Advertisement

- Italy

- /

- Diversified Financial

- /

- BIT:BFF

European Market: BFF Bank And 2 Other Stocks Trading At Estimated Discounts

Simply Wall St

Reviewed by Simply Wall St

As the European market navigates through a period of heightened global uncertainty, with indices such as the STOXX Europe 600 reflecting concerns over geopolitical tensions, investors are increasingly on the lookout for stocks that may be trading at a discount. In this environment, identifying undervalued stocks like BFF Bank and others can offer potential opportunities for those who focus on strong fundamentals and resilience amidst fluctuating economic conditions.

Top 10 Undervalued Stocks Based On Cash Flows In Europe

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| TTS (Transport Trade Services) (BVB:TTS) | RON4.36 | RON8.49 | 48.6% |

| Qt Group Oyj (HLSE:QTCOM) | €54.95 | €107.96 | 49.1% |

| Pluxee (ENXTPA:PLX) | €17.88 | €34.83 | 48.7% |

| PFISTERER Holding (XTRA:PFSE) | €39.50 | €78.15 | 49.5% |

| Lingotes Especiales (BME:LGT) | €6.00 | €11.87 | 49.4% |

| Laboratorios Farmaceuticos Rovi (BME:ROVI) | €53.50 | €104.47 | 48.8% |

| Koskisen Oyj (HLSE:KOSKI) | €8.84 | €17.31 | 48.9% |

| Galderma Group (SWX:GALD) | CHF113.20 | CHF221.57 | 48.9% |

| Absolent Air Care Group (OM:ABSO) | SEK209.00 | SEK415.74 | 49.7% |

| ABO Energy GmbH KGaA (XTRA:AB9) | €36.00 | €70.33 | 48.8% |

Let's take a closer look at a couple of our picks from the screened companies.

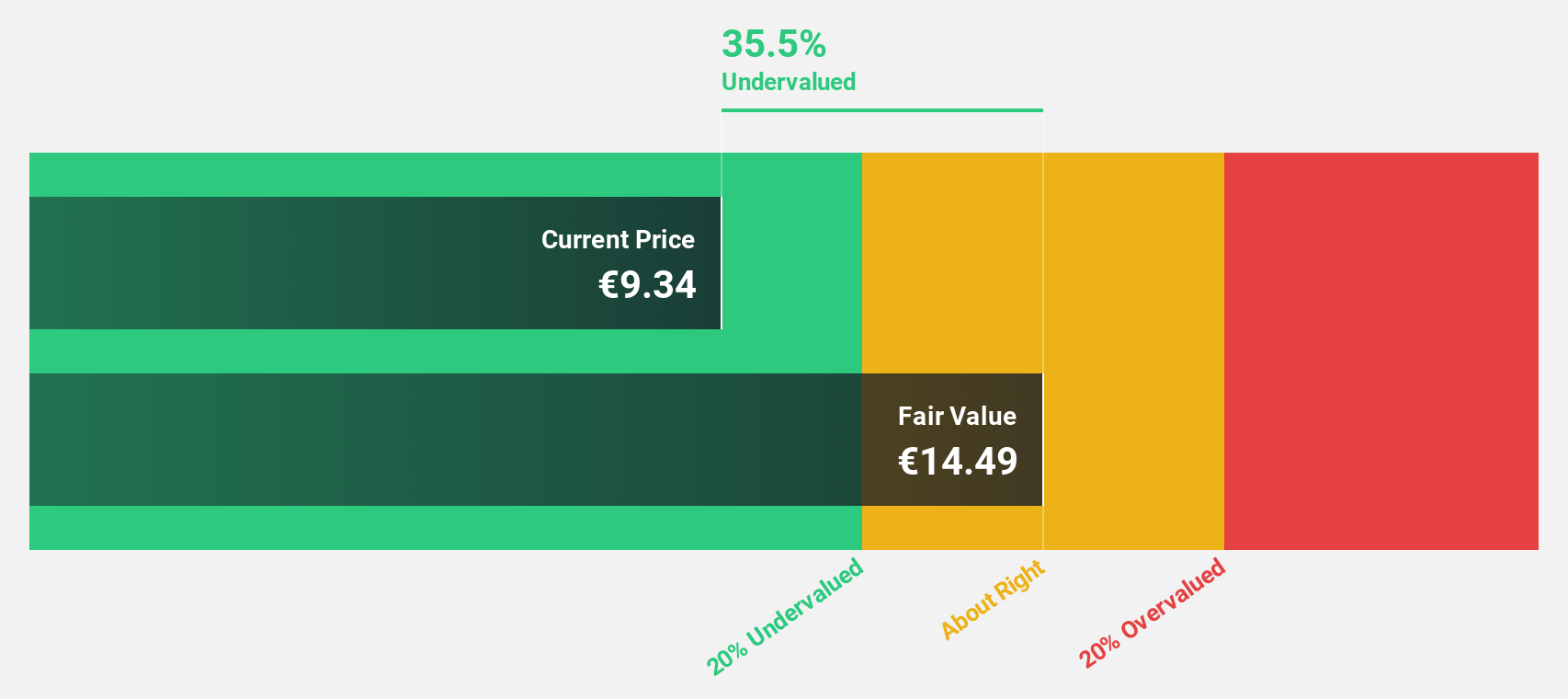

BFF Bank (BIT:BFF)

Overview: BFF Bank S.p.A. operates in non-recourse factoring and credit management for public administration bodies and private hospitals across several European countries, with a market cap of €1.72 billion.

Operations: The company's revenue is primarily derived from its Financial Services - Commercial segment, which generated €475.73 million.

Estimated Discount To Fair Value: 33.9%

BFF Bank appears undervalued, trading at €9.14, significantly below its estimated fair value of €13.83. Despite a high Return on Equity forecast of 26.2% in three years, the bank's debt isn't well-covered by operating cash flow and its 11.84% dividend is unsustainable with current free cash flows. Earnings grew by 30.3% last year but are expected to grow modestly at 6.6% annually, slightly above the Italian market's growth rate.

- According our earnings growth report, there's an indication that BFF Bank might be ready to expand.

- Click to explore a detailed breakdown of our findings in BFF Bank's balance sheet health report.

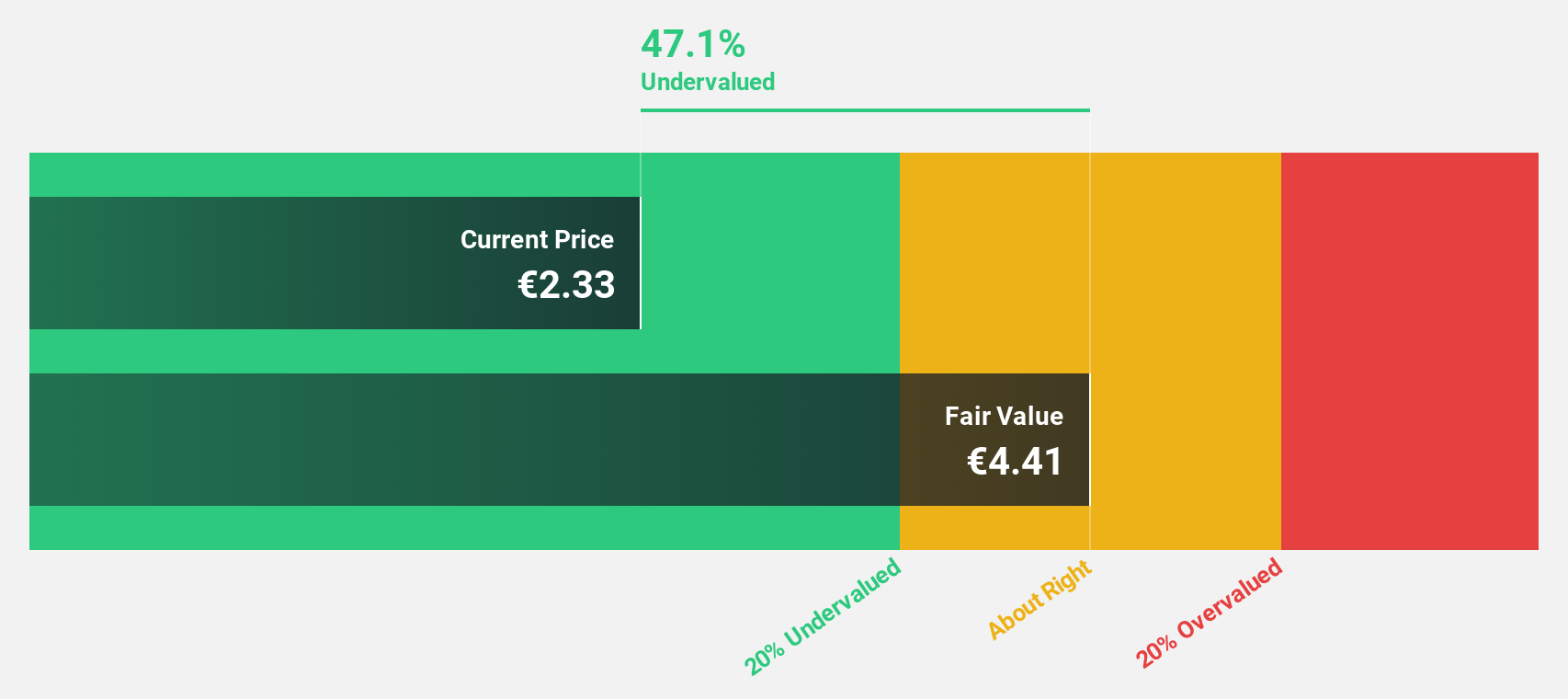

doValue (BIT:DOV)

Overview: doValue S.p.A. specializes in managing non-performing loans, unlikely to pay, early arrears, and performing loans for banks and investors across Italy, Spain, Greece, and Cyprus with a market cap of €447.80 million.

Operations: doValue S.p.A. generates revenue from managing non-performing loans, unlikely to pay, early arrears, and performing loans for financial institutions and investors in Italy, Spain, Greece, and Cyprus.

Estimated Discount To Fair Value: 48%

doValue is trading at €2.36, considerably below its estimated fair value of €4.54, suggesting significant undervaluation based on cash flows. The company's earnings are forecast to grow significantly at 59.1% annually, outpacing the Italian market's growth rate of 6.5%. However, doValue has experienced substantial shareholder dilution recently and faces challenges with interest coverage by earnings despite becoming profitable this year with improved financial results compared to last year.

- Insights from our recent growth report point to a promising forecast for doValue's business outlook.

- Unlock comprehensive insights into our analysis of doValue stock in this financial health report.

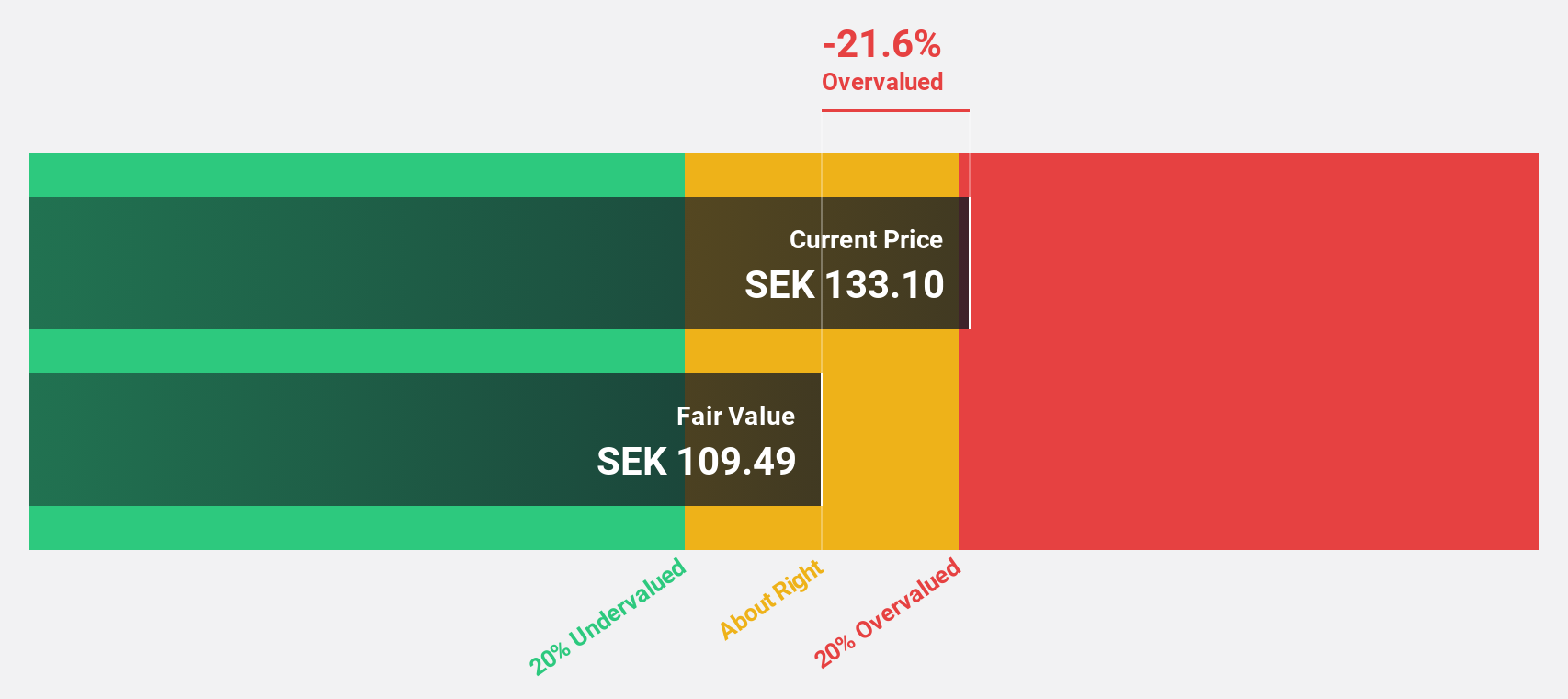

Munters Group (OM:MTRS)

Overview: Munters Group AB (publ) offers climate solutions across the Americas, Europe, the Middle East, Africa, and Asia with a market cap of approximately SEK24.97 billion.

Operations: The company's revenue segments consist of Air Tech at SEK8.05 billion, Food Tech at SEK3.13 billion, and Data Center Technologies at SEK4.94 billion.

Estimated Discount To Fair Value: 10.1%

Munters Group is trading at SEK 136.8, slightly below its fair value estimate of SEK 152.23, indicating some undervaluation based on cash flows. The company anticipates earnings growth of 20.6% annually, surpassing the Swedish market's rate, although it carries substantial debt. Recent strategic moves include issuing green bonds worth SEK 1 billion to diversify funding and opening a new facility in Massachusetts to enhance production capacity and sustainability efforts for long-term growth objectives.

- Our expertly prepared growth report on Munters Group implies its future financial outlook may be stronger than recent results.

- Dive into the specifics of Munters Group here with our thorough financial health report.

Seize The Opportunity

- Click this link to deep-dive into the 182 companies within our Undervalued European Stocks Based On Cash Flows screener.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if BFF Bank might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About BIT:BFF

BFF Bank

Engages in non-recourse factoring and credit management activities towards public administration bodies and private hospitals in Italy, Croatia, the Czech Republic, France, Greece, Poland, Portugal, Slovakia, and Spain.

Reasonable growth potential with adequate balance sheet and pays a dividend.

Market Insights

Advertisement

Community Narratives

Kodiak AI - a potential 100 bagger opportunity?

Fair Value US$14.00|44.7% undervalued

DA

Community Contributor

A Fair Price for a Great Business Facing Real Threats

Fair Value US$383.06|13.0% undervalued

IM

Community Contributor

AXON And Shopify Integration Will Unlock Global Mobile Advertising

Fair Value US$646.30|0% overvalued

AN

Based on Analyst Price Targets