Advertisement

- India

- /

- Professional Services

- /

- NSEI:FSL

Earnings Beat: Firstsource Solutions Limited Just Beat Analyst Forecasts, And Analysts Have Been Updating Their Models

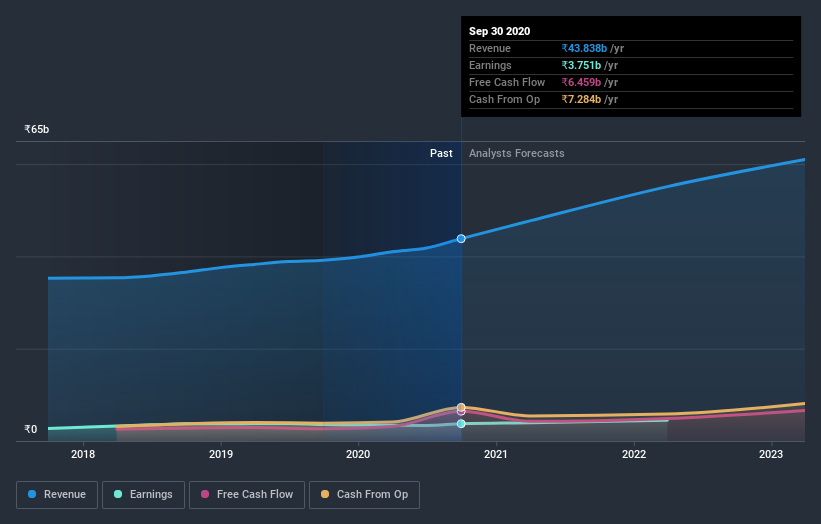

Firstsource Solutions Limited (NSE:FSL) defied analyst predictions to release its second-quarter results, which were ahead of market expectations. The company beat expectations with revenues of ₹12b arriving 4.2% ahead of forecasts. Statutory earnings per share (EPS) were ₹1.50, 7.1% ahead of estimates. Earnings are an important time for investors, as they can track a company's performance, look at what the analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. We've gathered the most recent statutory forecasts to see whether the analysts have changed their earnings models, following these results.

See our latest analysis for Firstsource Solutions

Taking into account the latest results, the current consensus from Firstsource Solutions' dual analysts is for revenues of ₹47.7b in 2021, which would reflect a notable 8.8% increase on its sales over the past 12 months. Statutory earnings per share are predicted to accumulate 4.8% to ₹5.70. In the lead-up to this report, the analysts had been modelling revenues of ₹47.1b and earnings per share (EPS) of ₹5.00 in 2021. Although the revenue estimates have not really changed, we can see there's been a nice increase in earnings per share expectations, suggesting that the analysts have become more bullish after the latest result.

The analysts have been lifting their price targets on the back of the earnings upgrade, with the consensus price target rising 46% to ₹92.50.

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. It's clear from the latest estimates that Firstsource Solutions' rate of growth is expected to accelerate meaningfully, with the forecast 8.8% revenue growth noticeably faster than its historical growth of 5.8%p.a. over the past five years. Compare this with other companies in the same industry, which are forecast to grow their revenue 9.5% next year. Firstsource Solutions is expected to grow at about the same rate as its industry, so it's not clear that we can draw any conclusions from its growth relative to competitors.

The Bottom Line

The most important thing here is that the analysts upgraded their earnings per share estimates, suggesting that there has been a clear increase in optimism towards Firstsource Solutions following these results. They also reconfirmed their revenue estimates, with the company predicted to grow at about the same rate as the wider industry. We note an upgrade to the price target, suggesting that the analysts believes the intrinsic value of the business is likely to improve over time.

Keeping that in mind, we still think that the longer term trajectory of the business is much more important for investors to consider. At least one analyst has provided forecasts out to 2023, which can be seen for free on our platform here.

Don't forget that there may still be risks. For instance, we've identified 3 warning signs for Firstsource Solutions that you should be aware of.

When trading Firstsource Solutions or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About NSEI:FSL

Firstsource Solutions

Provides tech-enabled business processes in India, the United Kingdom, the United States, Asia, South Africa, the Philippines, Australia, New Zealand, and internationally.

Reasonable growth potential with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|41.7% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|63.2% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|39.7% undervalued

UN

Community Contributor