- India

- /

- Semiconductors

- /

- NSEI:SURANASOL

These 4 Measures Indicate That Surana Solar (NSE:SURANASOL) Is Using Debt Reasonably Well

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. As with many other companies Surana Solar Limited (NSE:SURANASOL) makes use of debt. But should shareholders be worried about its use of debt?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for Surana Solar

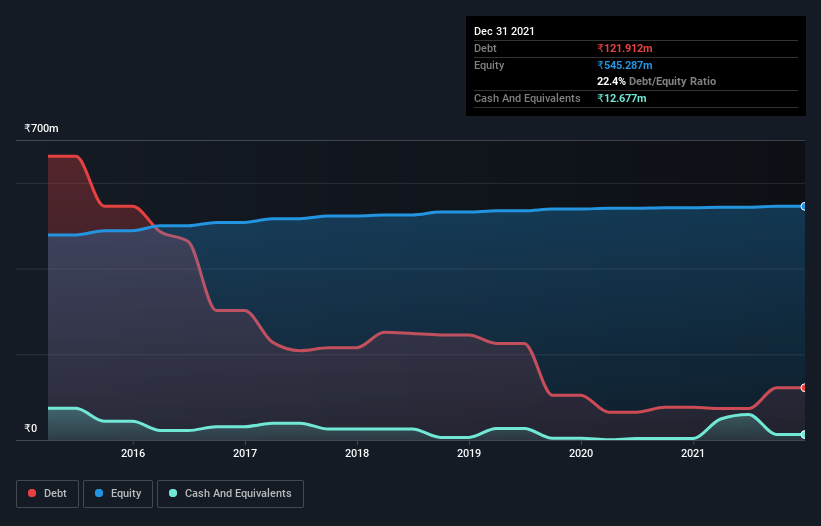

What Is Surana Solar's Net Debt?

The image below, which you can click on for greater detail, shows that at September 2021 Surana Solar had debt of ₹121.9m, up from ₹76.3m in one year. However, because it has a cash reserve of ₹12.7m, its net debt is less, at about ₹109.2m.

A Look At Surana Solar's Liabilities

The latest balance sheet data shows that Surana Solar had liabilities of ₹140.3m due within a year, and liabilities of ₹8.37m falling due after that. On the other hand, it had cash of ₹12.7m and ₹44.1m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by ₹91.9m.

Given Surana Solar has a market capitalization of ₹1.18b, it's hard to believe these liabilities pose much threat. Having said that, it's clear that we should continue to monitor its balance sheet, lest it change for the worse.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Surana Solar's net debt is sitting at a very reasonable 2.2 times its EBITDA, while its EBIT covered its interest expense just 2.9 times last year. In large part that's due to the company's significant depreciation and amortisation charges, which arguably mean its EBITDA is a very generous measure of earnings, and its debt may be more of a burden than it first appears. The bad news is that Surana Solar saw its EBIT decline by 19% over the last year. If that sort of decline is not arrested, then the managing its debt will be harder than selling broccoli flavoured ice-cream for a premium. There's no doubt that we learn most about debt from the balance sheet. But it is Surana Solar's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Over the last three years, Surana Solar actually produced more free cash flow than EBIT. That sort of strong cash conversion gets us as excited as the crowd when the beat drops at a Daft Punk concert.

Our View

On our analysis Surana Solar's conversion of EBIT to free cash flow should signal that it won't have too much trouble with its debt. However, our other observations weren't so heartening. To be specific, it seems about as good at (not) growing its EBIT as wet socks are at keeping your feet warm. Looking at all this data makes us feel a little cautious about Surana Solar's debt levels. While debt does have its upside in higher potential returns, we think shareholders should definitely consider how debt levels might make the stock more risky. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. Be aware that Surana Solar is showing 4 warning signs in our investment analysis , and 1 of those is significant...

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:SURANASOL

Surana Solar

Manufactures and sells solar panels and solar photovoltaic (PV) modules under the Surana Solar brand in India and internationally.

Excellent balance sheet slight.

Market Insights

Community Narratives