Z on Catcha Digital Berhad ·

Catcha Digital Q1 FY2026 Analysis - Acquisition-led growth is starting to convert into stronger operating earnings

Fair Value:RM 0.5451.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

HU

Hunter_Z on SBS Nexus Berhad ·

SBS Nexus首季业绩被一次性费用掩盖,市场估值或低估其盈利质量

Fair Value:RM 0.09817.3% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

HU

Hunter_Z on GIIB Holdings Berhad ·

GIIB: New Shareholders Could Mark the Beginning of a Turnaround Reset

Fair Value:RM 0.633.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8589.4% undervalued

120 followersusers have followed this narrative

2 commentsusers have commented on this narrative

34 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9719.1% undervalued

54 followersusers have followed this narrative

0 commentsusers have commented on this narrative

13 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1925.7% undervalued

43 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative