Advertisement

The Market Lifts Fincantieri S.p.A. (BIT:FCT) Shares 25% But It Can Do More

Despite an already strong run, Fincantieri S.p.A. (BIT:FCT) shares have been powering on, with a gain of 25% in the last thirty days. The last 30 days bring the annual gain to a very sharp 77%.

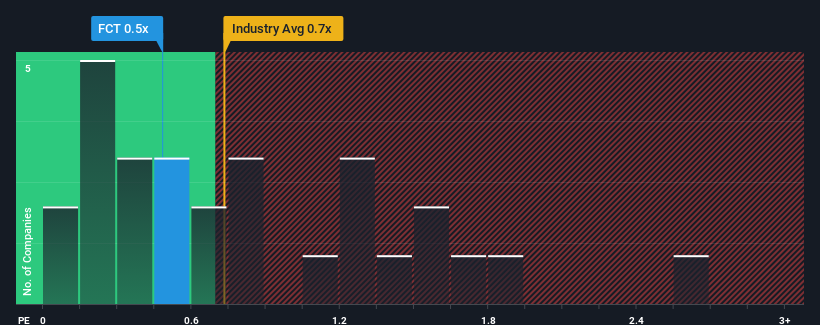

Although its price has surged higher, there still wouldn't be many who think Fincantieri's price-to-sales (or "P/S") ratio of 0.5x is worth a mention when the median P/S in Italy's Machinery industry is similar at about 0.7x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

Our free stock report includes 3 warning signs investors should be aware of before investing in Fincantieri. Read for free now.View our latest analysis for Fincantieri

What Does Fincantieri's P/S Mean For Shareholders?

Fincantieri certainly has been doing a good job lately as its revenue growth has been positive while most other companies have been seeing their revenue go backwards. It might be that many expect the strong revenue performance to deteriorate like the rest, which has kept the P/S ratio from rising. If not, then existing shareholders have reason to be feeling optimistic about the future direction of the share price.

Keen to find out how analysts think Fincantieri's future stacks up against the industry? In that case, our free report is a great place to start.How Is Fincantieri's Revenue Growth Trending?

The only time you'd be comfortable seeing a P/S like Fincantieri's is when the company's growth is tracking the industry closely.

Taking a look back first, we see that the company managed to grow revenues by a handy 6.8% last year. The solid recent performance means it was also able to grow revenue by 16% in total over the last three years. So we can start by confirming that the company has actually done a good job of growing revenue over that time.

Shifting to the future, estimates from the six analysts covering the company suggest revenue should grow by 8.4% each year over the next three years. Meanwhile, the rest of the industry is forecast to only expand by 5.1% each year, which is noticeably less attractive.

With this in consideration, we find it intriguing that Fincantieri's P/S is closely matching its industry peers. It may be that most investors aren't convinced the company can achieve future growth expectations.

The Key Takeaway

Fincantieri's stock has a lot of momentum behind it lately, which has brought its P/S level with the rest of the industry. It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

Despite enticing revenue growth figures that outpace the industry, Fincantieri's P/S isn't quite what we'd expect. Perhaps uncertainty in the revenue forecasts are what's keeping the P/S ratio consistent with the rest of the industry. At least the risk of a price drop looks to be subdued, but investors seem to think future revenue could see some volatility.

Having said that, be aware Fincantieri is showing 3 warning signs in our investment analysis, and 2 of those are a bit concerning.

If these risks are making you reconsider your opinion on Fincantieri, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BIT:FCT

Reasonable growth potential with acceptable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|44.6% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|46.4% undervalued

TO

Community Contributor