- India

- /

- Semiconductors

- /

- NSEI:SOLEX

The Market Lifts Solex Energy Limited (NSE:SOLEX) Shares 26% But It Can Do More

Solex Energy Limited (NSE:SOLEX) shares have continued their recent momentum with a 26% gain in the last month alone. The annual gain comes to 151% following the latest surge, making investors sit up and take notice.

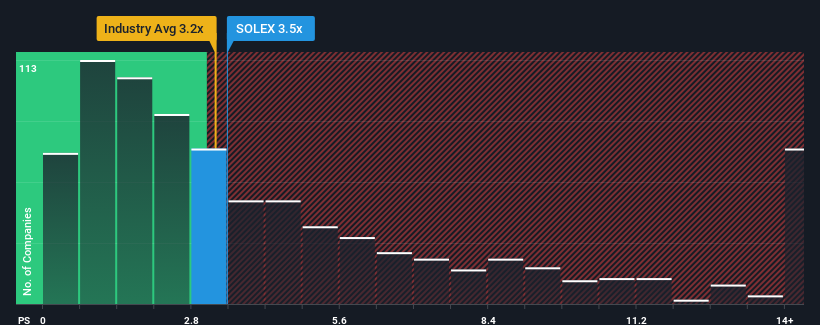

In spite of the firm bounce in price, Solex Energy may still be sending very bullish signals at the moment with its price-to-sales (or "P/S") ratio of 3.5x, since almost half of all companies in the Semiconductor industry in India have P/S ratios greater than 9.1x and even P/S higher than 25x are not unusual. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so limited.

See our latest analysis for Solex Energy

What Does Solex Energy's Recent Performance Look Like?

With revenue growth that's exceedingly strong of late, Solex Energy has been doing very well. It might be that many expect the strong revenue performance to degrade substantially, which has repressed the P/S ratio. If that doesn't eventuate, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on Solex Energy's earnings, revenue and cash flow.How Is Solex Energy's Revenue Growth Trending?

There's an inherent assumption that a company should far underperform the industry for P/S ratios like Solex Energy's to be considered reasonable.

Taking a look back first, we see that the company's revenues underwent some rampant growth over the last 12 months. Pleasingly, revenue has also lifted 160% in aggregate from three years ago, thanks to the last 12 months of explosive growth. Therefore, it's fair to say the revenue growth recently has been superb for the company.

Comparing that to the industry, which is only predicted to deliver 28% growth in the next 12 months, the company's momentum is stronger based on recent medium-term annualised revenue results.

In light of this, it's peculiar that Solex Energy's P/S sits below the majority of other companies. Apparently some shareholders believe the recent performance has exceeded its limits and have been accepting significantly lower selling prices.

What We Can Learn From Solex Energy's P/S?

Even after such a strong price move, Solex Energy's P/S still trails the rest of the industry. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

We're very surprised to see Solex Energy currently trading on a much lower than expected P/S since its recent three-year growth is higher than the wider industry forecast. When we see strong revenue with faster-than-industry growth, we assume there are some significant underlying risks to the company's ability to make money which is applying downwards pressure on the P/S ratio. While recent revenue trends over the past medium-term suggest that the risk of a price decline is low, investors appear to perceive a likelihood of revenue fluctuations in the future.

Before you settle on your opinion, we've discovered 4 warning signs for Solex Energy (3 are concerning!) that you should be aware of.

If these risks are making you reconsider your opinion on Solex Energy, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:SOLEX

Proven track record slight.