Advertisement

It's common for many investors, especially those who are inexperienced, to buy shares in companies with a good story even if these companies are loss-making. But the reality is that when a company loses money each year, for long enough, its investors will usually take their share of those losses. Loss-making companies are always racing against time to reach financial sustainability, so investors in these companies may be taking on more risk than they should.

So if this idea of high risk and high reward doesn't suit, you might be more interested in profitable, growing companies, like NLC India (NSE:NLCINDIA). While profit isn't the sole metric that should be considered when investing, it's worth recognising businesses that can consistently produce it.

See our latest analysis for NLC India

How Quickly Is NLC India Increasing Earnings Per Share?

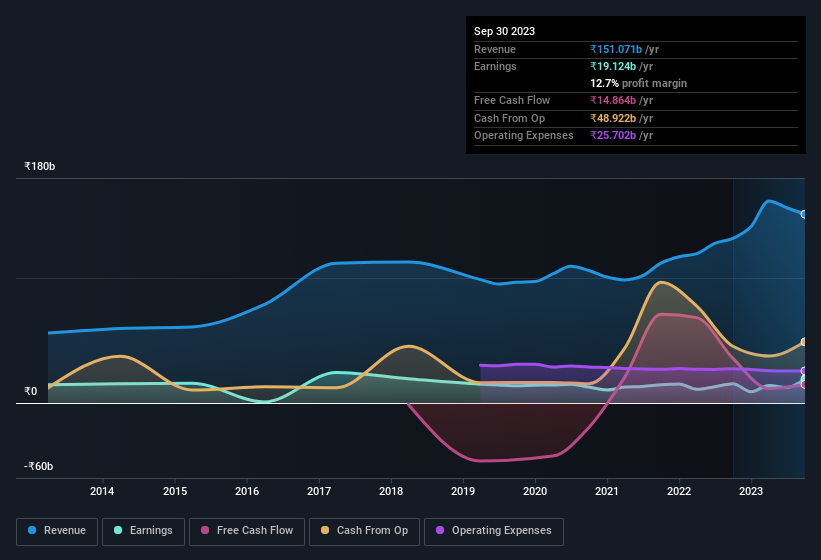

Generally, companies experiencing growth in earnings per share (EPS) should see similar trends in share price. That makes EPS growth an attractive quality for any company. Over the last three years, NLC India has grown EPS by 14% per year. That's a pretty good rate, if the company can sustain it.

Careful consideration of revenue growth and earnings before interest and taxation (EBIT) margins can help inform a view on the sustainability of the recent profit growth. The music to the ears of NLC India shareholders is that EBIT margins have grown from 24% to 28% in the last 12 months and revenues are on an upwards trend as well. Ticking those two boxes is a good sign of growth, in our book.

In the chart below, you can see how the company has grown earnings and revenue, over time. For finer detail, click on the image.

While it's always good to see growing profits, you should always remember that a weak balance sheet could come back to bite. So check NLC India's balance sheet strength, before getting too excited.

Are NLC India Insiders Aligned With All Shareholders?

It's a good habit to check into a company's remuneration policies to ensure that the CEO and management team aren't putting their own interests before that of the shareholder with excessive salary packages. The median total compensation for CEOs of companies similar in size to NLC India, with market caps between ₹166b and ₹533b, is around ₹47m.

The CEO of NLC India only received ₹5.4m in total compensation for the year ending March 2023. First impressions seem to indicate a compensation policy that is favourable to shareholders. CEO compensation is hardly the most important aspect of a company to consider, but when it's reasonable, that gives a little more confidence that leadership are looking out for shareholder interests. Generally, arguments can be made that reasonable pay levels attest to good decision-making.

Should You Add NLC India To Your Watchlist?

As previously touched on, NLC India is a growing business, which is encouraging. Not only that, but the CEO is paid quite reasonably, which should prompt investors to feel more trusting of the board of directors. All things considered, NLC India is definitely worth taking a deeper dive into. Before you take the next step you should know about the 2 warning signs for NLC India that we have uncovered.

There's always the possibility of doing well buying stocks that are not growing earnings and do not have insiders buying shares. But for those who consider these important metrics, we encourage you to check out companies that do have those features. You can access a free list of them here.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Valuation is complex, but we're here to simplify it.

Discover if NLC India might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:NLCINDIA

Solid track record and fair value.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on TAV Havalimanlari Holding ·

TAV Havalimanlari Holding will fly high with 25.68% revenue growth

Fair Value:₺545.1648.6% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.3% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k2.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

93 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative