- India

- /

- Communications

- /

- NSEI:TEJASNET

Tejas Networks Limited (NSE:TEJASNET) Analysts Are Pretty Bullish On The Stock After Recent Results

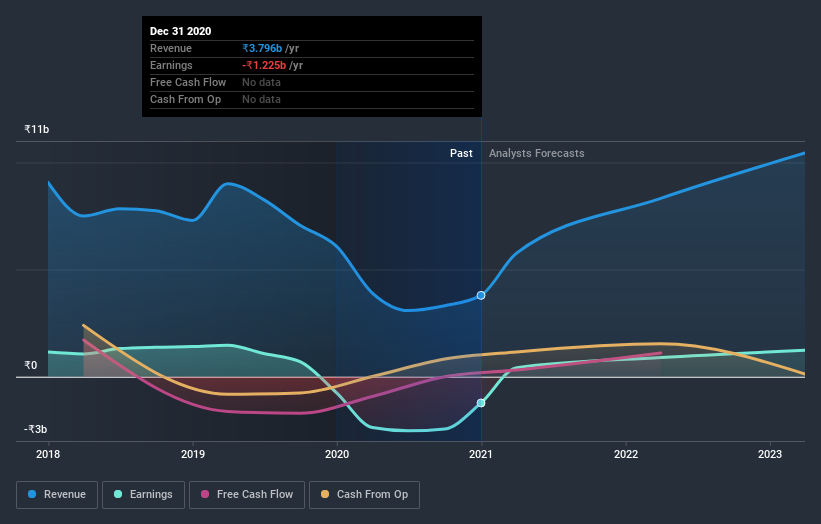

Investors in Tejas Networks Limited (NSE:TEJASNET) had a good week, as its shares rose 6.2% to close at ₹142 following the release of its third-quarter results. Revenues came in at ₹1.3b, an impressive 22% ahead of analyst forecasts. This is an important time for investors, as they can track a company's performance in its report, look at what experts are forecasting for next year, and see if there has been any change to expectations for the business. With this in mind, we've gathered the latest statutory forecasts to see what the analysts are expecting for next year.

Check out our latest analysis for Tejas Networks

Taking into account the latest results, the most recent consensus for Tejas Networks from dual analysts is for revenues of ₹8.32b in 2022 which, if met, would be a sizeable 119% increase on its sales over the past 12 months. Earnings are expected to improve, with Tejas Networks forecast to report a statutory profit of ₹9.40 per share. In the lead-up to this report, the analysts had been modelling revenues of ₹7.92b and earnings per share (EPS) of ₹9.05 in 2022. So there seems to have been a moderate uplift in sentiment following the latest results, given the upgrades to both revenue and earnings per share forecasts for next year.

With these upgrades, we're not surprised to see that the analysts have lifted their price target 63% to ₹155per share.

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. For example, we noticed that Tejas Networks' rate of growth is expected to accelerate meaningfully, with revenues forecast to grow 119%, well above its historical decline of 12% a year over the past five years. Compare this against analyst estimates for the wider industry, which suggest that (in aggregate) industry revenues are expected to grow 20% next year. So it looks like Tejas Networks is expected to grow faster than its competitors, at least for a while.

The Bottom Line

The most important thing here is that the analysts upgraded their earnings per share estimates, suggesting that there has been a clear increase in optimism towards Tejas Networks following these results. Happily, they also upgraded their revenue estimates, and are forecasting revenues to grow faster than the wider industry. There was also a nice increase in the price target, with the analysts clearly feeling that the intrinsic value of the business is improving.

Keeping that in mind, we still think that the longer term trajectory of the business is much more important for investors to consider. We have analyst estimates for Tejas Networks going out as far as 2023, and you can see them free on our platform here.

You still need to take note of risks, for example - Tejas Networks has 1 warning sign we think you should be aware of.

When trading Tejas Networks or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Tejas Networks might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NSEI:TEJASNET

Tejas Networks

Designs, manufactures, and sells wireless and wireline networking products in India and internationally.

Slight with mediocre balance sheet.