Advertisement

Returns On Capital At Kellton Tech Solutions (NSE:KELLTONTEC) Have Hit The Brakes

Finding a business that has the potential to grow substantially is not easy, but it is possible if we look at a few key financial metrics. Amongst other things, we'll want to see two things; firstly, a growing return on capital employed (ROCE) and secondly, an expansion in the company's amount of capital employed. Put simply, these types of businesses are compounding machines, meaning they are continually reinvesting their earnings at ever-higher rates of return. In light of that, when we looked at Kellton Tech Solutions (NSE:KELLTONTEC) and its ROCE trend, we weren't exactly thrilled.

What Is Return On Capital Employed (ROCE)?

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. To calculate this metric for Kellton Tech Solutions, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

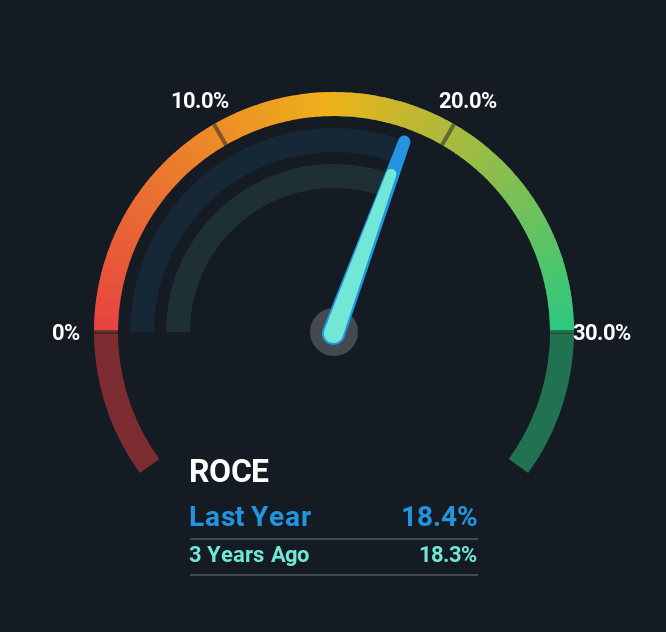

0.18 = ₹1.1b ÷ (₹7.9b - ₹1.9b) (Based on the trailing twelve months to March 2025).

Thus, Kellton Tech Solutions has an ROCE of 18%. In absolute terms, that's a pretty normal return, and it's somewhat close to the IT industry average of 16%.

View our latest analysis for Kellton Tech Solutions

Historical performance is a great place to start when researching a stock so above you can see the gauge for Kellton Tech Solutions' ROCE against it's prior returns. If you'd like to look at how Kellton Tech Solutions has performed in the past in other metrics, you can view this free graph of Kellton Tech Solutions' past earnings, revenue and cash flow.

What The Trend Of ROCE Can Tell Us

Over the past five years, Kellton Tech Solutions' ROCE and capital employed have both remained mostly flat. It's not uncommon to see this when looking at a mature and stable business that isn't re-investing its earnings because it has likely passed that phase of the business cycle. So unless we see a substantial change at Kellton Tech Solutions in terms of ROCE and additional investments being made, we wouldn't hold our breath on it being a multi-bagger.

The Bottom Line

In a nutshell, Kellton Tech Solutions has been trudging along with the same returns from the same amount of capital over the last five years. Investors must think there's better things to come because the stock has knocked it out of the park, delivering a 565% gain to shareholders who have held over the last five years. However, unless these underlying trends turn more positive, we wouldn't get our hopes up too high.

On a final note, we've found 1 warning sign for Kellton Tech Solutions that we think you should be aware of.

For those who like to invest in solid companies, check out this free list of companies with solid balance sheets and high returns on equity.

Valuation is complex, but we're here to simplify it.

Discover if Kellton Tech Solutions might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:KELLTONTEC

Kellton Tech Solutions

Engages in the provision of digital transformation, ERP, and other IT services in APAC, Europe, the United States, and internationally.

Excellent balance sheet with acceptable track record.

Market Insights

Advertisement

Weekly Picks

RI

Rick_Orford on Upside Gold ·

This OVERLOOKED Gold Stock Could TRIPLE - 3.3M Ounces, Bottom-of-Peer Valuation

Fair Value:CA$470.5% undervalued

20 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9719.1% undervalued

52 followersusers have followed this narrative

0 commentsusers have commented on this narrative

12 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1925.7% undervalued

42 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

BJ

Bjergby on PagSeguro Digital ·

PagSeguro: A Cheap Bet on a Bank Hiding Inside a Payments Company, Priced for Failure

Fair Value:US$19.251.3% undervalued

17 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

Recently Updated Narratives

DE

DeathSmiIes on New Horizon Aircraft ·

HORIZON AIRCRAFT (HOVR) Institutional Investor Package

Fair Value:US$2085.4% undervalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

EL

El_Gecko on AST SpaceMobile ·

AST SpaceMobile will achieve 80% revenue growth powered by their innovative future plans

Fair Value:US$524.778.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KA

kapirey on Tencent Holdings ·

Tencent Holdings will see revenue grow by 14%

Fair Value:HK$37015.5% overvalued

31 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8589.4% undervalued

120 followersusers have followed this narrative

2 commentsusers have commented on this narrative

34 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9719.1% undervalued

52 followersusers have followed this narrative

0 commentsusers have commented on this narrative

12 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1925.7% undervalued

42 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative