Advertisement

- Italy

- /

- Construction

- /

- BIT:TFIN

TREVI - Finanziaria Industriale S.p.A.'s (BIT:TFIN) Price Is Right But Growth Is Lacking After Shares Rocket 30%

TREVI - Finanziaria Industriale S.p.A. (BIT:TFIN) shares have had a really impressive month, gaining 30% after a shaky period beforehand. Longer-term shareholders would be thankful for the recovery in the share price since it's now virtually flat for the year after the recent bounce.

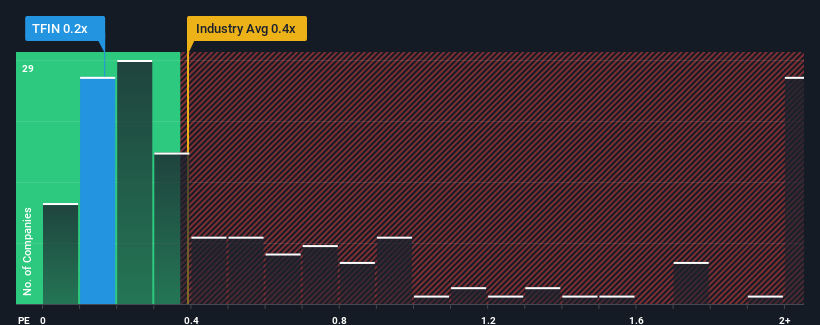

In spite of the firm bounce in price, considering around half the companies operating in Italy's Construction industry have price-to-sales ratios (or "P/S") above 0.7x, you may still consider TREVI - Finanziaria Industriale as an solid investment opportunity with its 0.2x P/S ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the reduced P/S.

Check out our latest analysis for TREVI - Finanziaria Industriale

What Does TREVI - Finanziaria Industriale's P/S Mean For Shareholders?

TREVI - Finanziaria Industriale could be doing better as it's been growing revenue less than most other companies lately. Perhaps the market is expecting the current trend of poor revenue growth to continue, which has kept the P/S suppressed. If you still like the company, you'd be hoping revenue doesn't get any worse and that you could pick up some stock while it's out of favour.

Keen to find out how analysts think TREVI - Finanziaria Industriale's future stacks up against the industry? In that case, our free report is a great place to start.How Is TREVI - Finanziaria Industriale's Revenue Growth Trending?

There's an inherent assumption that a company should underperform the industry for P/S ratios like TREVI - Finanziaria Industriale's to be considered reasonable.

Retrospectively, the last year delivered an exceptional 20% gain to the company's top line. As a result, it also grew revenue by 14% in total over the last three years. Therefore, it's fair to say the revenue growth recently has been respectable for the company.

Looking ahead now, revenue is anticipated to climb by 0.2% during the coming year according to the lone analyst following the company. That's shaping up to be materially lower than the 20% growth forecast for the broader industry.

With this in consideration, its clear as to why TREVI - Finanziaria Industriale's P/S is falling short industry peers. It seems most investors are expecting to see limited future growth and are only willing to pay a reduced amount for the stock.

The Final Word

The latest share price surge wasn't enough to lift TREVI - Finanziaria Industriale's P/S close to the industry median. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

As we suspected, our examination of TREVI - Finanziaria Industriale's analyst forecasts revealed that its inferior revenue outlook is contributing to its low P/S. Right now shareholders are accepting the low P/S as they concede future revenue probably won't provide any pleasant surprises. The company will need a change of fortune to justify the P/S rising higher in the future.

Don't forget that there may be other risks. For instance, we've identified 4 warning signs for TREVI - Finanziaria Industriale (2 can't be ignored) you should be aware of.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Valuation is complex, but we're here to simplify it.

Discover if TREVI - Finanziaria Industriale might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BIT:TFIN

Undervalued with excellent balance sheet.

Market Insights

Advertisement

Community Narratives

Nike's Direct-to-Consumer Focus Will Drive Future Growth

Fair Value US$87.90|18.2% undervalued

UN

Community Contributor

Novo Nordisk will dominate GLP-1 market with Ozempic and Wegovy growth

Fair Value US$89.59|12.1% undervalued

BE

Community Contributor

Rheinmetall could get 20-25% of EU-NATO 3%-GDP defence spending

Fair Value €7.57k|82.4% undervalued

NO

Community Contributor