Advertisement

The board of Tata Consultancy Services Limited (NSE:TCS) has announced that it will pay a dividend on the 4th of August, with investors receiving ₹11.00 per share. This takes the dividend yield to 3.9%, which shareholders will be pleased with.

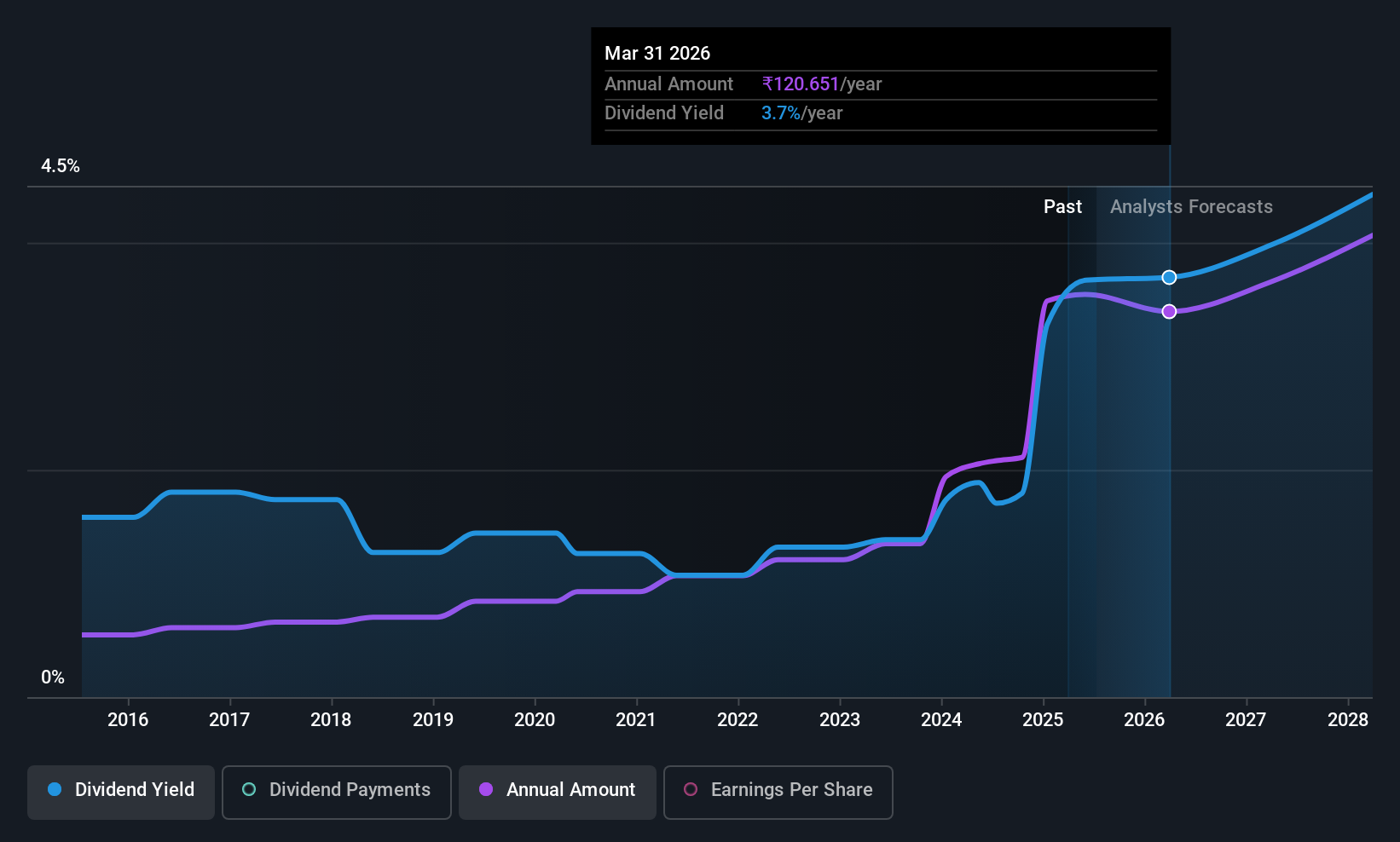

Tata Consultancy Services' Payment Could Potentially Have Solid Earnings Coverage

A big dividend yield for a few years doesn't mean much if it can't be sustained. Based on the last dividend, Tata Consultancy Services is earning enough to cover the payment, but then it makes up 104% of cash flows. While the company may be more focused on returning cash to shareholders than growing the business at this time, we think that a cash payout ratio this high might expose the dividend to being cut if the business ran into some challenges.

EPS is set to grow by 24.5% over the next year. If recent patterns in the dividend continues, the payout ratio in 12 months could be 83% which is a bit high but can definitely be sustainable.

Check out our latest analysis for Tata Consultancy Services

Tata Consultancy Services Has A Solid Track Record

The company has a sustained record of paying dividends with very little fluctuation. Since 2015, the annual payment back then was ₹19.50, compared to the most recent full-year payment of ₹126.00. This works out to be a compound annual growth rate (CAGR) of approximately 21% a year over that time. So, dividends have been growing pretty quickly, and even more impressively, they haven't experienced any notable falls during this period.

The Dividend Looks Likely To Grow

Some investors will be chomping at the bit to buy some of the company's stock based on its dividend history. Tata Consultancy Services has seen EPS rising for the last five years, at 10% per annum. The company is paying out a lot of its cash as a dividend, but it looks okay based on the payout ratio.

In Summary

Overall, we always like to see the dividend being raised, but we don't think Tata Consultancy Services will make a great income stock. While the low payout ratio is a redeeming feature, this is offset by the minimal cash to cover the payments. We would probably look elsewhere for an income investment.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. Taking the debate a bit further, we've identified 1 warning sign for Tata Consultancy Services that investors need to be conscious of moving forward. Is Tata Consultancy Services not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if Tata Consultancy Services might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:TCS

Tata Consultancy Services

Provides information technology (IT) and IT enabled services in the Americas, Europe, India, and internationally.

Flawless balance sheet established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|12.2% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.7% undervalued

TR

Community Contributor