Advertisement

- Italy

- /

- Auto Components

- /

- BIT:CFL

Cofle (BIT:CFL) Might Be Having Difficulty Using Its Capital Effectively

There are a few key trends to look for if we want to identify the next multi-bagger. Typically, we'll want to notice a trend of growing return on capital employed (ROCE) and alongside that, an expanding base of capital employed. This shows us that it's a compounding machine, able to continually reinvest its earnings back into the business and generate higher returns. However, after investigating Cofle (BIT:CFL), we don't think it's current trends fit the mold of a multi-bagger.

Understanding Return On Capital Employed (ROCE)

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. To calculate this metric for Cofle, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.15 = €6.3m ÷ (€63m - €22m) (Based on the trailing twelve months to June 2023).

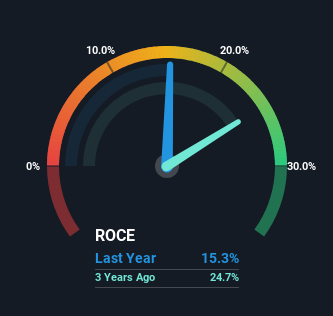

So, Cofle has an ROCE of 15%. On its own, that's a standard return, however it's much better than the 9.7% generated by the Auto Components industry.

View our latest analysis for Cofle

Above you can see how the current ROCE for Cofle compares to its prior returns on capital, but there's only so much you can tell from the past. If you'd like to see what analysts are forecasting going forward, you should check out our free report for Cofle.

So How Is Cofle's ROCE Trending?

On the surface, the trend of ROCE at Cofle doesn't inspire confidence. Around three years ago the returns on capital were 25%, but since then they've fallen to 15%. However, given capital employed and revenue have both increased it appears that the business is currently pursuing growth, at the consequence of short term returns. If these investments prove successful, this can bode very well for long term stock performance.

In Conclusion...

In summary, despite lower returns in the short term, we're encouraged to see that Cofle is reinvesting for growth and has higher sales as a result. These growth trends haven't led to growth returns though, since the stock has fallen 35% over the last year. So we think it'd be worthwhile to look further into this stock given the trends look encouraging.

Cofle does come with some risks though, we found 3 warning signs in our investment analysis, and 1 of those is potentially serious...

For those who like to invest in solid companies, check out this free list of companies with solid balance sheets and high returns on equity.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BIT:CFL

Cofle

Engages in the design, production, sale, and marketing of control cables and control systems worldwide.

Undervalued with reasonable growth potential.

Market Insights

Advertisement

Weekly Picks

DA

davidlsander on Nevgold ·

The U.S. Government Is Desperate for This Metal. This Tiny Miner Has It -- Its Closest Peer Is Already Worth Double.

Fair Value:US$2.1944.7% undervalued

24 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6512.7% undervalued

56 followersusers have followed this narrative

2 commentsusers have commented on this narrative

9 likesusers have liked this narrative

JD

JD009 on Celsius Holdings ·

From $5M to $2B: Why the 2024 Crash Was the Best Buying Opportunity in Consumer Stocks

Fair Value:US$55.4345.9% undervalued

19 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

WA

Wavefarer on Accenture ·

High-quality global services company facing an AI-driven valuation reset.

Fair Value:US$30152.0% undervalued

16 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

Recently Updated Narratives

CH

chris_packerfan on Micron Technology ·

Expect Micron Technology's Valuation to Hit 1890.54 Next Year

Fair Value:US$1.89k54.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

ES

Esteban on Hershey ·

Hershey - fortress brand-and-scale position in U.S. confectionery: protects the downside far better than it compounds the upside

Fair Value:US$79.25120.5% overvalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

RockeTeller on Silver One Resources ·

Silver One Resources, US$0.96/oz for 137Moz AgEq Past-Producing Silver Project, Eric Sprott Owns 15.61%

Fair Value:CA$2.585.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75026.5% undervalued

93 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5456.6% undervalued

63 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6512.7% undervalued

56 followersusers have followed this narrative

2 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Trending Discussion

ST

StoxEurope on Koninklijke Ahold Delhaize ·

I ran Ahold Delhaize through a three-model triangulation — DCF, dividend discount, and residual inco...

1

|0

BE

benjamin_lvieq on PayPal Holdings ·

An investment case is not about loving the product. Its about price vs reality.

1

|0